Personal Wealth Management / Market Analysis

Research Flash: European Bank Funding Markets

For several months, many have said European banks are having issues with US dollar-based funding. And to an extent, they’ve been right, but that’s not the whole story.

For several months now, pundits, ratings agencies and analysts have said European banks have been having issues with US dollar-based funding, one important source of bank liquidity—and they’ve been right. However, the situation isn’t nearly as dire as many presume.

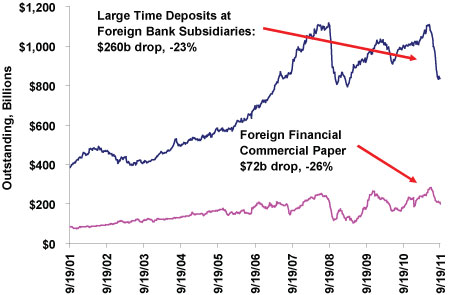

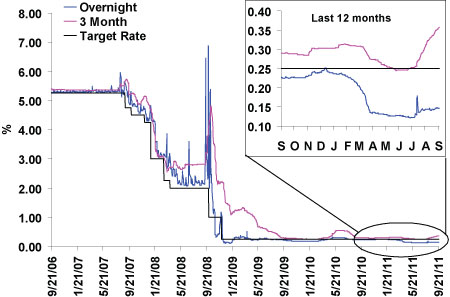

US money market funds—which had funded European banks through securities purchases—are frequently cited as a root cause of the issue. Outstanding Foreign Financial Commercial Paper and Foreign Large Time Deposits have fallen $332 billion collectively (Exhibit 1), and much of this can be attributed to action by money markets. This has driven USD funding rates to recent highs, increasingly making European banks tap their brethren for funding—as seen in interbank lending markets (Exhibit 2). But keep in mind, while USD funding has become more expensive in recent months, it pales in comparison to 2008 when financial panic caused a true liquidity crisis.

Exhibit 1: Money Markets Are Reducing Exposure to European Banks

Source: Thomson Reuters, Federal Reserve; (09/2001-09/2011)

Exhibit 2: USD Funding Markets - USD LIBOR

Source: Thomson Reuters, BBA; (09/2006-09/2011)

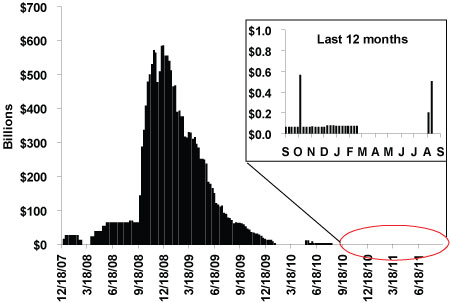

With that in mind,five prominent central banks collectively agreed to reinstate a USD swap facility when mild USD funding strains reappeared in 2010, allowing banks around the world access to USD funding. The cost of this funding is not cheap (the most recent term was seven days at 1.1%), but recent moves higher in USD LIBOR have made the facility cost about as much as in the private sector (many believe this will increase the facility’s usage). Even more recently, the collective central banks have agreed to offer unlimited three-month USD financing to any bank in need. And, further demonstrating central banks’ willingness to stem any banking panics, the ECB recently loosened its collateral requirements—allowing banks access to more than €13 trillion in central bank funding if needed.

So, even if the USD funding squeeze continues, banks always have the option of going to their central bank—and in fact, earlier this year, banks took them up on the offer. In early August, while markets were very volatile, European banks tapped the facility for a measly $700 million, and more recently, a European bank tapped just $575 million. While the limited usage and relatively small amounts are a pretty good sign the banks likely don’t really need the facility, this backstop is a great way to stem potential future problems driven by USD liquidity concerns.

Exhibit 3: Central Bank Liquidity Swaps Facility

Source: Federal Reserve, 12/18/2002-09/14/2011

While USD funding is being squeezed, it’s important to note the vast majority of European banks’ liabilities is in euros. In fact, USD liabilities account for about half of European banks’ foreign currency liabilities but a paltry2.3% of total liabilities.

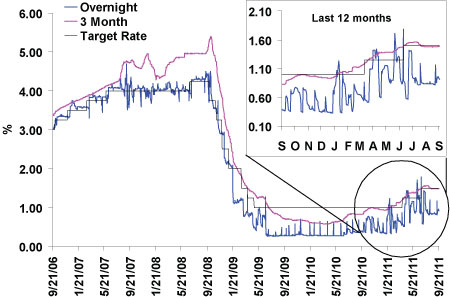

Arguably, the big concern would be a panic in the euro funding market. With €32 trillion of euro liabilities, a squeeze in this market would be dramatically more impactful. However, in part due to central bank facilities, there’s not currently a squeeze in this market. One way to observe this is to look at the spread between LIBOR (London Inter-Bank Offering Rates) and the policy target rate (Exhibit 4). Note the rather substantial difference between today and 2008—interest rates are actually below the target rate, whereas they were substantially above during the panic when liquidity dried up and funding costs soared. Typically, three- and six-month LIBOR is at a slight premium to the target rate, but when fear spiked in 2008, this spread exploded higher as banks stopped lending to each other. Following the panic, the ECB flooded the system with liquidity, and LIBOR moved substantially below the target rate as liquidity was abundant. More recently, the ECB removed some liquidity, so it’s tightened a bit, moving LIBOR closer to historic norms. But this is pretty clearly not indicative of panic. And the same trend exists when measured other ways such as Forward Rate Agreements (FRA) and Euribor.

Exhibit 4: EUR LIBOR Market

Source: Thomson Reuters, BBA; (09/2006-09/2011)

There are valid concerns in Europe, including dislocations in the USD funding market, but coordinated central bank action has alleviated much of the concern for now. However, more importantly, the larger euro-based funding market is currently and overall fine.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

SHARE THIS MEDIA

Related Resources

Learn More

Learn why 150,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 3/31/2024

New to Fisher? Call Us.

Contact Us Today