Personal Wealth Management / Politics

Italy’s Election: Let the Games Begin!

Although Italy probably won’t have a government for a while, we believe the likeliest outcome—gridlock—should be fine for Italian and eurozone equities.

Italy voted on Sunday, and as of Monday afternoon, here is what the results have revealed: The anti-establishment populists won the most votes, the second-place finisher is considered a failure (based on media coverage we have seen), the third-place finisher thinks it should govern the country, and the man who would be kingmaker is now seemingly an afterthought. We don’t know—and probably won’t know for a while—which parties will end up in government. Officials are still figuring out how many seats each party gets, and it will likely be a few weeks before President Sergio Mattarella decides which party leader should get the first attempt to form a government. So uncertainty hasn’t vanished from Italian politics. However, now that investors know the basic results, we think markets can start weighing potential outcomes—including the very high likelihood that whoever forms Italy’s next government, diverse coalitions are usually a recipe for gridlock, reducing the chances of major change. Considering media coverage shows investors broadly fear major change in Italy, we think gridlock throwing sand in the gears should bring relief. In our view, this should be positive for Italy and eurozone shares.

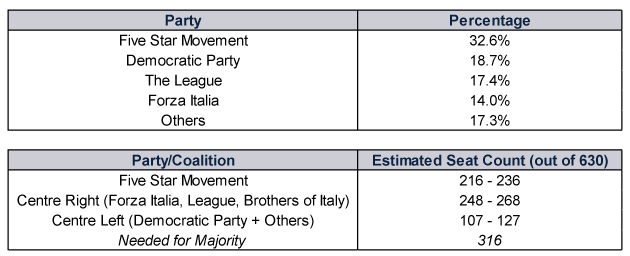

Exhibit 1 shows the vote tally as of Monday afternoon.

Exhibit 1: Estimated Election Results

Source: BBC News, as of 5/3/2018 at 5:00 PM GMT.

Whilst the centre-right coalition—symbolically headed (at least until Sunday) by Silvio Berlusconi’s Forza Italia—won the most seats, few seem to expect Berlusconi to be kingmaker. That honor rested on Forza Italia being top banana of the group. Instead, voters flocked to The League, a eurosceptic party also known as The Northern League. Its leader, Matteo Salvini, is now the coalition’s poster boy, and some observers now suspect he will abandon Forza Italia and instead seek an alliance with the anti-establishment Five Star Movement (M5S) and its equally telegenic leader, Luigi Di Maio. Early tallies have them combining for around 50% of the vote. Before the vote, Di Maio said M5S wasn’t interested in joining a formal coalition, preferring instead to form a minority government and partner with various parties on individual laws. Now, however, he has changed his tune, and M5S is apparently open for business.

Aside from Berlusconi, the other big “loser” in the eyes of the media was the Democratic Party and its leader, former Prime Minister Matteo Renzi. Although it came in second, it lost a big chunk of the vote and failed to win over even one-fifth of voters. With The League and M5S collectively trouncing the two mainstream parties, the traditional centre left and centre right will probably have to do some soul searching and figure out how to regain relevance—much as Greece’s centre-right opposition, the New Democracy Party, has done during the last three years. Left in disarray after the radical leftist Syriza party won Greece’s election in early 2015, New Democracy now tops polls.

We bring this up because what many investors fear today—M5S and The League forming a radical populist government that pulls Italy from the eurozone and EU—is, in our view, an echo of what investors feared when Syriza won in Greece. And Syriza and Greek Prime Minister Alexis Tsipras indeed came close to fulfilling those fears. But after a chaotic first six months in power, which included Syriza ripping up the bailout agreement and “winning” a referendum against austerity imposed by eurozone leadership, things settled down. Syriza didn’t pass much in the way of populist legislation, complied with the EU, passed some tough austerity measures (ignoring the referendum they called) and kept Greece in the eurozone. Tsipras and company talked a big game, but with only a tiny majority in parliament, they couldn’t make good on most campaign pledges.

If The League and M5S were to join forces, we expect it would go similarly. They would likely talk a lot but pass little, hamstrung by the divided parliament and their own internal divisions. After all, whilst both parties are populist, they differ ideologically. The League has a fairly hard right bent. M5S is much more of a melange, united by their hatred of the establishment, but it has a strong leftist faction. The League also seems more eurosceptic than M5S’s leadership, which has softened considerably toward Brussels in recent months. Not only have they backtracked on talk of leaving the eurozone or EU, but in recent interviews they claimed they never wanted to leave—they only wanted to use it as some leverage to reform the eurozone from the inside. So whilst both parties seem to want to thumb their nose at the establishment in Europe and their own country, it is difficult to see much common ground on matters of policy. We believe the same logic would likely apply to any broader coalition of Forza Italia, The League and M5S—another possibility discussed in the media.

That said, there are several permutations for potential coalition negotiations, and we think it is premature and fruitless to examine these in detail for now. Markets move on probabilities, not possibilities. In the coming weeks, as party leaders negotiate and consult with Mattarella, the outcome should become more clear, and we think it will then make sense then to assess specific policy pledges and their potential economic and market impact. For now, though, we think the biggest takeaway is that, whoever forms the next government, gridlock likely makes governing difficult—not much different from the status quo in Italy. A do-little government hasn’t kept Italy’s economy from growing or Italian equities from rising, and we expect shares shouldn’t mind having more of the same.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today