Personal Wealth Management / Economics

A Quick Lesson Hidden in the Eurozone’s Double Dip

Why contracting GDP and expansionary business surveys aren’t in conflict, in our view.

After weeks of speculation amongst financial commentators we follow, it is official: The eurozone has double-dipped. Or, more formally, the eurozone’s gross domestic product (GDP, a government-produced metric of economic output) contracted in Q1. This is the second straight decline, signifying a broad decline in economic output is underway—what many economists call a recession. And, given there was another recession tied to lockdowns in early 2020, this second drop makes the return to contraction a double-dip recession. Whilst this was widely expected by financial commentators and economists we follow, the interesting thing about this one, in our view, is that it seems to defy widely watched business surveys that reported growth throughout Q1, which we will detail shortly. However, seemingly contradictory datasets don’t seem strange to us after diving into the dataset’s details—a big reason why we think digging into the data can be worthwhile for investors.

Of the eurozone’s four largest economies, only France (0.4% q/q) grew in Q1.[i] Italy (-0.4% q/q), Spain (-0.5% q/q) and Germany (-1.7% q/q) contracted, contributing to the eurozone’s -0.6% q/q decline.[ii] The results didn’t surprise the experts quoted in financial publications we follow. Many noted that ongoing lockdowns reduced eurozone output in the quarter, and we concur. See Germany, where COVID restrictions persisted in Q1 and may linger until the end of May or mid-June, based on government officials’ latest rumblings. That is a stark contrast with America, where states began easing restrictions in early March.

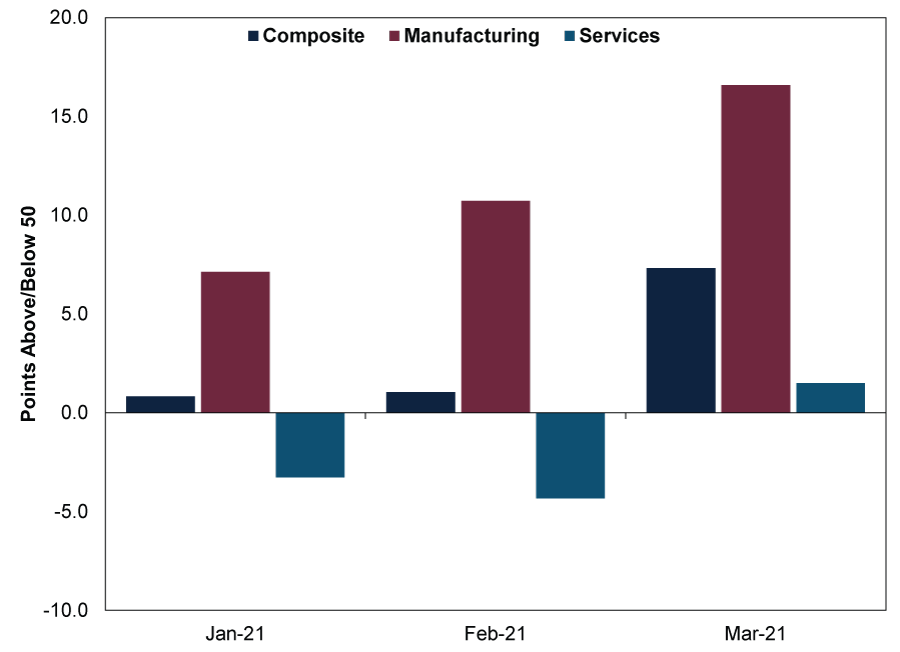

Those who monitor economic data closely may notice a seeming contradiction in this contraction: Why was GDP so weak even as business surveys reported growth? Take Germany, whose IHS Markit Composite Purchasing Managers’ index (PMI) registered 50.8, 51.0, and 57.3 in January, February and March, respectively.[iii] A Composite PMI combines output from both the services and manufacturing sectors, and readings above 50 imply expansion, according to the survey’s methodology. Yet German GDP’s quarterly decline was the sharpest amongst major eurozone economies.

We don’t think these data are in conflict—they just measure different things. PMIs are business surveys reflecting private sector activity. They are a timely snapshot of general business conditions—i.e., whether respondents see more economic activity or less in a given month—but they don’t measure the magnitude of that activity. GDP, in contrast, tallies broad economic activity. It tracks inputs including personal consumption, private investment, government spending and trade—and the magnitude by which those components grew or contracted in a given time period. GDP is a comprehensive attempt to track how a nation or region’s broad economy is faring, though we think it has imperfections. For example, GDP treats government spending as always and everywhere growth-positive—not necessarily the case, in our view, as public spending and investment can crowd out private activity, which may not be a net positive.

In the case of Germany’s Q1 numbers, the composite PMI reflected record-setting manufacturing activity that overshadowed a subdued services sector.

Exhibit 1: Q1 German PMIs

Source: FactSet, as of 4/5/2021. Readings above 50 imply expansion.

As IHS Markit Associate Economics Director Phil Smith noted:

The German Manufacturing PMI marked its 25th anniversary in March with a record-high reading of 66.6, showing the goods-producing sector going from strength to strength. It was a record-breaking month on many fronts including new export orders, which have benefited from synchronised upturns in sales to the US and China and seen an unprecedented number of German manufacturers reporting growth.[iv]

However, Germany’s Services PMI returned to expansion only in March—and barely, as lockdown measures hindered businesses, which we think is relevant to Q1 GDP’s weak showing. According to our financial coverage, many observers view Germany as an industrial powerhouse, with the seeming implication that factory output is the dominant driver behind GDP growth. However, manufacturing’s share of German GDP is roughly 20%.[v] Services comprise 70%—much more influential on GDP’s direction.[vi] COVID restrictions disproportionately impact services businesses, many of which are people-facing. In contrast, outside of last year’s initial lockdowns , German factories remained operational when subsequent COVID waves triggered new restrictions. Alongside other temporary developments—e.g., weak household consumption may have also reflected the expiration of a temporary value-added tax (VAT) cut that prompted consumers to make purchases before the tax rate rose in Q1—Germany’s GDP contraction isn’t a shock to us.

Whilst GDP and PMIs receive plenty of attention when released, we think markets see through all the associated chatter and analysis, as they have already digested the information. GDP covered January, February and March. We are now in May. Even preliminary, or flash, PMIs, which preview the final figures, reflect responses from several weeks prior. These data therefore confirm a reality we think shares have already priced in. Our research shows equities are forward-looking, which means they focus on the future—specifically the next 3 – 30 months, in our view. We think what matters most from here is how investors’ expectations align with reality. With vaccines finally rolling out across the Continent, we think the eurozone economic recovery is likely to soon follow the general path of other major economies, including China, America and the UK. That likely means a brief growth-rate pop before a return to pre-COVID growth trends, in our view. To us, this is worth keeping in mind now, especially as financial commentators become more optimistic about growth ahead.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-14

-

Politics Can Germany Engineer Faster Growth at Last?2026-07-08

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-02

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today