Fisher Investments UK recommends the portfolio management services of its parent company, Fisher Investments. Fisher Investments UK is a restricted advice firm authorised by the FCA. Fisher Investments is not regulated by the FCA, they are based in the United States and regulated by the SEC. As a result, certain UK retail protections may not be available to clients of Fisher Investments. For more information, see our Regulatory Information page.

As a client of Fisher Investments, you will receive a tailored portfolio we believe is appropriate to help reach your investment goals, managed with an investment practise deeply rooted in time-tested processes and philosophies. Fisher Investments’ portfolio management approach—combined with proactive, personalised client service—has allowed the firm to manage portfolios for more than 40 years. Fisher Investments currently serves over 150,000* clients globally.

Fisher Investments’ Investment Policy Committee (IPC) has over 150 years of combined industry experience. Supported by a large Research Department, the IPC monitors global economic and market conditions and makes strategic investment decisions for client portfolios, an approach based in active, flexible portfolio management. Scroll down to learn more about Fisher Investments’ portfolio management approach and tailored client portfolios.

*As of 31/03/2024. Includes Fisher Investments and its subsidiaries.

Our Approach

Investment Style

Active, flexible and global. Fisher Investments tailors your investment portfolio based on forward-looking market views and capitalises on opportunities around the world, taking into consideration your personal objectives and investment mandates.

Investment Philosophy

Fisher Investments’ investment philosophy is the set of financial principles that guide all investment decisions, rooted in the firm’s belief in capitalism and the power of free markets.

Top-Down Approach

To address the daunting task of selecting from tens of thousands of securities globally, Fisher Investments employs a top-down investment process and leverages a large research team to help make sense of a complex and vast investment landscape.

Tailoring Your Portfolio

Investment success is personal—the management of your assets should be too. Your portfolio deserves more than a one-size-fits-all financial plan. Discover how Fisher Investments builds investment portfolios tailored to each client’s situation and financial goals.

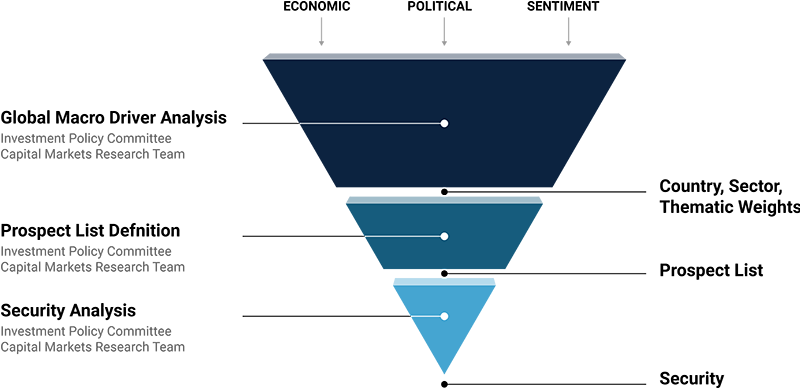

Top-Down Investment Approach

Fisher Investments believes approximately 70% of long-term portfolio returns are attributable to asset allocation, i.e., what mix of equities, fixed interest, cash or other securities you own at any particular time. At the highest level, Fisher Investments’ Research Department gathers a wide range of data inputs, aiding both qualitative and quantitative applications of proprietary capital markets technology. Analysis of current market conditions, history and behavioural factors help enable dynamic tactical asset allocation decisions.

From there, Fisher Investments’ portfolio management teams may seek to emphasise parts of the market they believe will perform best, such as different countries and sectors. Finally, they analyse individual securities and select the ones they believe best capture high-level views. We believe this flexible, active approach to portfolio management enables clients to capitalise on global investing opportunities and help achieve their financial goals.

To determine a portfolio strategy, consistent with your goals and objectives, Fisher Investments UK must understand your complete financial picture as it relates to the assets Fisher Investments will manage. Based on your financial position, we may recommend, where deemed suitable, an asset allocation strategy we feel best fits your particular situation, along with a recommendation for the discretionary investment management services of Fisher Investments.

The Four Elements of a Personalised Investing Approach

Fisher Investments combines experience as a professional portfolio manager with world-class service and state-of-the-art research to help clients meet their long-term goals

-

Personalised

-

Flexible

-

Disciplined

-

Global

Personalised

As you give us more information about your personal portfolio considerations, we will recommend an initial strategic asset allocation based on your specific objectives. We will review this asset allocation with you in detail before your portfolio is invested.

Flexible

Fisher Investments’ approach can help enhance returns and reduce risk by making forecasts and changing asset allocations accordingly. This tactical approach is different from the style of investing in many mutual funds or from money managers who tend to adhere to a static asset allocation and are unwilling or unable to make changes based on market conditions.

Disciplined

Fisher Investments uses a time-tested investment approach that informs the mix of equities, fixed interest and other securities to hold in your portfolio. Fisher Investments first analyses the global macroeconomic environment and market conditions to identify what they think are the most attractive investment categories. Then, they select individual securities within those categories that fit your tailored investment strategy.

Global

Fisher Investments seeks to maximise opportunity and manage risk by investing globally. Many UK investors tend to focus solely on UK equities. However, the UK makes up around 4% of the global equity market.** Investing globally can help take advantage of worldwide opportunities many miss.

**Source: FactSet. MSCI All Country World Index constituents as of 30/06/2022.

The Benefits of Active Portfolio Management

Fisher Investments’ investing style emphasises an active, flexible approach. Whilst passive portfolio management rightly has its supporters, we believe if passive investing was always as easy as it sounds, then everybody would be doing it effectively.

Passive Portfolio Management Has Its Challenges

Yet, being a true passive investor requires extreme discipline that many people often struggle to attain. Investors frequently react emotionally to uncertainty, whether through market volatility or economic, political or personal challenges.

Studies have found that people feel the negative impacts of a loss to a much greater degree than the positive impacts of a gain. This often means that even relatively modest volatility or downturns can lead to investor panic and overreactions to short-term changes by pulling money out of the market and failing to re-enter before it recovers.

Emotional Decision-Making Hampers Passive Investing

Emotion is the downfall of effective passive investment retirement strategies. As soon as you let your feelings drive you into action, you’re no longer a passive investor. Almost inevitably, this subjective bias influences investment decisions, particularly during times of market peaks or troughs.

The Benefits of Active Investment Management

On the other hand, a good active investment manager has the experience and analytical resources needed to help investors avoid investing pitfalls. An active manager like Fisher Investments has a wealth of research and analytical resources to better ensure that your portfolio is positioned to help you meet your financial goals.

Stay Disciplined, Follow the Plan

What many investors need is an asset allocation aligned with their long-term goals. As we’ve discussed, having the discipline to endure the ups and downs of a passive approach is something many struggle with, so it’s also valuable to consider how your investment manager may help prevent you from making a costly error in judgement.

The key with either active or passive investment is to stay disciplined and follow your plan. The difference is that with an active manager, you have someone knowledgeable there to help you steer a steady course when emotions and uncertainty arise.

Helpful Financial Planning Guides

Available at no obligation to you, our ongoing insights offer information on retirement planning, retirement income and more.

Insights & Media

Contact Us

Learn why 150,000 clients* trust Fisher Investments UK and its subsidiaries to manage their money and how we may be able to help you achieve your financial goals.

*As of 31/03/2024

New to Fisher? Call Us.

Contact Us Today