Personal Wealth Management / Market Analysis

Oil’s OPEC+ Plus Sign Probably Not Assured to Last

We think markets have seen this before.

After the Organization of the Petroleum Exporting Countries and its partners (collectively known as OPEC+) announced a surprise production quota cut Sunday, crude oil prices jumped on Monday, and commentators we follow raised inflation concerns once again.[i] Most commentary we read focussed on the scale of crude’s intraday rise. But even with Monday’s price movement, crude prices remained below levels seen at this point last month—and well off last year’s highs.[ii] Couple that with OPEC’s recent failures to meet quotas, and we are struggling to see why some seem so worried.[iii] In our view, this looks much more like a scare story—which our research finds are abundant early in bull markets (long periods of generally rising equity prices)—than a fundamental reason for stocks to tumble to new lows from here.

When OPEC+ nations get together, they theoretically assess global demand, production in the US and other non-cartel nations, and then set production targets at a level they anticipate will balance supply and demand. In October, they caused a stir amongst commentators we follow by announcing voluntary cuts that would reduce production by 2 million barrels per day (bpd) beginning in November and lasting through 2023.[iv] Prices bounced higher initially … then fell.[v] Sunday’s announcement added another voluntary 1.66 million bpd reduction, which includes Russia’s plans to cut output by 500,000 bpd in the face of tighter Western sanctions.[vi] OPEC+’s announcement states these cuts are “aimed at supporting the stability of the oil market.”[vii] But most coverage we observed portrayed this as the cartel piling production cuts on top of production cuts in an attempt to boost crude prices. We think that rhetoric, coupled with Brent crude’s nearly $5 jump on Monday, resurrected inflation worries.[viii]

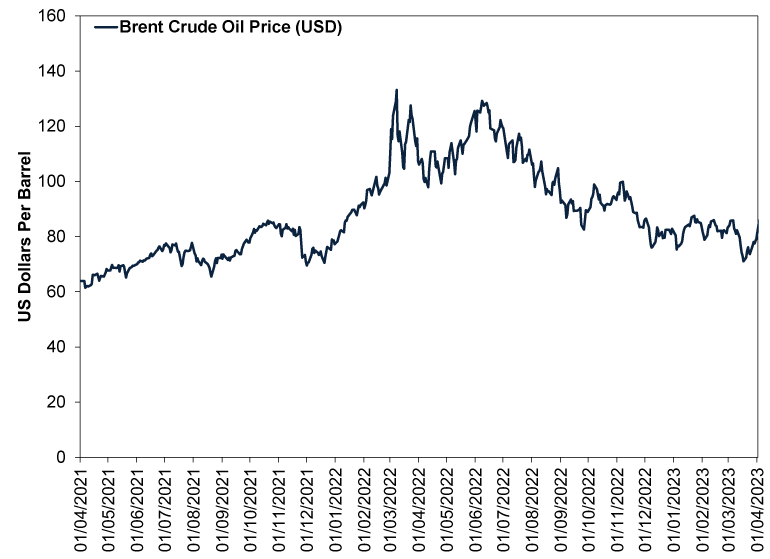

In our view, this is all a bit hasty. For one, even with Monday’s jump, crude is down significantly from 2022.[ix] Prices closed Monday well below their spike after October’s production cut announcement.[x] Then, Brent crude temporarily flirted with $100 per barrel before falling in November and December.[xi] It closed Monday around $85, in line with prices throughout December, January and February, and hovered around there through Wednesday.[xii] If energy prices then were disinflationary, we don’t see why they would suddenly be some massive consumer price booster now.

Exhibit 1: Oil Is Still Down

Source: FactSet, as of 4/4/2023. Brent crude oil price in USD, 3/4/2021 – 3/4/2023.

Maybe oil prices soar from here, but we rather doubt it. We have observed a pretty solid history of OPEC+ making widely watched announcements, markets reacting one way immediately, then reverting to extant trends as global supply and demand come back into focus. On that front, we don’t think OPEC+’s quotas are as meaningful as many commentators we follow allege. For one, the US and other non-members produce the majority of global crude, diminishing OPEC+’s power over supply.[xiii] Production in the US, Brazil and elsewhere continues rising, and most forecasts we have seen project rising global supply this year despite OPEC+’s machinations.[xiv]

Two, the cartel and its partners haven’t exactly hit their quotas to begin with. October’s cuts put the production target at about 41.36 million bpd for November onward. In October, the participants’ collective output was 38.47 million bpd.[xv] It inched a tad lower in November to 38.8 million bpd and slipped again to 37.68 million bpd in December.[xvi] But it crept back up to 38.05 million bpd in January and 38.1 million bpd in February.[xvii] Overall, the drop is nowhere close to 2 million bpd. From our perspective, the only thing that has changed is that because the quota is lower, the minimally changed output undershoots the target by a smaller amount. The gap between output and the quotas simply narrowed from 3.63 million bpd in October to just over 2 million in February.[xviii] Cutting the target again likely just brings it even closer to where actual output is.

Accordingly, we think it seems rather unlikely OPEC+’s move causes inflation to rocket higher from here. Even slightly higher crude prices in the immediate future would be down big from their year-ago comparison points, making them a deflationary CPI component.[xix] Meanwhile, businesses have likely already swallowed last year’s energy cost increases, factored them into their costs and sales prices, and moved on. Fisher Investments Founder and Executive Chairman Ken Fisher often likens last year’s inflation to a large rodent that a snake ate and then digested slowly—picture a lump slowly pulsing through. It took a while, but by this point, most of last year’s big inflation drivers have worked their way through the system, and eased tremendously. Energy is down.[xx] Shipping conditions and costs have eased.[xxi] Supply shortages are evening out.[xxii] Money supply throughout the developed world is slowing or even falling, depending on the measure you use.[xxiii]

In our experience, investors have a long history of fighting the last war, meaning they are on high alert for a repeat of the negative developments they think drove the most recent market downturn. In the early 2010s, we saw many on high alert for a new financial crisis—some still are, as last month’s regional bank failures suggest. In 2020 and 2021, we saw many commentators watching for new lockdowns roiling economies. Now an inflation repeat seems front of mind. In our view, this is a sign of sentiment, and it is what we would anticipate in a young bull market—it is a big part of what builds the wall of worry. In our view, the more people look high and low for signs of resurgent inflation—sapping its surprise power—the more this looks like a new bull market.

[i] Source: FactSet, as of 4/4/2023. Brent crude oil spot price in USD, 31/3/2023 – 3/4/2023. Inflation refers to broadly rising prices across the economy.

[ii] Ibid. Brent crude closed at $84.87 Monday versus $85.73 on 3 March 2023. It peaked over $130 last year.

[iii] “OPEC Misses Production Quota By 310,000 Bpd,” Julianne Geiger, Oilprice.com, 9/12/2022.

[iv] “OPEC+ To Cut Oil Production by 2 Million Barrels Per Day to Shore Up Prices, Defying U.S. Pressure,” Sam Meredith, CNBC, 5/10/2022.

[v] Source: FactSet, as of 4/4/2023. Brent crude oil spot price in USD, 5/10/2022 – 18/10/2022.

[vi] Source: OPEC, as of 4/4/2023.

[vii] Ibid.

[viii] See note i.

[ix] Source: FactSet, as of 4/4/2023. Brent crude oil spot price in USD, 30/12/2022 – 4/4/2023.

[x] Ibid. Brent crude oil spot price in USD, 5/10/2022 – 3/4/2023.

[xi] Ibid.

[xii] Ibid.

[xiii] Source: US Energy Information Administration, as of 4/4/2023.

[xiv] Source: US Energy Information Administration and International Energy Agency, as of 4/4/2023.

[xv] Source: Argus Media, as of 3/4/2023.

[xvi] Ibid.

[xvii] Ibid.

[xviii] Ibid.

[xix] Source: FactSet, as of 4/4/2023. Brent crude oil spot price in USD, 4/4/2022 – 4/4/2023. The consumer price index, or CPI, is a government-produced index tracking prices of commonly consumed goods and services.

[xx] Source: FactSet, as of 4/4/2023. MSCI World Energy Index return with net dividends, 30/12/2022 – 4/4/2023.

[xxi] Source: New York Federal Reserve and St. Louis Federal Reserve, as of 4/4/2023. Global Supply Chain Pressure Index and Producer Price Index for General Freight Trucking, Deep Sea Freight and Air Freight, January 2022 – February 2023.

[xxii] Source: US Institute for Supply Management, as of 4/4/2023. Manufacturing purchasing managers’ index, January 2022 – March 2023.

[xxiii] Source: Federal Reserve, European Central Bank, Bank of Japan, Bank of England and Reserve Bank of Australia, as of 4/4/2023.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

-

Market Analysis Reviewing America’s Q1 Earnings and What Q2 Expectations Say2026-06-23

-

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-23

-

Macro Insights SpaceX IPO and Rising Equity Supply2026-06-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today