Personal Wealth Management / Market Analysis

An Overlooked Reason Behind July’s Slowing US Inflation

The base effect kicks in.

Editors’ Note: Inflation remains a hot political topic, so please understand that our commentary is intentionally non-partisan and focused on the potential market implications only.

America’s July inflation report made headlines globally this week, with good reason: The US generates about one-fourth of global economic output and represents about two-thirds of the developed-world stock market, making developments in America key worldwide.[i] So when the report revealed that the inflation rate decelerated from June’s 9.1% y/y to 8.5% y/y, we noted much relief amongst financial commentators we follow.[ii] We also saw ample discussion of the deceleration’s causes, with much attention centering on falling petrol and jet fuel prices. Whilst those played a role, we see an additional, widely overlooked explanation, and we think understanding it can help investors set realistic expectations for a big chunk of the global stock market over the period ahead.

That explanation: a mathematical phenomenon called the base effect. The inflation rate, as a year-over-year calculation, measures the percentage change between prices in one month and that same month a year prior. The base is that year-ago price level, which is the denominator in the calculation. As we all learnt in primary school fraction lessons, a higher denominator can result in a smaller quotient—and vice versa. That is what happened in July.

On a month-over-month basis, the Consumer Price Index (CPI, a government-produced measure of broad goods and services prices) was unchanged from June. But prices in July 2021 rose 0.5% from June 2021.[iii] That gives us a constant numerator divided by a larger denominator. Presto, lower inflation rate.

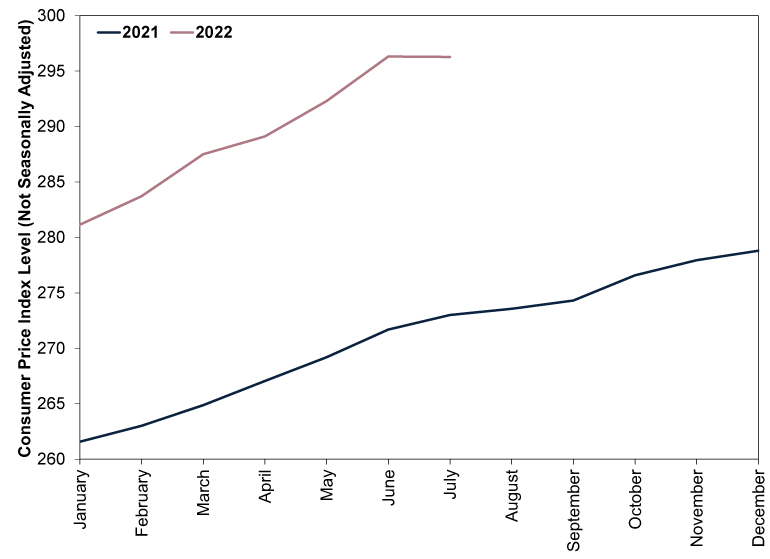

We aren’t pointing this out to talk down the deceleration. Nor do we mean anything political by going here. Rather, we think there is a good chance that the base effect continues having a balancing effect from here. To see the potential, consider Exhibit 1. It shows the US CPI level in 2022 (the numerators) and 2021 (the denominators). As you will see, prices’ autumn 2021 rise will raise the calculation base over the rest of this year. Then, as we head into 2023, early 2022’s sharp rises will move into the denominator, potentially adding more disinflationary maths.

Exhibit 1: The CPI Base Effect, Deconstructed

Source: St. Louis Federal Reserve, as of 10/8/2022.

Hence, even if month-over-month price changes don’t remain at zero from here, America’s inflation rate could still moderate. We saw this, to an extent, in core inflation, which excludes food and energy prices, in July. On a month-over-month basis, core prices rose 0.3%, matching the long-term average.[iv] But the year-over-year core inflation rate stayed at 5.9%, matching June’s reading.[v] The rising denominator simply cancelled out the numerator’s wiggle.

This is encouraging, in our view, because month-over-month price moves appear highly unlikely to stay at zero from here, much less dip negative for a long stretch. After all, it isn’t like American prices stabilised across the board in July. That flat month-over-month headline rate stems from a bunch of goods and services’ offsetting energy prices’ -4.6% m/m fall.[vi] That category is notoriously bouncy, which is a big reason the core measure exists. Beyond that, the most likely scenario to us has always been that after the US economy swallowed this year’s big price moves—once energy costs, shortages and shipping bottlenecks worked their way through the system—prices would probably grow more slowly off a higher base. We think July is a real-time example of what this would look like.

Not that America’s inflation rate has peaked, mind you. Inflection points are only clear with a good amount of hindsight. We are also keenly aware that much of this discussion doesn’t apply in Britain, given the household default energy tariff price cap’s semiannual rise has a large effect on UK inflation data. Several economists we follow project another large increase in October, likely making the base effect less of a factor in the UK in the near term.

But in our experience, global markets tend to look beyond even stiff headwinds in one country, making it important for investors to consider economic drivers globally. To that end, July’s US inflation results show that even with volatility from month to month, the base effect there can still stabilise the headline rate enough to help sentiment toward US stocks improve. That is primarily what matters from an investing standpoint, in our view. Inflation was one of the biggest factors weighing on sentiment during this year’s stock market downturn based on financial publications we monitor, and it hit US stocks disproportionately.[vii] From a fundamental standpoint, we think businesses and the economy are equipped to stomach higher prices, considering American consumer spending has continued growing on an inflation-adjusted basis this year.[viii] But we have found sentiment and reality often veer, creating room for inflation improvement in the US to be a tonic toward American stocks even if it doesn’t represent much for the US economy at a fundamental level.

[i] Source: World Bank and FactSet, as of 10/8/2022. Statement based on US and global gross domestic product, which is a government-produced measure of economic output, and the market capitalisation of the MSCI World Index and its constituent countries. Market capitalisation is a measure of a company’s or stock index’s total value, calculated by multiplying share price times total shares outstanding.

[ii] Source: FactSet, as of 10/8/2022.

[iii] Ibid.

[iv] Ibid.

[v] Ibid.

[vi] Ibid.

[vii] Ibid. Statement based on MSCI World Index return with net dividends and S&P 500 total return in USD. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[viii] Source: US Bureau of Economic Analysis, as of 10/8/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-07

-

Macro Insights The Danger of Chasing Investor Flows2026-08-05

-

Market Analysis A Market-Orientated Perspective on the EU’s Low Summertime Gas Storage Levels2026-08-03

-

Economics On Fires and GDP2026-07-31

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today