Personal Wealth Management / Market Analysis

Gauging the Global Economy in August

A slew of global economic data alludes to growth continuing nicely as the summer wound down.

The recipe for a big, eyeball-grabbing market-related news story typically goes a little like this:

- Take a smidge of geopolitical conflict, mysterious central bank policies few really grasp, legislation and single stock news like a merger or earnings.

- Do not attempt to scale, explain the actual application or put in any sort of context, historical or other.

- Draw grandiose stock market conclusion.

It usually does not go a little like this:

- Take a smidge of manufacturing data, add a dash of service sector results, sprinkle in some trade numbers and beat on medium speed until you have some charts.

- Season with international data to taste.

- Put numbers in context with recent trends.

- Add a joke.

- Draw rational stock market conclusion.

So this article-which will indeed present a slew of data arguing the global economy is on overall solid footing-is not like anything you will have read this week, when central banks and so-called ceasefires garnered most attention. Yet it was particularly hectic for economic data crunchers, statisticians, press release writers and heavy consumers of economic data-and finance nerds like us. And that's even before Friday's US jobs data, which typically trigger a festival of statistical analysis, deep data diving and more.[i] Through Thursday, the week's data show that what folks aren't focusing as much on is a global economy that's growing just fine, thank you very much. Investors would be well served to take note.

This is the week each month when a huge number of monthly economic surveys-Purchasing Managers' Indexes (PMIs)-roll in. These gauges survey businesses and tabulate the percentage of firms polled that saw increased orders, activity, shipments and the like. Now, as we've written, these are not a perfect macroeconomic gauge[ii], because you can get growth in the broad economy with less than half of firms growing-PMIs do not measure magnitude. However, they do provide a relatively timely assessment of recent economic activity, a signpost of the breadth of economic growth.

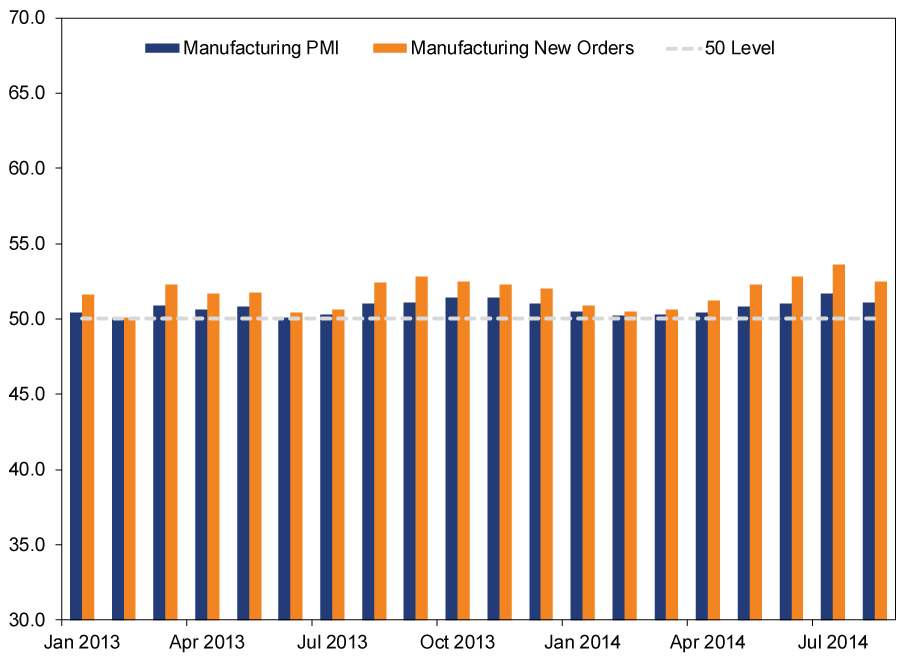

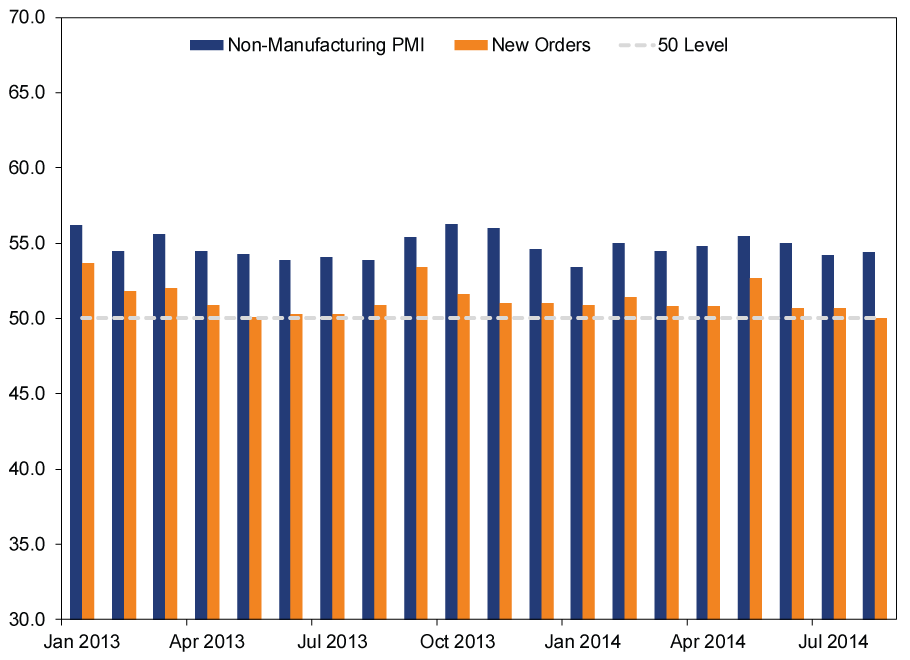

Monday, China's official manufacturing PMI for August came in at 51.1-more than half of firms reported growth, but a smaller share than July's 51.7. The HSBC/Markit preliminary manufacturing PMI for China also slightly slowed, falling to 50.2 from 50.3.[iii] But before hard landing fears could even rev much, Wednesday both Chinese non-manufacturing (services) PMIs grew, with the official gauge hitting 54.4 and HSBC/Markit's reaching 54.1, its strongest reading in over a year. These readings are more or less in line with recent history, which have just barely exceeded the 50 dividing line, or even slightly dipped in the case of HSBC/Markit Manufacturing. (Exhibits 1 & 2) Yet all the while, GDP has grown at a 7%+ clip, enviable by global standards. According to Markit's analysts, the latest PMI figures don't show a marked change from that trend.

Exhibit 1: China Official Manufacturing PMI (Headline) and New Orders

Source: China National Bureau of Statistics, FactSet. January 2013 - August 2014.

Exhibit 2: China Official Non-Manufacturing PMI (Headline) and New Orders

Source: China National Bureau of Statistics, January 2013 - August 2014.

Also reported Monday, eurozone manufacturing PMI fell to 50.7 from July's 51.8, leading to more worries over the currency bloc's economic health. Most analyses seemingly tied the dip to Ukraine tensions, with pundits arguing it hit the German business zeitgeist. However, this seems a premature conclusion to jump to, especially in light of Thursday's report German factory orders-future output-boomed in July. Eurozone services PMI growth also slowed to 53.1 from 54.2 in Wednesday's report. Investor sentiment toward the eurozone seems somewhere on the curve from dour to expecting a deflationary depression, so it's at least notable that both services and manufacturing PMI aren't logging big contractions-they show growth. And, unsurprisingly, that growth is narrow and a bit shaky, which has been the story in the eurozone for much-if not most-of this global expansion.

The UK posted mixed, but still nicely expansionary PMI figures. Manufacturing slowed from 54.8 in July to 52.5, missing estimates. Services, however, grew quickly-accelerating from 59.1 to 60.5, beating estimates. UK Construction PMI also accelerated, rising to 64.0 from 62.4. The UK is still one of the leaders of developed world economic growth.

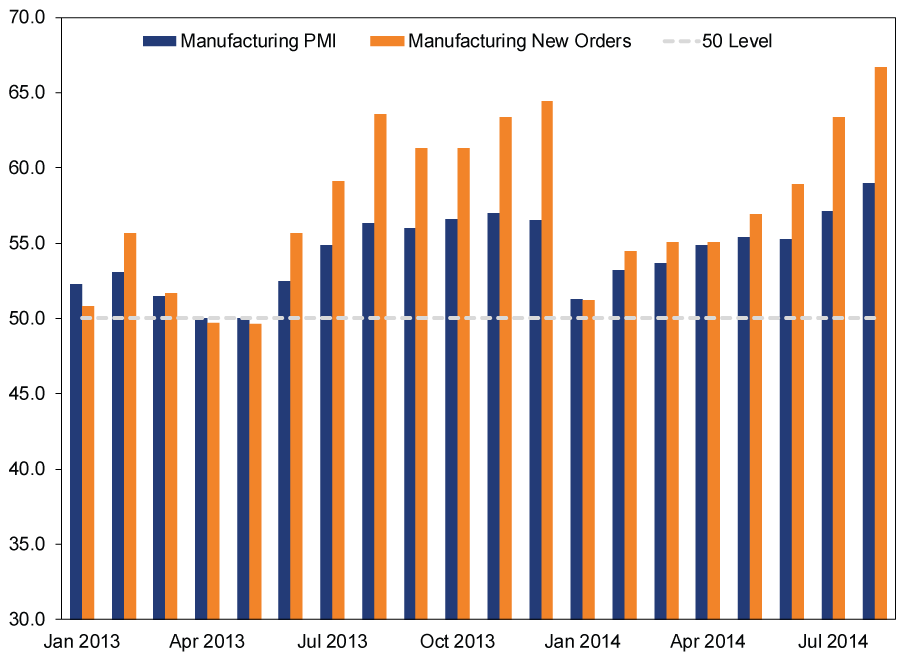

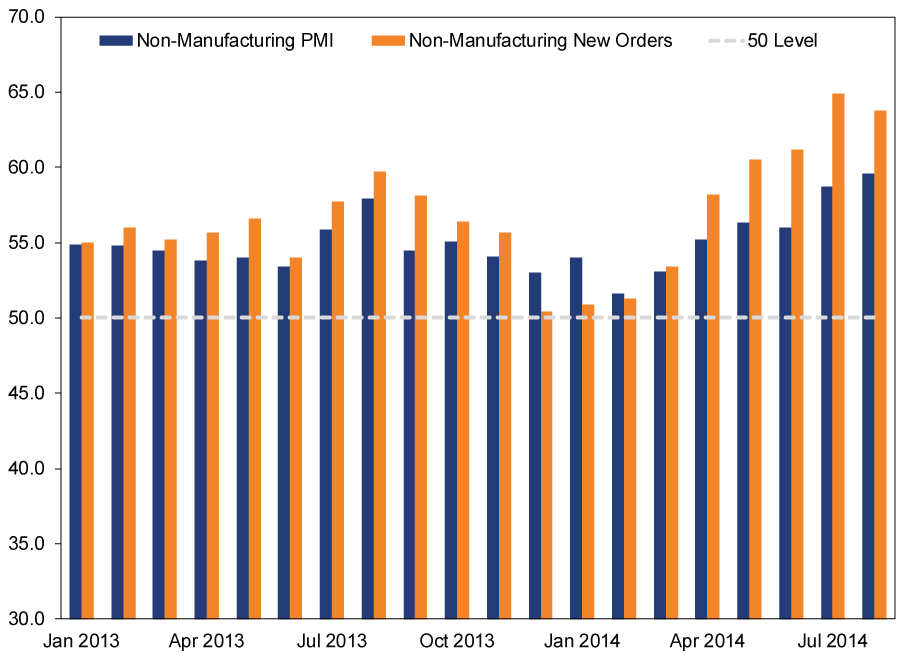

The other, the US, also released a bevy of data this week. Tuesday, ISM published its US manufacturing PMI for August, which hit a three-year high of 59.0, accelerating from July's 57.1 and topping analysts' expectations for a decline to 56.9. ISM's US non-manufacturing gauge also accelerated, to 59.6 from July's 58.7. New orders for manufacturing surged; non-manufacturing orders remained solidly expansionary. (Exhibits 3 & 4)

Exhibit 3: ISM Manufacturing PMI and New Orders

Source: Federal Reserve Bank of St. Louis, January 2013 - August 2014.

Exhibit 4: ISM Non-Manufacturing PMI and New Orders

Source: Federal Reserve Bank of St. Louis, January 2013 - August 2014.

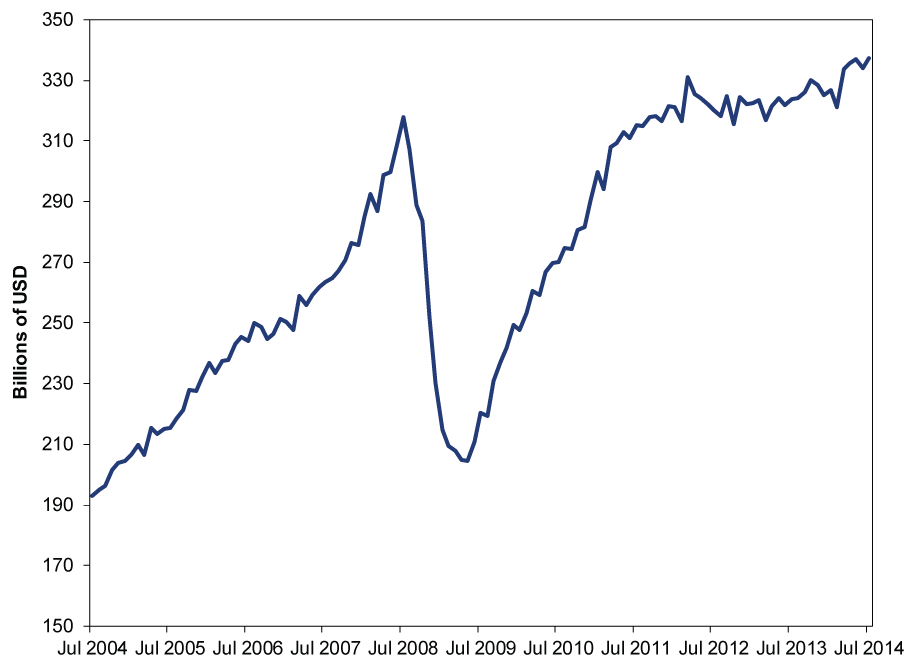

Also in the US, headlines celebrated a declining US trade gap, but the better news was why it fell.[iv] Imports rose 0.8% m/m and exports 1.3%, pushing total trade-exports plus imports-up 1.0% to a new record monthly high. (Exhibit 5)

Exhibit 5: US Total Trade (Monthly, Balance of Payments Basis)

Source: US Census Bureau, US exports plus imports, July 2004 - July 2014.

Sometimes the flashier headline will be worth paying attention to-we aren't suggesting the individual economic data points shown usurp Ukraine and the ECB. But there is a risk investors miss the forest for the trees, as well, because above all else, the dominant economic and market story of the last five years is probably the one all these various global economic data points taken together tell.

[i] The report is, after all, released on the first Friday of the month, and who doesn't love a Friday full of factoids?

[ii] No economic data point is perfect. They all have quirks and imperfections, things to weigh in reviewing them.

[iii] The HSBC gauge excludes large, state-owned enterprises, making them somewhat more narrow than China's official gauges.

[iv] As we've written many times, the difference between exports and imports-the trade deficit-is a near-meaningless economic stat that presumes imports are negative for the US economy, which isn't accurate.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

SHARE THIS MEDIA

Related Resources

Learn More

Learn why 150,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 3/31/2024

New to Fisher? Call Us.

Contact Us Today