Retirement Plan Benefits

It makes sense that the key to a secure retirement is saving as much as you can every payday. However, by saving in your employer’s retirement plan, you give yourself the opportunity to benefit from some unique advantages.

Simple Account Savings

Automatic payroll deductions

If you’ve found it difficult to maintain a regular savings habit in the past, your retirement plan makes it much easier for you. Your retirement plan provides the convenience of automatic payroll deductions: The saving amount you choose is deducted out of your paycheck automatically.

Company contributions

Your company may choose to match the dollars you contribute to your retirement plan, up to a certain limit, to accelerate your retirement savings. It’s essentially extra money. If your company provides a matching contribution, take full advantage of it so that you don’t leave any money on the table. Please see your Summary Plan Description to find out if your plan includes a company match contribution and its terms.

Flexible investment support options

Your retirement plan lets you arrange your investments in a way that best fits your personal needs and long-term goals. You can change your investment choices as your situation changes. Learn more information about your investment options and the resources we offer to help you choose them in the Investment Support Options section.

Tax Savings

The difference between traditional pretax and Roth

Determining which type of account is best of you depends on your personal needs and goals. Before you decide, consider talking to a Fisher Retirement Specialist or to a tax adviser to help you look at your specific situation and determine which approach—traditional pretax, Roth or a mixture of both—is best for you.

PAY TAXES LATER:

Traditional

- The money you contribute to your retirement plan is not taxed beforehand.

- You’ll pay taxes when you withdraw the money.

- Earnings made from your contributions will also be taxed later.

- A good option if you see yourself in a lower tax bracket later on.

PAY TAXES NOW:

Roth

- Your contribution is taxed before going into your account.

- If you meet tax law requirements, you can withdraw your contributions plus any plan earnings later in retirement tax-free.

- This is a good option if you see yourself in a higher tax bracket later on.

- Check your plan’s Summary Plan Description for further details and to see if your plan offers a Roth option.

Traditional vs Roth

Compound Growth

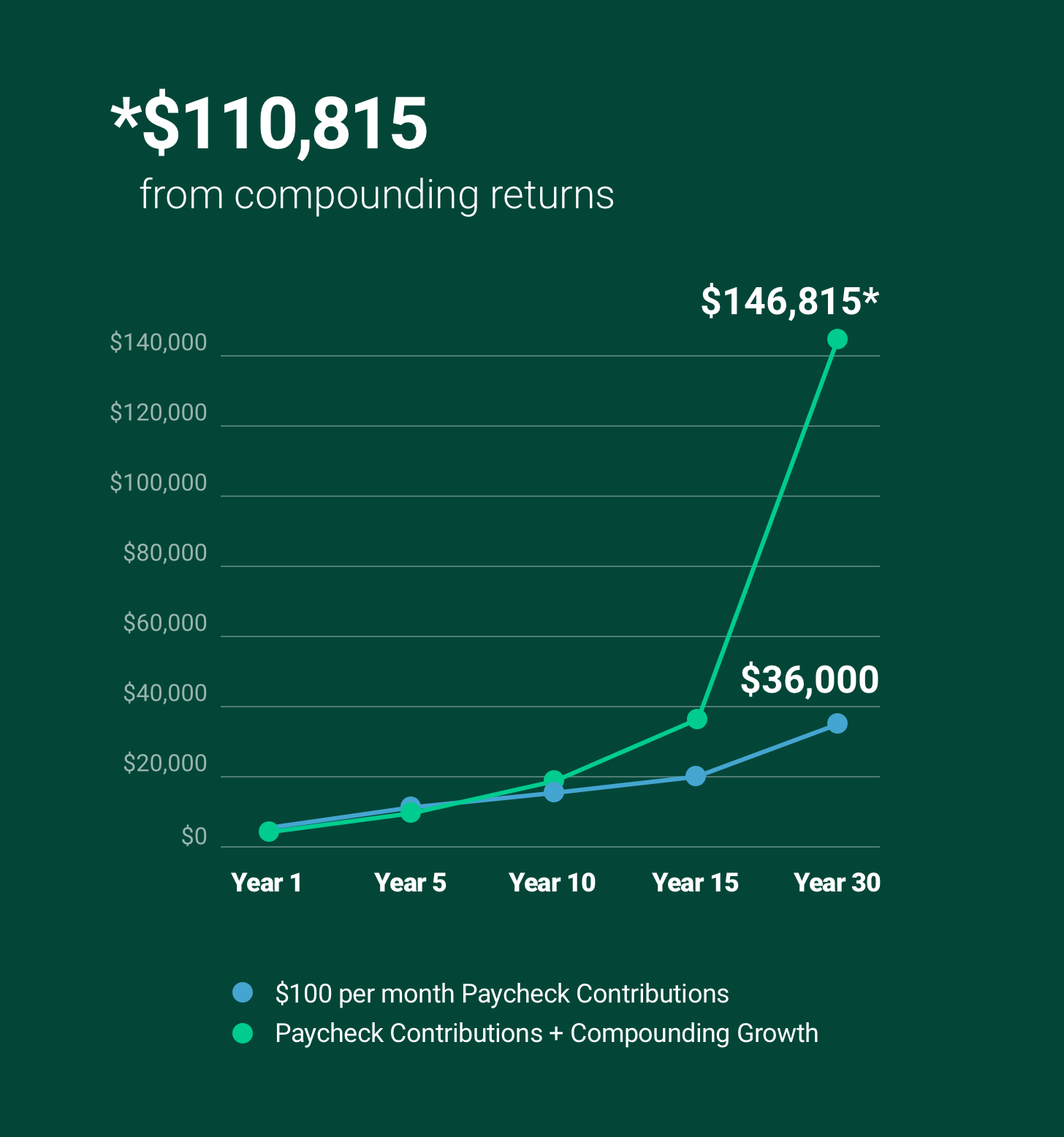

Account growth through compounding

Compounding allows your retirement plan balance to grow faster by combining the power of:

- Time

- Investment Growth

Compounding occurs when the returns generated by your savings are reinvested back into your retirement account and begin generating returns of their own.

Given enough time, compounded returns on your balance can be larger than the contributions you made.

How compounding returns can work for you:

For example, if you contribute $100 per month, after 30 years, your account is valued at $146,815, with only $36,000 being actual contributions from your paychecks!* The rest is from compounding returns by having your money in the market longer.

*Values based on an 8% annual rate of return. Calculations are hypothetical and meant for illustrative purposes only. Investing in securities involves the risk of loss.

Schedule Your Meeting

Schedule a 30-minute one-on-one meeting with a Retirement Specialist by filling out this form.

You can also contact us:

Hours of Operation:

Monday - Friday 5:00am - 5pm PST

(Latest available appointment: 4:15pm)

Thank you for your message. Someone from our team will reach out to you shortly.

888-322-7586 | contact401k@fi.com

©2023 Fisher Investments. Investing in securities involves the risk of loss. Privacy