Personal Wealth Management / Economics

UK GDP Tells a Well-Known Story

Whilst GDP reports grab attention, they are old news to equities, in our view.

UK gross domestic product (GDP, a government-tallied measure of economic output) just registered its fastest monthly growth rate since July 2020.[i] Yet the nation’s recovery still trails many major developed economies, according to the Organisation for Economic Co-operation and Development (OECD)—and the outfit also warned domestic developments (e.g., Brexit) may hurt future growth.[ii] Whilst the latest GDP figures and projections tend to grab eyeballs, we think they are old news to markets—a point investors benefit from keeping in mind, in our view.

GDP rose 2.3% m/m in April thanks to the services sector’s 3.4% growth.[iii] COVID restrictions eased throughout the month, and the data confirm as much, as consumer-facing services (e.g., retail trade, travel and transport, and entertainment and recreation) jumped 12.7% m/m.[iv] Other people-facing services categories surged, including accommodations (68.6% m/m), food and beverages (39.0%) and other personal service activities, which include hairdressing (63.5%).[v] Education—the second-biggest contributor to growth behind wholesale and retail trade—rose 11.2% m/m and added 0.72 percentage point to GDP growth as more students returned to the classroom in person.[vi]

Services is nearly 80% of UK GDP, so strong growth there was more than enough to offset contractions in the other two major sectors, production (which includes manufacturing as well as mining and oil extraction) and construction.[vii] They contracted -1.3% m/m and -2.0%, respectively.[viii] Yet that weakness appears to be temporary, as mining’s -15.0% m/m decline stemmed from planned temporary maintenance closures at oil production sites.[ix]

Financial commentators we follow anticipate output improving further in May given reopening progress.[x] However, the broader summertime recovery may be a tad slower than many outlets initially projected, as Prime Minister Boris Johnson just delayed England’s full reopening from 21 June to 19 July, and Scotland may soon do the same.[xi] Short-term speedbumps aren’t new for the UK, which has trailed other major developed economies after suffering the biggest decline from pre-pandemic levels amongst all Group of 20 countries, according to a headline-grabbing OECD report.[xii] The latest news may also seem to validate a separate OECD missive, which warned COVID-related setbacks and trade frictions with the EU post-Brexit could lead to permanent economic damage.[xiii] We see some reasons to take these warnings with a grain of salt, however.

According to the UK’s Office for National Statistics (ONS), several factors may explain why UK GDP fell harder than other countries’ during the pandemic.[xiv] For one, COVID restrictions, by their nature, disproportionately affect social consumption activities (e.g., recreation, restaurants and hotels)—industries that have a heavier weighting in UK GDP than other developed economies.[xv] The UK government’s COVID policies have also been relatively harsher and longer-lasting than elsewhere.[xvi] Beyond pandemic-related variables, countries’ GDP tabulation methods vary, from what they include to how they measure. The UK and Italy, for example, try to account for money spent in the more shadowy corners of the informal economy—activities other statistics agencies don’t formally track for GDP.[xvii] How the UK measures public services output—particularly for healthcare and education services—may have caused its lockdown-era GDP decline to look much worse than its peers.[xviii] The ONS found that when excluding public services, economic contractions amongst G7 countries were more comparable, although the UK’s decline was still the largest.[xix] Whilst we think these findings are interesting, they are also largely meaningless to forward-looking shares, in our view.

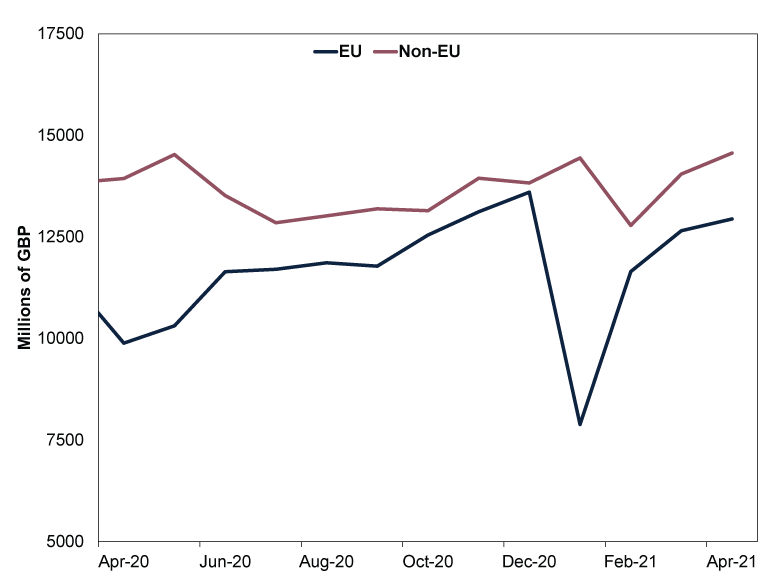

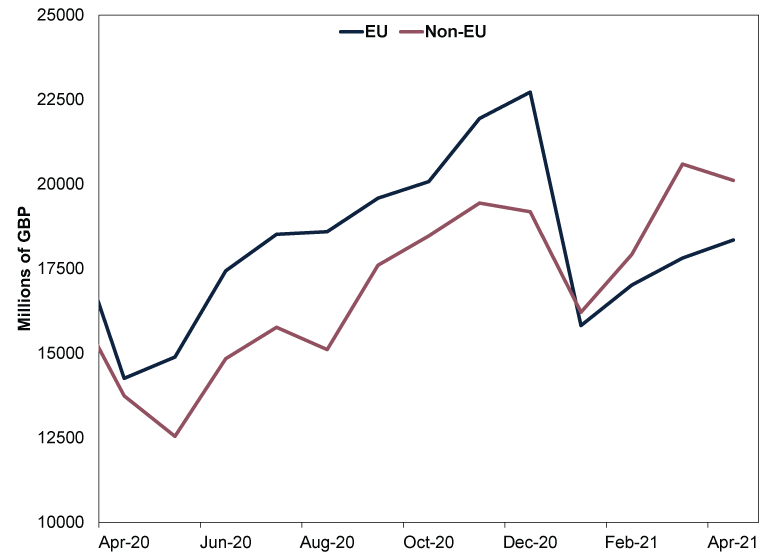

However, we think one OECD concern already appears overstated: Brexit’s hurting UK trade. The latest data show the initial damage was temporary. After dropping in January, EU exports and imports have regained a lot of ground—and non-EU exports and imports have fared even better.[xx] (Exhibits 1 – 2)

Exhibit 1: EU and Non-EU Exports of Goods

Source: ONS, as of 15/6/2021. Exports in goods at current market prices to EU and non-EU nations, monthly, April 2020 – April 2021.

Exhibit 2: EU and Non-EU Imports of Goods

Source: ONS, as of 15/6/2021. Imports in goods at current market prices to EU and non-EU nations, monthly, April 2020 – April 2021.

Though the EU remains the UK’s largest trading partner at a regional level—a status that isn’t likely to change any time soon—the UK isn’t shrinking away from the rest of the global economy.[xxi] Its ties appear to be strengthening given its recent spate of free-trade agreements with non-EU countries.

As economic data continue to roll out, it won’t shock us if financial commentators and experts we follow vigorously debate their meaning. For investors, though, thinking like markets and looking forward seems wise to us. These numbers confirm a reality equities have likely already priced in and moved on from to a large extent, in our view, given our research shows equity markets quickly incorporate all widely known information. We think shares are well aware of the herky-jerky reopening progress. Other countries have had reopening setbacks, and we have seen headlines discuss the possibility of a pushed-back England reopening since April.[xxii] Equities probably also aren’t ignoring the UK and EU’s latest disagreement over their trade deal terms, in our view. If their deal were to fall through, equities probably know businesses on both sides of the Channel already have no-deal Brexit plans that can be deployed if necessary.[xxiii]

In our view, markets are likely looking past the noise and beyond the summer months, to a time when the UK and other major developed economies have returned to a post-pandemic normal (or something close to it). We think it would be beneficial for investors to do the same, despite headlines’ preoccupation with the latest numbers.

[i] Source: ONS, as of 14/6/2021. “GDP Monthly Estimate, UK: April 2021.”

[ii] “UK Growth Upgraded, but OECD Warns of Deepest Economic Scar in G7,” Graeme Wearden, The Guardian, 31 May, 2021.

[iii] See note i.

[iv] Ibid.

[v] Ibid.

[vi] Ibid.

[vii] Ibid.

[viii] Ibid.

[ix] Ibid.

[x] “UK Economy Grows for Third Month in a Row as Covid Controls Ease,” Richard Partington, The Guardian, 11 June 2011.

[xi] “Covid: Lockdown Easing in England to be Delayed by Four Weeks,” Becky Morton and Joseph Lee, BBC, 14 June 2021.

[xii] “UK Economy Lags Behind Other Countries in Covid Recovery,” Staff, BBC, 10 June 2021.

[xiii] See note ii

[xiv] “International Comparisons of GDP During the Coronavirus (COVID-19) Pandemic,” Sumit Dey-Chowdhury, Niamh McAuley and Andrew Walton, ONS, 1 February 2021.

[xv] Ibid.

[xvi] Ibid.

[xvii] “Britain, Italy Include Drugs and Sex in GDP,” Melvin Backman, CNN, 30 May 2014.

[xviii] See note xiv.

[xix] Ibid.

[xx] Source: ONS, as of 14/6/2021. “UK Trade: April 2021.”

[xxi] “UK Trading Partners and Trade Relationships: 2020,” Chris Goldsworthy, ONS, 2 December, 2020.

[xxii] “Step by Step: England's Roadmap for Easing Covid Lockdown,” Peter Walker, The Guardian, 1 April, 2021.

[xxiii] “Deal or No Deal: How Life Will Look for Key Industries After Brexit,” Phillip Inman, Julia Kollewe, Kalyeena Makortoff, Gwyn Topham and Zoe Wood, The Guardian, 12 December 2020.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights SpaceX IPO and Rising Equity Supply2026-06-23

-

Market Analysis Reviewing America’s Q1 Earnings and What Q2 Expectations Say2026-06-23

-

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-23

-

Market Analysis A Market Perspective on Iran Truce Talks2026-06-17

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today