Personal Wealth Management / Market Analysis

More Evidence We Think a Recession Wouldn't Shock Now

When this many CEOs, fund managers and economists see imminent downturn, surprise power is minimal, in our view.

On the heels of December’s dim manufacturing purchasing managers’ indexes (PMIs), services and composite PMIs showed contraction in many of the world’s major economies.[i] (PMIs are monthly surveys that track the breadth of economic activity as companies report a yes or a no to their company growing or contracting. Readings above 50 indicate expansion, whilst below 50 indicates contraction.) Perhaps services’ contraction is less broad-based than manufacturing, given their readings are closer to 50.[ii] Yet most are still below, suggesting contraction. That said, as we wrote last week, we think what likely matters to stocks looking forward isn’t whether economies shrink, but whether any recession (a decline in broad economic output) is a surprise or surprisingly nasty. A quick tour of the latest surveys of economists, CEOs and fund managers shows recession is a popular forecast this year, suggesting negative surprise power is quite limited.

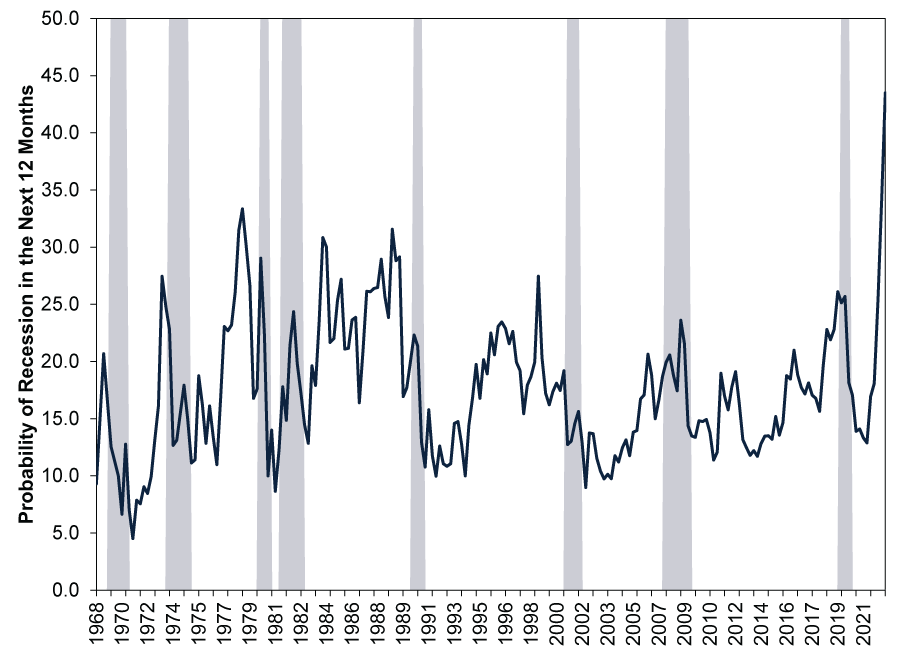

Take survey results in the US for example. The US Federal Reserve Bank of Philadelphia’s (Philly Fed’s) quarterly survey of professional forecasters tracks a few dozen economists’ gross domestic product (GDP, a government-produced measure of economic output) growth projections for the US for the next several quarters. From their forecasts, the Philly Fed calculates the mean probability of US GDP growing (or contracting) at a given rate. In Q4, economists put the mean probability of a US recession occurring within the next 12 months at 43.5%. That is the highest estimated probability in the series’ history, which begins in 1968.

Exhibit 1: Philly Fed Survey of Professional Forecasters

Source: Federal Reserve Bank of Philadelphia, as of 5/1/2023. Shaded areas indicate recessions as tabulated by America’s National Bureau of Economic Research.

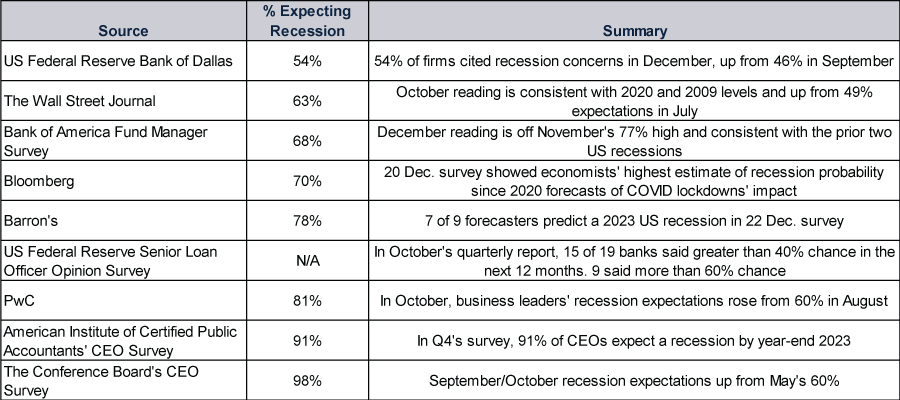

Exhibit 2 collates a number of other, similar surveys—all showing business leaders, economists and professional investors see a very high likelihood of recession in the US this year.

Exhibit 2: Major Surveys at a Glance

Source: US Federal Reserve Bank of Dallas, The Wall Street Journal, Bank of America, Bloomberg, Barron’s, Federal Reserve, PwC, AICPA and The Conference Board, as of 29/12/2022. Note: The US Federal Reserve’s Senior Loan Officer Opinion Survey doesn’t normally include questions about recession. But researchers elected to include a special set of questions on recession in October, which, in our view, illustrates just how front-of-mind recession worries are presently.

In our view, there are a couple encouraging things to glean from this. One, perhaps most obviously, if a recession strikes in the US or elsewhere, it isn’t likely to be a broad-based surprise. Not to the pros, not to the masses and likely not to stocks, which we think are well aware of these surveys and what they represent. In our view, stocks quickly discount widely known information, so they have probably already incorporated these projections into current prices. We think that probably has a lot to do with the global stock market decline that began just over a year ago.[iii] Therefore, if a recession becomes official in the US or elsewhere, far from being a shocking bad thing that stocks will have to grapple with, we suspect it would just confirm whatever they already priced in. In our experience, events like that tend to ease uncertainty and help stocks move on.

Two, from our observations of business leaders, they tend not to just sit on their hands and wait for economic data to confirm recession. Rather, we have long observed that falling stock prices, weak earnings projections and widespread recession forecasts usually create an incentive for businesses to get lean and mean to survive whatever bad times could lie ahead. In our view, a recession’s general purpose is to wring out accumulated excess—and our historical research shows the more wringing, the deeper and longer they tend to last. But this time, we are already seeing a lot of those cuts—witness all the recent layoff announcements from large American companies, many of which include plans to cut real estate holdings and investments.[iv] If companies are getting lean and mean now, we think that suggests there wouldn’t be much more to trim by the time US recession becomes official—if it becomes official (based on the National Bureau of Economic Research’s criteria and declarations)—which, in our view, speaks to it probably being short and shallow. We think that also argues for stocks having pre-priced this risk.

[i] Source: FactSet, as of 10/1/2023. Statement based on S&P Global Services and Composite PMIs for the US, the UK, eurozone, Germany, France, Italy, Japan and China; Institute for Supply Management (ISM) Services PMI for the US, Caixin and National Bureau of Statistics of China official Services and Composite PMIs for China, December 2022.

[ii] Ibid.

[iii] Source: FactSet, as of 10/1/2023. Statement based on MSCI World Index return with net dividends in GBP, 8/12/2021 – 9/1/2023.

[iv] “Salesforce’s 10% Staff Cut Highlights Slowdown in Tech Spending,” Brody Ford, Bloomberg, 4/1/2023. Accessed through Yahoo! Finance.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-07

-

Macro Insights The Danger of Chasing Investor Flows2026-08-05

-

Market Analysis A Market-Orientated Perspective on the EU’s Low Summertime Gas Storage Levels2026-08-03

-

Economics On Fires and GDP2026-07-31

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today