Personal Wealth Management / Financial Planning

Four Timely Timeless Lessons for a Volatile Market Environment

Reviewing some well-known keys to successful long-term investing.

Global stocks are down slightly year to date, and the path has been quite volatile.[i] Stocks slumped from early January – early March before rebounding sharply by the end of Q1.[ii] From there global stocks churned lower—down as much as -13.9% after hitting their year-to-date low on 16 June—before rallying over the next two months.[iii] Then from mid-August through Wednesday, the MSCI World Index fell -3.8%.[iv] In our experience, sharp bouts of volatility can cause investors to focus on short-term developments, which can drive reactive investment decision-making—a mistake, in our view. To counter that thinking, here are several timeless lessons we think are particularly useful during a challenging year for investors.

Lesson One: Fathom the Power of Compounding

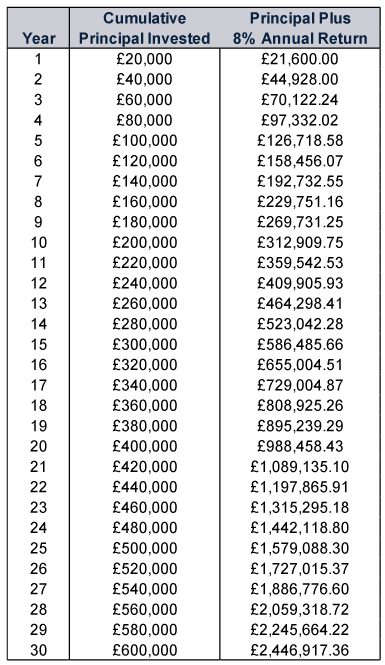

Many financial publications we follow discuss the concept of compound growth—i.e., earning a return on returns. In our view, understanding this concept is critical for investors, as those who take advantage of compounding’s power position themselves well for the long-term. To illustrate compounding in practice, consider the following hypothetical: A UK investor contributes £20,000 to an Investment ISA and earns a return of 8% after one year (£1600). For illustrative purposes only, presume this investor invests £20,000 at the beginning of each year for the next 29 years, makes no withdrawals and earns a constant 8% annual rate of return. Thanks to compounding, that cumulative contribution of £600,000 over 30 years turns into over £2.4 million. (Exhibit 1)

Exhibit 1: A Hypothetical Illustration of Compounding’s Power

Source: Math and Microsoft Excel. Note, actual investment returns are highly unlikely to be this consistent and smooth. We share this table strictly for illustrative purposes.

Realistically, investment returns aren’t this smooth. However, we think history provides a useful guide, and global stocks have an annualised return of 10.3% since 1970.[v] That figure includes both positive and negative periods for stocks—as well as many bouts of volatility. To capture that growth, we think investors benefit from thinking long term.

Lesson Two: Long-Term Returns Include Extended Negative Stretches

The S&P 500, a US stock index we cite here for its long historical dataset, has an average annualised return of 10.3% since 1925.[vi] That figure includes nearly a century’s worth of market results, including negativity from bear markets (typically prolonged and fundamentally driven declines exceeding -20%) and corrections (short, sharp, sentiment-driven declines of -10% to -20%) to pullbacks and daily dips. This year isn’t an anomaly in that regard, in our view.[vii] Now, no individual investor likely invests with the next 100 years in mind. Rather, with the Office for National Statistics estimating UK life expectancy at around 22 years for 60-year-old males and 25 years for 60-year-old females today—we have found that people nearing retirement tend to focus on much shorter periods, and many commentators we follow warn one or two big negative years can permanently set back a retirement portfolio.[viii]

But consider 20-year periods. Since 1926, the S&P 500 has averaged about 5 negative years per rolling 20-year stretch.[ix] Yet no rolling 20-year period has been negative, and the worst run (1929 – 1949) included the market crash of 1929, the ensuing Great Depression and World War II.[x] Despite 10 negative years, that stretch’s average total return (price return plus reinvested dividends) was 6.2%.[xi]

The past isn’t predictive of the future, in our view, and it is always possible stocks deliver weaker—or even negative—returns over the next 20 years. But making portfolio decisions based on historically unprecedented, possible outcomes isn’t wise, in our view.

Lesson Three: Most Investing Harm Is Self-Inflicted

In our experience, one of the most counterproductive moves investors can make is changing their asset allocation (a portfolio’s mix of stocks, fixed interest, cash and other securities) in reaction to negative volatility. If you are able to identify a bear market early enough, we think it can make sense to shift. But taking action for the sake of doing something—the comforting feeling of taking control in an uncomfortable situation—is often counterproductive, in our view. Selling when stocks are down turns paper losses into actual losses and leads to what we think can be an even bigger risk: not returning to markets for the subsequent recovery. In our view, not participating in bull markets (extended periods of rising equity prices) is a significant risk to investors’ ability to reach their long-term goals.

American columnist Michelle Singletary of The Washington Post recently highlighted the costs associated with missing a stock market recovery.[xii] She described three hypothetical investors in September 2008 and the actions they took (or didn’t take) with their 401(k) plans (a company-sponsored retirement account in America, which employees can contribute income to) after US stocks had fallen by -20%:

The first investor jumped out of the market, going to all cash, and stopped making contributions. The second one also moved to cash but kept contributing to a workplace plan. The third investor kept the money invested and continued to contribute. The latter two investors each had $15,000 going into their 401(k) annually, including employer matching contributions.

By February 2012, the investor who cashed out and stopped contributing had $353,400. The worker who went to cash at least returned to making 401(k) contributions and had $404,709. The third investor had $524,600 by sticking to the original investment mix.

Often in investing, doing nothing is the most beneficial long-term move, in our view.

Lesson Four: Long-Term Investing Isn’t Easy

That said, long-term investing isn’t an easy, stress-free endeavour. Whether you have been investing for decades or just started to learn about the stock market, we don’t think anybody is perfectly immune from the market’s challenges. Whatever their experience level, people are at risk of making mistakes by acting on emotional impulses, in our view. Moreover, there is no silver bullet strategy, and if anyone tells you otherwise, we think it is wise to treat that idea sceptically.

But whilst times can be trying today, flat or negative market periods needn’t prevent you from reaching your investing goals, in our view. Thinking longer term and focusing on what you want your money to provide for you in the future can help instill discipline when negative market volatility challenges nerves.

Finally, mistakes come with the territory, and we have found most investors make them. Rather than beat yourself up, view them as learning opportunities that will make you a better investor going forward. During rough market periods, perspective and levelheadedness are your best allies, in our view.

[i] Source: FactSet, as of 14/9/2022. MSCI World Index returns with net dividends, in GBP, 31/12/2021 – 13/9/2022.

[ii] Ibid. MSCI World Index returns with net dividends, in GBP, 3/1/2022 – 31/3/2022.

[iii] Ibid. MSCI World Index returns with net dividends, in GBP, 31/3/2022 – 19/8/2022.

[iv] Ibid. MSCI World Index returns with net dividends, in GBP, 19/8/2022 – 13/9/2022.

[v] Source: FactSet, as of 7/9/2022. MSCI World Index returns with net dividends, in GBP, 1970 – 2021. An annualised return is the compound annual growth rate that would deliver the cumulative return over a given period.

[vi] Source: Global Financial Data, as of 28/3/2022. S&P 500 Total Return Index, 31/12/1925 – 31/12/2021. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[vii] Ibid.

[viii] “Expectation of Life, Principal Projection, UK,” Office for National Statistics, 12/1/2022.

[ix] Ibid.

[x] Ibid.

[xi] Ibid. S&P 500 Total Return Index, 31/12/1925 – 31/12/2021. Statement based on average annual return from 1929 – 1949. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[xii] “When the Stock Market Is Crazy, Invest Like a Millionaire,” Michelle Singletary, The Washington Post, 19/8/2022. Accessed via the Richmond Times-Dispatch.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today