Personal Wealth Management / Economics

Into Perspective: UK Q4 GDP

We find the end of COVID restrictions is pumping up economic expectations.

Q4 UK gross domestic product (GDP, a government-produced measure of economic output) rose 1.0% q/q, leaving it just -0.4% below its Q4 2019 high, spurring rising enthusiasm amongst commentators we follow for a post-Omicron bounce.[i] Even monthly GDP’s tiny December contraction didn’t appear to dent their economic outlook. Yet we think a more measured view is in order. Whilst UK output is likely to grow, in our view, forward-looking stocks probably already reflect restrictions’ end, and a swift advance seems unlikely.

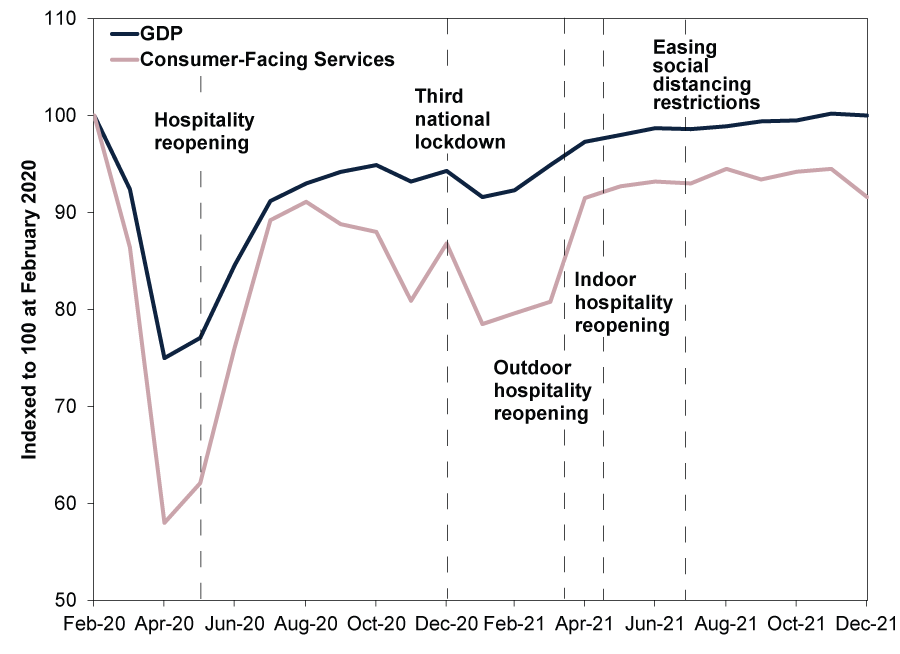

As Exhibit 1 shows, UK monthly GDP’s -0.2% m/m dip came mostly from consumer-facing services, which fell -3.0%.[ii] Based on our reading of the data, services’ slide stemmed largely from Omicron restrictions that are now gone and, judging from how the political winds are blowing, seem highly unlikely to return—hence the broad enthusiasm for a post-restriction rebound amongst commentators we follow. Perhaps adding to the cheer, overall output merely inched down from November’s new monthly high to February 2020’s pre-pandemic level.[iii]

Exhibit 1: Monthly UK GDP Back to Level Despite Consumer-Facing Services’ Lag

Source: ONS, as of 11/2/2022. Monthly UK GDP and consumer-facing services, February 2020 – December 2021. Consumer-facing services consists of retail trade, food and beverage serving activities, travel and transport, and entertainment and recreation.

We do agree there is more room for improvement, as the services sector has lagged heavy industry. The biggest contributor to December GDP was human health and social work activities, which the Office for National Statistics (ONS) said was driven by the NHS’s Test and Trace and vaccination programmes.[iv] But only 5 of 14 services sub-sectors are above their pre-pandemic levels, which suggests to us some catch-up growth likely remains ahead.[v]

That likely happens in Q1, now that restrictions are gone, in our view. Yet economists’ consensus forecasts seem a touch optimistic to us. The median forecast is for GDP to grow 0.7% q/q in Q1 and 0.8% in Q2.[vi] Consensus forecasts envisage growth remaining elevated through yearend at 0.7% and 0.6% for Q3 and Q4, respectively.[vii] This would be above the last expansion’s 0.5% q/q average.[viii] We aren’t in the business of giving precise GDP forecasts, but we think projecting above-average growth indefinitely is probably a stretch. Whilst there is some catch-up room left, in our view, there doesn’t appear to be that much of it, the overall base is higher, and fundamentals largely point to a return of lacklustre pre-pandemic growth rates. Plus, given services’ December decline wasn’t huge, we don’t think a big immediate bounce is likely in the offing, either. Then too, the latest restrictions didn’t force business closures, so we don’t think their end is likely to cause a big surge in economic activity from pent-up demand. Also, it is unclear to us how much of retail trade’s decline was due to discounts and supply chain chatter pulling holiday demand into November, versus Omicron’s deterring people from the high street.

We think recent history also argues against swift growth. After a big 5.6% q/q reopening bounce in Q2 2020, Q3’s growth slowed to 1.0%.[ix] A similar slowdown followed the post-reopening boomlet after winter and spring 2021’s milder lockdown, as Exhibit 1 demonstrated. Once pent-up demand was spent, growth rates reverted to the slower pre-pandemic trend.[x] We don’t think this spring and summer are likely to deviate much from that script. In our view, if economists are pencilling in fast UK growth and expecting the country to keep outperforming for the whole year, those expectations are likely reflected in stock prices by now, setting markets up to do something different.

The services-heavy UK economy suffered the most amongst developed countries amidst lockdowns, due in large part to the way the ONS calculates GDP.[xi] It has now bounced back.[xii] But we don’t think it helps to extrapolate much beyond that. The easy recovery phase is now mostly in the rear view and doesn’t say anything about the UK’s longer-term outlook, which is what stocks are focussing on, in our view.

[i] Source: ONS, as of 11/2/2022. UK GDP, Q4 2021.

[ii] Ibid. Monthly UK GDP and consumer-facing services, December 2021.

[iii] Ibid.

[iv] “GDP Monthly Estimate, UK: December 2021,” Ellis Best, ONS, 11/2/2021.

[v] Ibid.

[vi] Source: FactSet, as of 11/2/2022. Q1 and Q2 2022 UK GDP consensus estimates, October 2021 – February 2022.

[vii] Ibid. Q3 and Q4 2022 UK GDP consensus estimates, February 2022.

[viii] Ibid. UK GDP, Q3 2009 – Q4 2019.

[ix] Ibid. UK GDP, Q2 2020 – Q3 2020.

[x] Source: ONS, as of 11/2/2022.

[xi] “International Comparisons of GDP During the Coronavirus (COVID-19) Pandemic,” Sumit Dey-Chowdhury, Niamh McAuley and Andrew Walton, ONS, 1/2/2021. Namely, the ONS measures the actual volume of public services like healthcare and education (such as the number of healthcare treatments or students’ school enrolment) in real GDP calculations, whereas other countries estimate them.

[xii] See note iv.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-07

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today