Personal Wealth Management / Politics

Germany Gets Political Gridlock Again

Whatever coalition emerges following the weekend’s election probably can’t pass much.

Editors’ Note: MarketMinder Europe is politically agnostic. We prefer no politician nor any party and assess political developments for their potential economic and market impact only.

The results are in, and German voters have elected—wait for it—political gridlock. No party took a majority in Sunday’s federal election, and it is far from clear which party will head the next government and who will replace Angela Merkel as chancellor—as we (and most observers we follow) expected. Coalition negotiations could very well take months. Yet for markets, we think this all amounts to political stability and the extension of the status quo, which we think has long been a fine backdrop for German equities.[i]

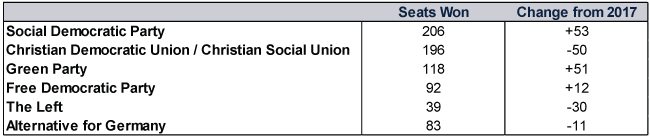

Heading into the vote, the centre-left Social Democratic Party (SPD) was polling just ahead of Merkel’s centre-right Christian Democratic Union (CDU) and its Bavarian sister party, the Christian Social Union (CSU).[ii] Those polls proved more or less right, with the SPD winning 25.7% of the vote and the CDU and CSU combining for 24.1%.[iii] The SPD took a small plurality of the Bundestag’s 735 seats.

Exhibit 1: German Election Results

Source: German Federal Returning Officer, as of 27/9/2021. The South Schleswig Voters’ Association took one seat.

All parties fell well short of the 368 needed to form a majority, ensuring Germany will get another coalition government—the postwar norm. As it stands, few commentators we follow expect the SPD and CDU/CSU to renew their eight-year-old coalition, as both parties have stated their preference for something new. Voters, who upped their support for the Greens and pro-business Free Democratic Party (FDP), seem to agree. Mathematically, any new coalition would require one of the main parties to join with both the FDP and Greens, making them joint kingmakers. But they are also odd bedfellows, as they have little common ground ideologically—the FDP is right-leaning and founded on free-market principles, whilst the Greens lean left and see a large role for the state in directing resources. When Merkel tried to form a coalition with both parties after 2017’s election, talks collapsed after several fruitless months.

In most European parliamentary democracies, the head of state (be it the monarch or president) assesses the results and then asks the leader of the top-finishing party to form a government. If that party doesn’t have a majority, the leader then sets out negotiating with potential coalition partners. In Germany, however, it is a free for all. The president doesn’t tap anyone, and all parties are free to pursue their own coalitions simultaneously. As a result, SPD leader Olaf Scholz and CDU leader Armin Laschet each stated they would attempt to build a coalition with the FDP and Greens Monday. Both leaders’ personalities thus came into focus throughout the commentary we read. Scholz, who has a reputation for calm leadership after serving as Merkel’s finance minister, acted the part of chancellor in waiting. Laschet, meanwhile, ignored calls from within his party to concede and resign following the CDU’s worst drubbing since WWII, illustrating the divisions that have reportedly plagued his leadership from the start.

But counting the CDU out would be wrong, in our view. For one, neither the SPD nor the CDU/CSU initially wanted to renew their coalition after 2017’s election—but that is exactly what they ended up doing.[iv] Two, FDP leader Christian Lindner has said his party prefers to be part of a centre-right coalition.[v] To us, it seems likely he and other FDP bigwigs remember the thrashing they took in 2013’s election as supporters punished their participation in the Greek, Portuguese and Irish bailouts, which many observers we followed at the time argued went against the party’s traditional free-market values and fiscal conservatism. If supporting a centre-right government landed them in such hot water with voters then, rubber-stamping policies further to the left may not strike FDP leaders as a wise endeavour now. But coalition building often isn’t about ideological purity—it usually is about power and influence. Leaders might see major cabinet posts as enough of a win.

If recent history is a guide, negotiations will likely stretch on for several weeks or even months, delaying Merkel’s retirement (she remains caretaker chancellor). Scholz and Laschet have talked of having a new government by Christmas, which seems a tad optimistic to us. There isn’t much indication either party will be involved in serious talks anytime soon. We have seen reports the FDP and Greens are just beginning talks to see what—if any—common ground they have and stake out a potential joint negotiating position. But even getting that far will require either party to concede on whether to reach out to the SPD (the Greens’ preference) or CDU/CSU (the FDP’s) first. Oh, and we think they will likely also need to find some overlap on taxes, infrastructure spending and the country’s constitutional deficit limit, which the FDP wants to reinstate from its temporary pandemic hiatus and the Greens want to repeal. All of these issues seem to us like potential deal breakers.

We suggest not getting consumed by all of the political theatrics that will likely ensue, which will likely dive deep into what this-or-that coalition pairing could emphasise and potentially explore the leanings and interests of various potential ministers. For equity markets, we think that stuff is a sideshow. Our research shows policies, not personalities, determine politics’ market impact. A slow-moving coalition process that yields a fractured government is a recipe for legislative inaction. In either of the possible three-party coalitions, divides between the FDP and Greens appear likely to torpedo any major legislation. If both three-party possibilities fall through and the SPD and CDU/CSU join forces again, we have already seen what that looks like. In all cases, major changes seem unlikely. We might see taxation and spending tweaks at the margins, but there presently aren’t enough votes to repeal the debt brake—not with the CDU/CSU and FDP opposed to doing so. Scholz, too, has stated he would prefer to reform rather than repeal the limit.[vi]

For equities, we think this extended gridlock is a fine backdrop—as it has been for years in Germany. According to our research, equity markets are generally happiest when governments can’t alter property rights or otherwise discourage risk-taking and investment. Gridlock thus lowers legislative risk aversion, giving equities a few less potential negatives to stew over. Protracted stalemates aren’t bearish, either. Dutch voters went to the polls in mid-March, and the Netherlands still doesn’t have a government—yet the country has outperformed European shares cumulatively since the election.[vii] Similarly, German shares beat European shares during the nearly six-month stalemate after 2017’s election.[viii] We think markets simply saw what voters perhaps couldn’t: A government that can’t form for months on end can’t rock the boat much.

[i] Source: FactSet, as of 27/9/2021. Statement based on MSCI Germany Index return with net dividends.

[ii] “German Election Too Close to Call as Polls Find SPD Has Lots Its Lead,” Kate Connolly, The Guardian, 24/9/2021.

[iii] Source: German Federal Returning Officer, as of 27/9/2021.

[iv] “Germany’s Coalition Agreement: What’s In It?” Ben Knight and Timothy Jones, Deutsche Welle, 12/3/2018.

[v] “German Coalition Talks Could Take Months After Split Vote: Guide,” Patrick Donahue and Benedikt Kammel, Bloomberg, 26/9/2021. Accessed via MSN.

[vi] “Christian Lindner: Return of the German Kingmaker,” Hans von der Burchard, Politico, 24/9/2021.

[vii] Source: FactSet, as of 27/9/2021. Statement based on MSCI Netherlands and MSCI Europe returns with net dividends, 15/3/2021 – 24/9/2021.

[viii] Ibid. Statement based on MSCI Germany and MSCI Europe returns with net dividends, 22/9/2017 – 7/2/2028.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today