Personal Wealth Management / Market Analysis

America’s Q2 Earnings in Focus

We think they mostly just confirm what sector returns already reflect.

America’s Q2 earnings season is winding down, with the vast majority of S&P 500 companies having reported.[i] Given the US is 70% of developed world stock market capitalisation, we think its profit picture is worth reviewing for global investors.[ii] The results? Three-fourths of those reporting so far beat expectations, and revenues did much of the heavy lifting.[iii] Yet whilst Energy earnings soared, profits in the other 10 sectors combined fell, echoing the split amongst sector returns during this year’s stock market downturn.[iv] In our view, this is a good reminder that stocks look forward.

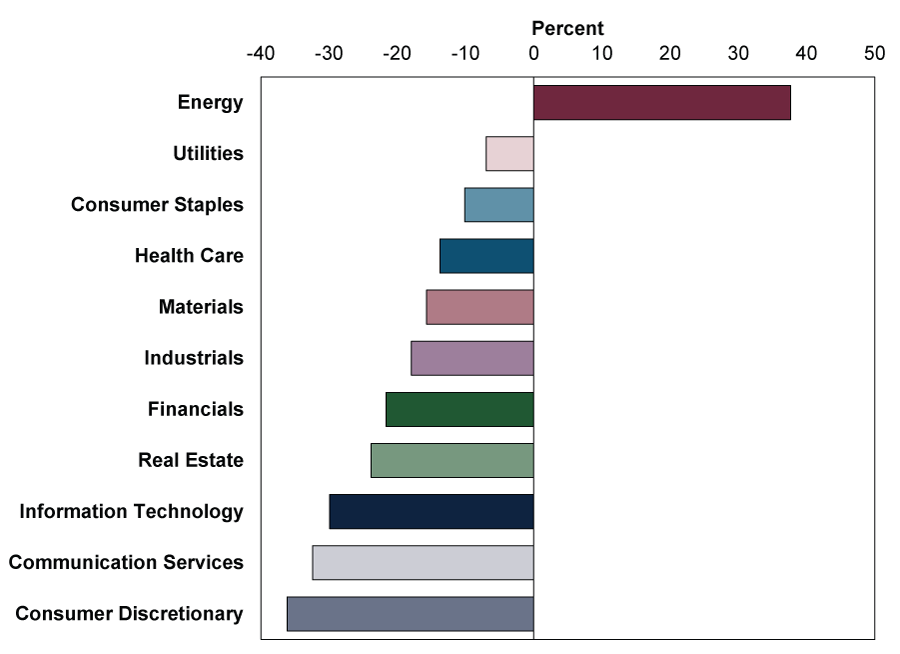

In US dollars, US and global stocks’ declines this year breached -20%, which is the traditional threshold for a bear market—an extended deep stock market decline, typically with a fundamental cause.[v] As Exhibit 1 shows, S&P 500 sector returns in US dollars from their early peak this year through the year’s low point to date on 16 June mostly seemed to preview how earnings turned out. Whilst S&P 500 earnings overall rose 6.7% y/y, much of that came from Energy earnings soaring 299.2%.[vi] Excluding Energy, they fell -3.7%.[vii] So whilst headline earnings growth was near its 7.1% annualised average historically, we think it masks some underlying weakness.[viii] Yet first-half sector returns appear to us to have largely captured the earnings dynamic below the surface, with only Energy positive through Q2.[ix] Markets anticipated high oil prices’ impact on Energy earnings well in advance of official reports, in our view.

Exhibit 1: S&P 500 Sector Returns, 3/1/2022 – 16/6/2022

Source: FactSet, as of 16/8/2022. S&P 500 sector total returns in US dollars, 3/1/2022 – 16/6/2022. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns.

Note that we aren’t arguing stocks fell this year on earnings weakness outside Energy—in our view, sentiment, not fundamental problems, was the downturn’s primary contributing factor. Moreover, whilst investors’ anticipation of high oil prices driving big earnings growth probably drove Energy’s singular outperformance, in our view, it isn’t as if non-Energy sectors’ earnings fell and surprised negatively across the board. Excluding Energy, five sectors’ earnings rose (Industrials, Materials, Real Estate, Health Care, Tech), and five fell (Financials, Consumer Discretionary, Communication Services, Utilities and Consumer Staples).[x] Of the former, Industrials, Health Care and Tech earnings are coming out ahead of consensus expectations at Q2’s end.[xi] Meanwhile, Financials, Consumer Discretionary and Communication Services earnings have been materially worse than expectations indicated.[xii]

But there are some nuances here as well. For example, Financials companies’ setting aside loan loss provisions due to a new US accounting rule appears to be driving the sector’s earnings negativity.[xiii] However, this is mainly precautionary, in our view—whether actual loan losses result is questionable—and releases of these reserves as America’s economic and financial conditions improve could boost earnings later (this, too, is a facet of the accounting rule). To see how distortionary this may be, S&P 500 earnings excluding Financials would be 14.2% y/y, more than doubling the headline growth rate.[xiv] As for Consumer Discretionary and Communication Services, we don’t think it is a secret categories that saw huge growth during the pandemic (e.g., Internet & Direct Marketing Retail) are giving some of it back as travel and in-person services industries (like Hotels, Restaurants and Leisure and Automobiles) resume normal operations. In Communication Services, we find Interactive Media & Services drove its earnings decline as businesses’ online advertising failed to match last year’s strong post-COVID boom.

With Q2 earnings more mixed under the bonnet, in our view, the narrative that only Energy is seeing profits at the expense of all else breaks down. We think it is also notable that every sector’s revenues rose in Q2, which cuts against widespread inflation (economy-wide price increases) and energy price-fuelled recession warnings.[xv] S&P 500 revenue growth was 13.6% y/y, and even excluding Energy, sales rose 8.8%.[xvi] Corporate America has varying degrees of pricing power, but we think this demonstrates its overall resilience—and why our research finds stocks typically keep up with, or outpace, inflation over time (notwithstanding this year’s bear market, of course).

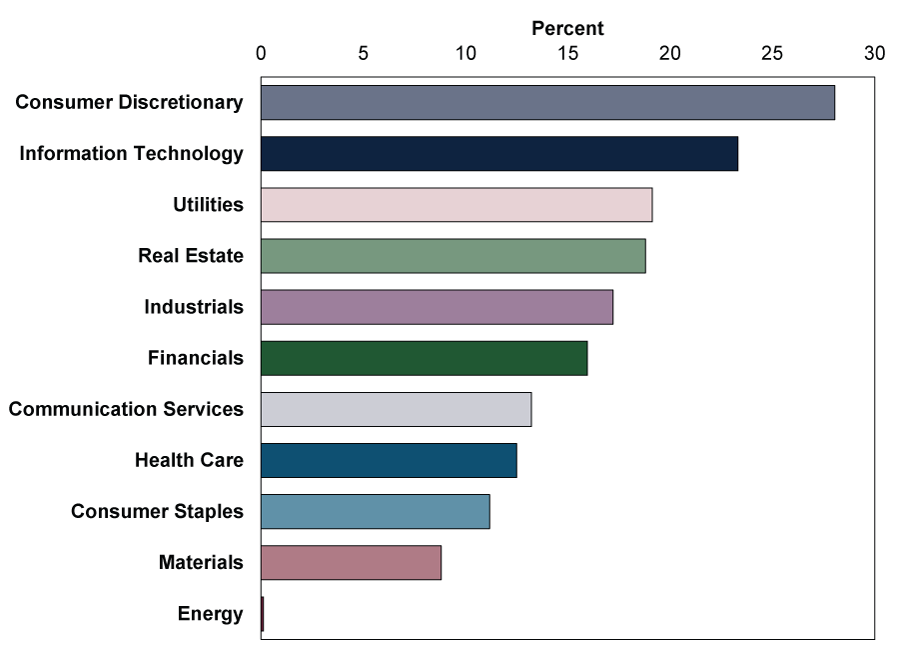

Overall, we think stocks seem to be looking beyond Q2’s pockets of earnings weakness. Whilst our research shows markets swing on sentiment in the short term, over the longer term we think they look forward 3 to 30 months and assess how likely earnings outcomes compare with present sentiment. Since 16 June, the market’s assessment of future reality has seemingly shifted markedly, in our view—if not turned a corner. Exhibit 2 shows Energy up only 0.1% since stocks’ year-to-date low point, as crude oil’s price has fallen -29.8% from its 8 March peak.[xvii] It seems likely to us that markets are suggesting it may be harder for Energy to beat expectations. Conversely, though, we think the bigger gains for every other sector since then suggest the expectations bar was low for them, particularly the ones hit most in the first half. In our view, judging by ongoing earnings scepticism amidst widespread recession chatter, a big gap between expectations and reality still exists.

Exhibit 2: S&P 500 Sector Returns, 16/6/2022 – 15/8/2022

Source: FactSet, as of 16/8/2022. S&P 500 sector total returns in US dollars, 16/6/2022 – 15/8/2022. Currency fluctuations between the US dollar and pound may result in higher or lower investment returns.

We don’t know whether stocks’ rally from mid-June will mark a sustained recovery. That will only be clear in hindsight, but it appears to us the conditions are in place. We find sentiment remains dour, yet we see much to suggest sentiment has overshot reality to the downside. From here, we think that is what matters for stocks’ direction going forward: How will Q3 earnings—and beyond—fare against expectations? In our view, that is what investors should be focussing on, too.

[i] “FactSet Earnings Insight,” John Butters, FactSet, 5/8/2022.

[ii] Source: FactSet, as of 16/8/2022. Statement based on MSCI World Index market capitalisation by country, 15/8/2022.

[iii] See note i.

[iv] Ibid.

[v] Source: FactSet, as of 16/8/2022. Statement based on S&P 500 total returns and MSCI World Index returns with net dividends in USD. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[vi] See note i.

[vii] Ibid.

[viii] Source: FactSet, as of 16/8/2022. S&P 500 earnings, Q1 1990 – Q2 2022. The annualised growth rate refers to the compound annual growth rate that would deliver the cumulative growth rate over time.

[ix] Source: FactSet, as of 16/8/2022. Statement based on S&P 500 sector returns, 31/12/2021 – 30/6/2022.

[x] See note i.

[xi] Ibid.

[xii] Ibid.

[xiii] “Wall Street Debates the Real Message Behind Bank Loss Provisions,” Enrique Roces and Natalia Kniazhevich, Bloomberg, 20/7/2022. Accessed via Advisor Perspectives.

[xiv] See note i.

[xv] Ibid.

[xvi] Ibid.

[xvii] Source: FactSet, as of 16/8/2022. Brent crude oil spot price, 8/3/2022 – 15/8/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

-

Market Analysis February’s Growthy Data—and the Iran War’s Souring Sentiment2026-03-06

-

Market Analysis Putting the Latest Private Credit Implosion in Perspective2026-03-06

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today