Personal Wealth Management / Economics

A Look at US GDP’s First-Half Dip—and Beyond

Stocks are the best leading indicator, in our view, and what matters to them is ahead—not behind.

Q2 US Gross Domestic Product (GDP, a government-produced measure of domestic economic output) fell -0.9% annualised, its second consecutive quarterly decline after Q1’s -1.6% dip.[i] Because this is one traditional definition of recession (broad, extended period of economic contraction)—although not the official way America defines it—headlines we read feverishly debate whether this means one is now underway. And, with US GDP about a quarter of the world’s, they discuss what it augurs for the global economy.[ii] But in our view, that debate is too backward-looking for investors to mind it much. Months-old economic activity has little relevance for stocks, which we think have already dealt with the mild economic contraction and are looking ahead to what the next 3 to 30 months have in store relative to expectations.

Our research shows stocks move ahead of economic activity, and bear markets (typically prolonged, fundamentally driven declines exceeding -20%) often precede recessions as stocks discount the likely decline in investment and corporate earnings. We think this year’s shallow (to date) US and global bear market (when defined in US dollars) would be pretty consistent with a shallow recession.[iii] But whether or not one is underway is questionable. America’s National Bureau of Economic Research (NBER), which is the US’s official arbiter, doesn’t define a recession as two sequential GDP contractions. Rather, it defines it as a “significant decline in economic activity that is spread across the economy and lasts more than a few months.”[iv] Diving under the bonnet of Q2’s GDP report, we think there are reasons to question whether the US economy meets that threshold.

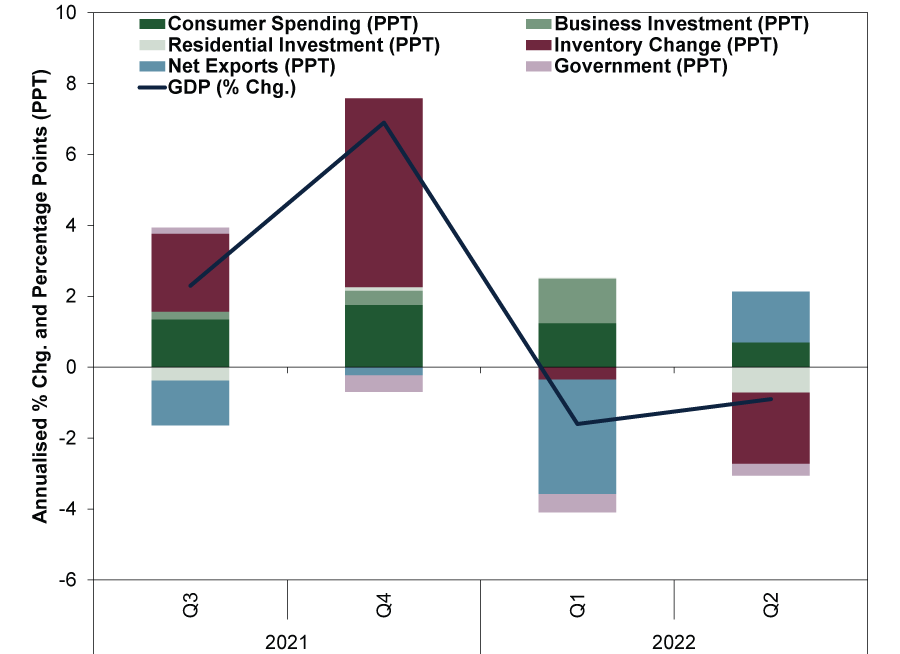

Exhibit 1 breaks out the US’s net trade (exports minus imports, light blue columns) and inventories (burgundy) by their contribution to headline growth (dark blue line). It also shows America’s government spending contribution (lavender) and three major GDP components: consumer spending (71% of GDP), business investment (15%) and residential investment (3%) in shades of green.[v]

Exhibit 1: US GDP Breakdown

Source: FactSet, as of 28/7/2022. US GDP and components, Q3 2021 – Q2 2022.

In Q1, whilst trade subtracted heavily as imports (which reflect domestic demand) jumped, US consumer spending and business investment remained nicely positive. In Q2, trade added to US GDP—exports rose more than imports—but inventories’ big subtraction more than offset it. This could be a delayed giveback from Q4’s huge inventory surge, presuming it stays in the data. In Q1, the US Bureau of Economic Analysis (BEA) initially reported inventories subtracted -0.84 percentage point (ppt) from headline growth.[vi] But the BEA substantially reduced that in later revisions to the tiny detraction shown in Exhibit 1. Q2’s report similarly faces several rounds of revision from here.

Regardless, we think inventories are always open to interpretation. A reduction could mean demand outstripped supply, or it could mean businesses had to clear a supply glut. The latter seems more likely to us. All last quarter, major retailers reported heavy discounting to clear inventory overhangs.[vii] It is possible Q4’s huge holiday stocking met with ongoing supply chain uncertainty in Q1 to keep reductions at bay, but as bottlenecks started to ease in Q2, managers felt more comfortable letting inventories run off.

Elsewhere, consumer spending rose 1.0% annualised, a slowdown, whilst fixed investment fell -3.9%, shaving -0.72 ppt off headline growth.[viii] This has many commentators we follow warning the downturn is more than just temporary supply-chain-related hiccups. The investment drop, however, was almost entirely residential real estate.[ix] Whilst it took a chunk out of GDP last quarter as new home sales stalled, residential real estate is a sliver of the total US economy.[x] No surprise many homebuyers got cold feet from rising mortgage rates, which could persist near term.[xi] But with new homes under construction hitting record levels, affordability could improve in time.[xii]

Meanwhile, business investment, which our research shows is usually recession’s swing factor, declined -0.1% annualised, subtracting a miniscule -0.01 ppt from headline growth.[xiii] Now, we don’t think flattish capital expenditures are a resounding economic confidence booster. Coupled with the inventory decline, it could signal businesses are getting lean and presage investment decreasing further. But we hesitate to draw that huge of a conclusion from a single-quarter’s minute dip.

So although the US’s Q2 was mixed, does it constitute a recession? NBER’s eight-member business cycle dating committee will officially decide, but it will only be in hindsight—and likely far into the rear view by the time it does. In the meantime, others are free to choose their narratives.

For (in our view) forward-looking markets, though, we find recession calls are of little relevance. We don’t think it is very helpful to get caught up in after-the-fact refereeing when stocks have long since moved on. GDP reports are a backward look at what markets have already anticipated, in our view—declaring a recession based on them, or any other measure, is even more backward looking.

Whatever commentators dub it, the greater than -20% stock market decline from January’s highs through mid-June in US dollars suggests to us a substantial amount of economic weakness is reflected in stocks already.[xiv] We think what matters from here is how things go relative to expectations. A deep, lasting recession could mean stocks have more negativity ahead. But, whilst possible, it isn’t necessarily probable. The 10-year to 3-month US Treasury yield curve—a key leading economic indicator, in our view—remains positively sloped, and even if the US Federal Reserve continues hiking short-term rates and it inverts, that isn’t necessarily a trigger or harbinger, in our view. We think this is because banks’ deposit rates—their funding costs for new loans—remain close to zero, keeping new lending profitable with long-term rates higher than 10-year Treasury yields.[xv] Moreover, whilst it is backward-looking relative to the yield curve, through mid-July, loan growth has accelerated to 10.5% y/y, its highest rate in over a decade (excluding pandemic lockdown emergency lending), which isn’t what you typically see in or entering recession.[xvi]

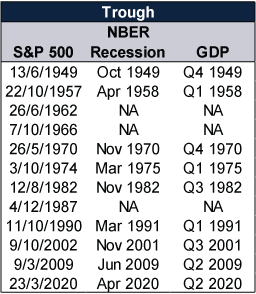

In any event, we think stocks are a leading economic indicator, too. They can be volatile—as the economist Paul Samuelson once observed, “the stock market has predicted nine out of the last five recessions.”[xvii] But more often than not, as Exhibit 2 illustrates, the market has turned higher well before GDP does. (Note the exception in 2002: Based on our analysis, US stocks’ ultimate low came long after the recession ended as heavy-handed new US financial regulations slammed them anew.) So in our view, nothing in stocks’ upturn since 16 June is inconsistent with the US enduring a shallow recession.[xviii] It may be, though we can’t know for sure, that stocks are moving on to pricing in an economic recovery ahead.

Exhibit 2: The US’s Stock Market Usually Troughs Before Its GDP

Source: FactSet and NBER, as of 28/7/2022. S&P 500 price index, 1/1/1947 – 28/7/2022, NBER business cycle trough dates and US GDP, Q1 1947 – Q2 2022. S&P 500 trough dates are presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns, potentially shifting the dates of market lows.

[i] Source: US BEA, as of 28/7/2022. GDP, Q2 2022.

[ii] “World Economic Outlook,” IMF, April 2022.

[iii] Source: FactSet, as of 29/7/2022. Statement refers to S&P 500 and MSCI World returns from 3/1/2022 – 16/6/2022 and 4/1/2022 - 17/6/2022, respectively. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[iv] “Business Cycle Dating Procedure: Frequently Asked Questions,” NBER, 19/7/2021.

[v] Source: US BEA, as of 28/7/2022. Personal consumption expenditures, non-residential fixed investment and residential fixed investment as a percent of GDP, Q2 2022.

[vi] Source: US BEA, as of 28/4/2022. Change in private inventories, advance estimate, Q1 2022.

[vii] “Stores Have Too Much Stuff. Get Ready for Discounts,” Nathaniel Meyersohn, CNN, 27/5/2022.

[viii] Source: US BEA, as of 28/7/2022. Personal consumption expenditures and private fixed investment, Q2 2022.

[ix] Source: US BEA, as of 28/7/2022. Residential fixed investment, Q2 2022.

[x] See note iv. “New Home Sales Decrease Sharply, Record Months of Unsold Inventory Under Construction,” Bill McBride, Calculated Risk, 26/7/2022.

[xi] “Pending Home Sales Fell 20% in June Versus a Year Earlier as Mortgage Rates Soared,” Diana Olick, CNBC, 27/7/2022.

[xii] Source: US Census Bureau, as of 19/7/2022. New privately‐owned housing units under construction, June 2022.

[xiii] Source: US BEA, as of 28/7/2022. Non-residential fixed investment, Q2 2022.

[xiv] Source: FactSet, as of 28/7/2022. S&P 500 total return, 3/1/2022 – 16/6/2022. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[xv] Source: US Federal Reserve Bank of St. Louis, as of 28/7/2022. Statement based on national deposit rates for interest checking and savings accounts, money markets and 12-month CDs, July 2022, and bank prime loan rate, 27/7/2022.

[xvi] Source: US Federal Reserve Bank of St. Louis, as of 28/7/2022. Total loans and leases in bank credit, 13/7/2022.

[xvii] “Science and Stocks,” Paul Samuelson, Newsweek, 19/9/1966.

[xviii] Source: FactSet, as of 28/7/2022. S&P 500 total return, 16/6/2022 – 28/7/2022. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights The Danger of Chasing Investor Flows2026-08-05

-

Market Analysis A Market-Orientated Perspective on the EU’s Low Summertime Gas Storage Levels2026-08-03

-

Economics On Fires and GDP2026-07-31

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today