Personal Wealth Management / Market Analysis

A Look Around the World at Manufacturing Surveys Entering 2023

Heavy industry’s slump isn’t news for stocks, in our view.

The New Year is officially underway, but 2022 still lingers on in a sense, as December’s economic data are only just starting to come out. First up: The business surveys known as Manufacturing Purchasing Managers’ Indexes (PMIs), which showed factories worldwide finished the year on a poor note—which didn’t surprise economists, based on the consensus expectations compiled by FactSet.[i] Manufacturing’s troubles have been well-documented throughout financial commentary we follow, but our research suggests heavy industry is uniquely vulnerable to last year’s biggest headwinds. The potential silver lining? With those headwinds widely known and now, in our view, starting to fade, we think global markets could be poised to begin pricing in an economic recovery much sooner than commentators we follow have stated is likely.

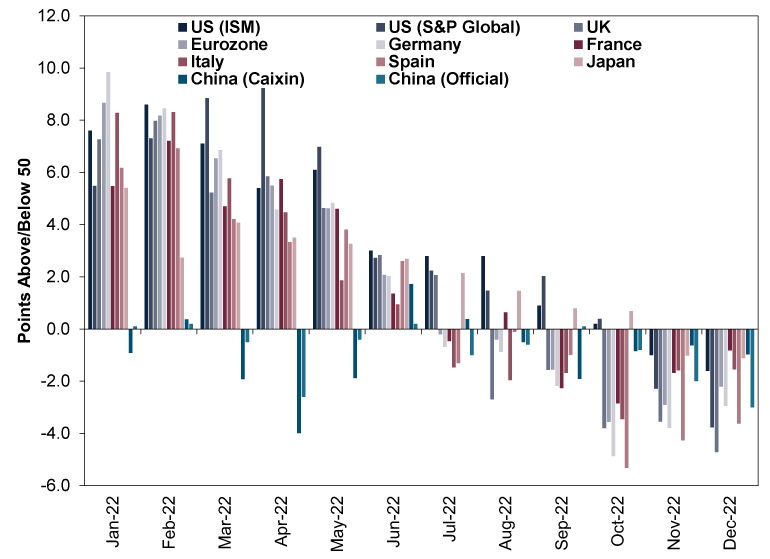

Exhibit 1 rounds up the major manufacturing PMIs. As you will see, all remained under 50—the dividing line suggesting more respondents reported contraction than growth. That extends the trend that materialised around midyear.

Exhibit 1: Around the World in Manufacturing PMIs

Source: FactSet, as of 4/1/2023. S&P Global Manufacturing PMIs for the US, UK, eurozone, Germany, France, Italy, Spain and Japan; Institute for Supply Management (ISM) Manufacturing PMI for the US; Caixin and National Bureau of Statistics of China official Manufacturing PMIs for China, January 2022 – December 2022.

In our view, geographic trends highlight the causality. China started and ended the year weak, which we think was due first to the continuation of its Zero-COVID policies and then, as the year closed, the big COVID wave that followed the easing of most restrictions.[ii] It is increasingly an outlier globally, but we think it will probably come back in line with the rest of the world later this year as it moves past the winter COVID surge. In the developed world, the UK and eurozone were first to slip into contraction, which we think ties to their comparatively higher energy costs.[iii] Manufacturing is quite energy-intensive, so factory output can be especially susceptible to rising power prices.[iv] Germany unsurprisingly suffered the most, since natural gas is a key feedstock for its mighty chemical industry, hitting it disproportionately as natural gas prices surged after the West’s response to Russia’s Ukraine invasion hit supply in the eurozone.[v] But by yearend, all major developed economies’ manufacturing sectors were in contraction, likely hit by higher operating costs and input prices as well as reduced demand from clients that had their own issues trying to deal with inflation.[vi]

That is all the bad news—and we think it is all backward-looking. Stocks, however, look out to the next 3 – 30 months, in our view. In that stretch, we think the issues that hampered factories as 2022 wound down look highly likely to improve. Energy costs are down—way down—with even benchmark European natural gas prices below pre-invasion levels.[vii] Natural gas shortages didn’t erupt during recent cold snaps, which suggests to us the likelihood of rationing and factory outages in Europe has fallen.[viii] In the US, lower petrol prices mean lower transit costs, enabling more goods to move around the country.[ix] Commodity prices are down across the board.[x] Per the PMIs, input and output price increases have continued moderating significantly.[xi] Forward-looking inflation indicators we track—chiefly, slowing in broad money supply growth—suggest that may continue.[xii] Meanwhile, loan growth remains resilient across the developed world, suggesting to us households and businesses should have plenty of capital to deploy as their inflation concerns ease.[xiii]

We know this doesn’t square with much of the economic pessimism dominating headlines, evident once again in the International Monetary Fund’s (IMF) latest comments about one-third of the world being in decline, not to mention the drumbeat of surveys showing recession is the baseline forecast amongst economists globally.[xiv] But that is our point. In our view, markets move most on the gap between expectations and reality over the foreseeable future. Based on all the surveys showing economists and business leaders—not to mention consumers—think a recession is likely, expectations are quite low, but we think it is because people are extrapolating the current weakness forward.[xv] But the indicators we consider forward-looking currently suggest some improvement is in the offing, even in the areas seemingly hit hardest by last year’s dynamics—improvement that doesn’t seem to be factored into sentiment right now. Seems to us like there is a lot of room for positive economic surprise to benefit stocks.

When that will happen, we can’t say. It may already have begun in mid-June. In our view, turning points are clear only in hindsight. Maybe stocks move well in advance of any notable improvement in the data, or maybe there is further downside ahead if data stay bad a bit longer. After a year in which we think markets seemed to dwell on bad news much more than good, who can say when that preoccupation with the negative will flip. But looking purely at the economic driver, we see much more positive surprise potential ahead than negative. At some point, if markets are at all efficient, we think that should eventually show up in prices.

[i] Source: FactSet, as of 4/1/2023. Purchasing Managers’ Indexes are monthly surveys that track the breadth of economic activity; readings above 50 indicate expansion, below 50, contraction.

[ii] “Xi Jinping Estimates China’s 2022 GDP Grew At Least 4.4%. But Covid Misery Looms,” Laura He, CNN, 2/1/2023.

[iii] Source: FactSet, as of 4/1/2023. Statement based on Dutch TTF Gas Price in EUR and GBP, 1/8/2022 – 4/1/2023.

[iv] Source: Office for National Statistics, as of 4/1/2023. Statement based on Energy Use by Industry, Source and Fuel, June 2022.

[v] “Russia Is Giving German Industry a Slow Puncture,” George Hay, Reuters, 27/7/2022. Accessed via Nasdaq.com.

[vi] See note i.

[vii] Source: FactSet, as of 4/1/2023. Statement based on Dutch TTF Gas Price in EUR, 23/2/2022 – 4/1/2023.

[viii] “National Grid: Coal Plants Stood Down to Supply Electricity,” Michael Race & Dearbail Jordan, BBC, 12/12/2022.

[ix] “Gas Prices Tumble to 15-Month Low. Sub-$3 Could Be Next,” Matt Egan, CNN Business, 16/12/2022.

[x] Source: FactSet, as of 4/1/2023. Statement based on S&P GSCI Index – All Metals and S&P GSCI Index – Agriculture, 4/12/2022 – 4/1/2023.

[xi] See note i.

[xii] Source: US Federal Reserve, as of 4/1/2023.

[xiii] Source: US Federal Reserve, European Central Bank, Bank of Japan and Bank of England, as of 4/1/2023.

[xiv] “Third of World Economy to Hit Recession in 2023, IMF Head Warns,” Staff, The Guardian, 2/1/2023. A recession is a period of contracting economic output.

[xv] Source: FactSet, Bloomberg and Bank of America, as of 4/1/2023. University of Michigan Survey of Consumers – Business Conditions Expected During the Next Year, ZEW Eurozone Financial Market Survey and Bank of America Global Fund Manager Survey, December 2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-07

-

Macro Insights The Danger of Chasing Investor Flows2026-08-05

-

Market Analysis A Market-Orientated Perspective on the EU’s Low Summertime Gas Storage Levels2026-08-03

-

Economics On Fires and GDP2026-07-31

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today