Personal Wealth Management / Market Analysis

Europe Has a Parliament—and Gridlock

Despite all the noise, we think this weekend’s results likely entrench gridlock in the European Parliament—and in national parliaments as well.

Editors’ Note: Our political commentary is nonpartisan by design. We favour no party, politician or elected official in any country and assess political developments solely for their potential economic or financial market impact.

The dust has settled after late-May’s European Parliamentary elections, and the winners are becoming clear: everyone and no one! Ok, perhaps that is a bit oversimplified. But pro-European parties combined for more than 50% of available seats—seemingly a victory of sorts.[i] Then again, the two biggest centrist groupings lost their combined majority for the first time since the European Parliament launched in 1979. Populist and eurosceptic parties combined for a largest-ever total of 25% of seats. But those populists aren’t unified, and no faction won anywhere near enough seats to get a meaningful place at the table. Meanwhile, both pro- and anti-Brexit parties in the UK are claiming victory, whilst one of Italy’s ruling populist parties appears to be claiming a newfound mandate. For investors, we think the outcome is much simpler: entrenched gridlock, which should provide relief to European shares, in our view.

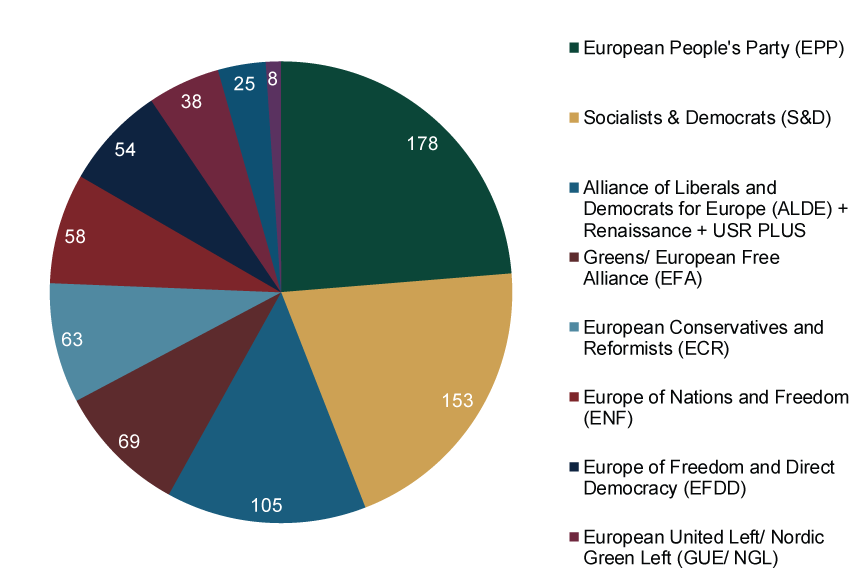

Exhibit 1 shows the latest tally. The two traditional groups—the centre-right European People’s Party (EPP) and centre-left Progressive Alliance of Socialists and Democrats (S&D)—took first and second place, respectively, but combined for only 44.1% of seats.[ii] However, a third centrist group, the Alliance of Liberals and Democrats for Europe (ALDE) and its allies, took third place with 14% of seats, giving a three-way centrist coalition an easy majority if that is the road party leaders decide to take. Throughout the coverage we read, political analysts worldwide seem to think this is the likeliest outcome, perhaps with the Green Party joining. We suppose a left-leaning coalition of S&D, ALDE, Greens, leftists and the populist Europe of Freedom and Direct Democracy (EFDD) is also possible, as is some other fractured hodgepodge. But whatever coalition ultimately emerges, simple maths suggest it will have at least three main parties—a recipe for internal disagreements and next to nothing happening, in our view. We suspect populist parties will probably spend most of their time making rousing speeches from the back benches, not writing radical legislation.

Exhibit 1: European Parliamentary Election Results (Number of Seats)

Source: European Parliament, as of 28/5/2019. https://www.election-results.eu/

This apparently hasn’t stopped individual populist leaders from claiming victory. In Italy, The League took 34.3% of the vote, more than doubling its national coalition partner, Five Star Movement (M5S).[iii] To say these parties didn’t get along before last week’s vote seems like an understatement to us—despite being “populists,” they agree on little, with Matteo Salvini’s League skewing far-right and M5S leaning quite to the left. Salvini and M5S leader Luigi DiMaio are also rival deputy prime ministers, frequently battling for influence and the spotlight. As Salvini worked the press after the results hit, he argued he now has a mandate from Italian voters to ram through policies like a two-tier flat tax and greater autonomy for the northern regions—policies M5S is less keen on. That raises speculation over a potential snap election, but for now Salvini says he wants to keep the current administration in place. This could be because the centre-left Democratic Party (PD) surprised most observers by taking second place with 22.7% of the vote. It and M5S combined for 39.8% of the vote, not far behind The League and centre-right Forza Italia’s total, 43.1%. Considering European Parliamentary elections have historically tended to have lower turnout than national contests and serve as more of a protest vote, Salvini may not want to risk overplaying his hand and ending up out of government if PD beats expectations again.

As for the UK, if we had to use one word to describe the results, it would be “messy.” The Brexit Party, whose platform is probably self-evident, took first place with 31.7% of the vote.[iv] The Liberal Democrats, which seem to be one step away from renaming themselves The Remain Party, came in second at 18.5%. Labour came next, with 14.1%, followed by the Greens with 11.1% and the Conservatives with just 8.7%. Brexiteers are of course calling it a victory. Yet so are Remainers, arguing the Lib Dems, Greens and Welsh and Scottish Nationalists combined for an anti-Brexit win. Some Labour MPs are now arguing their party should endorse the so-called “People’s Vote,” aka a second Brexit referendum. However, we think the fact the Brexit Party nearly swept Wales—a traditional Labour stronghold—and England likely makes other Labour leaders queasy about going full-fledged Remain. Meanwhile, despite both sides’ shouting about renewed momentum, turnout was only 36.9%. Yes, that is the second-highest since 1979, but also, it is only 36.9%.[v] Turnout in 2017’s general election was nearly double that, 68.8%.[vi] We find it difficult to draw sweeping conclusions from what looks like a clear protest vote. However, it also seems realistic to expect pro-Brexit candidates for Conservative Party leadership to gain an edge, as well as for sitting MPs to do whatever it takes to avoid a snap election, just in case. Other than that, though, the status quo of gridlock and Brexit uncertainty (or if you prefer, chaos) probably persists.

On the whole, though, we think this weekend’s results look positive for Continental European shares. Pre-vote uncertainty is gone. Populists didn’t make the sweeping gains we saw some financial pundits warning they could. Pro-EU forces likely still hold sway and, almost certainly, the power. In our view, this sets the stage for relief in the coming months as the victors gel, a coalition emerges and the reality of gridlock sets in. For markets, we think the combination of reduced uncertainty and low legislative risk should be a nice tonic.

[i] Source: European Parliament and Kantar, as of 28/5/2019 at 10:48 PM BST. https://www.election-results.eu/european-results/2019-2024/

[ii] Ibid.

[iii] Ibid. https://www.election-results.eu/national-results/italy/2019-2024/

[iv] Ibid. https://www.election-results.eu/national-results/united-kingdom/2019-2024/

[v] Ibid.

[vi] Source: House of Commons Library, as of 28/5/2019. https://researchbriefings.parliament.uk/ResearchBriefing/Summary/CBP-8060%23fullreport

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today