Personal Wealth Management / Market Analysis

Japan’s Resurgence in Perspective

Some things to note as Japanese stocks scale generational heights.

Broad Japanese equity indexes rose to multi-decade highs last week.[i] Coupled with some very high profile investors recently taking an interest, the climb is garnering a lot of attention.[ii] Whilst an interesting observation, we think more in-depth perspective is in order before loading up on Japan.

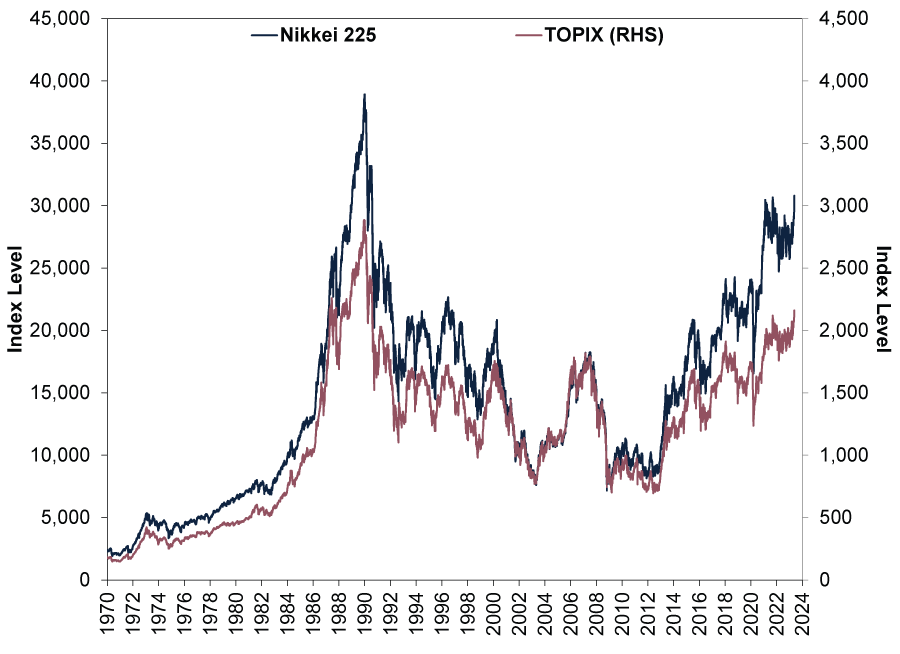

As Exhibit 1 shows, two of Japan’s most-followed indexes in publications we cover—the Nikkei 225 and TOPIX—are hitting 33-year highs. Those highs were the culmination of the epic late-1980s’ bubble, which Japanese markets have yet to regain.[iii] They also preceded the country’s infamous lost decade(s).[iv]

Exhibit 1: Japanese Equities Hitting Multi-Decade Highs in Yen

Source: FactSet, as of 22/5/2023. Nikkei 225 and TOPIX price indexes, 1/1/1970 –19/5/2023. Presented in Japanese yen. Currency fluctuations between the pound and yen may result in higher or lower investment returns.

Although these indexes remain below their respective 1990 peaks, they aren’t too far from them, which appears to be contributing to the latest attention and interest in Japan’s stock market from commentators we follow. Supposedly, this could be signalling its days of perceived economic stagnation and chronic deflation are finally ending. Japanese markets’ recent upturn also seemingly contrasts with other developed countries’ stock markets. The MSCI World Index, whilst recovering since the fall, remains below its December 2021 peak, unlike Japan’s gauges.[v]

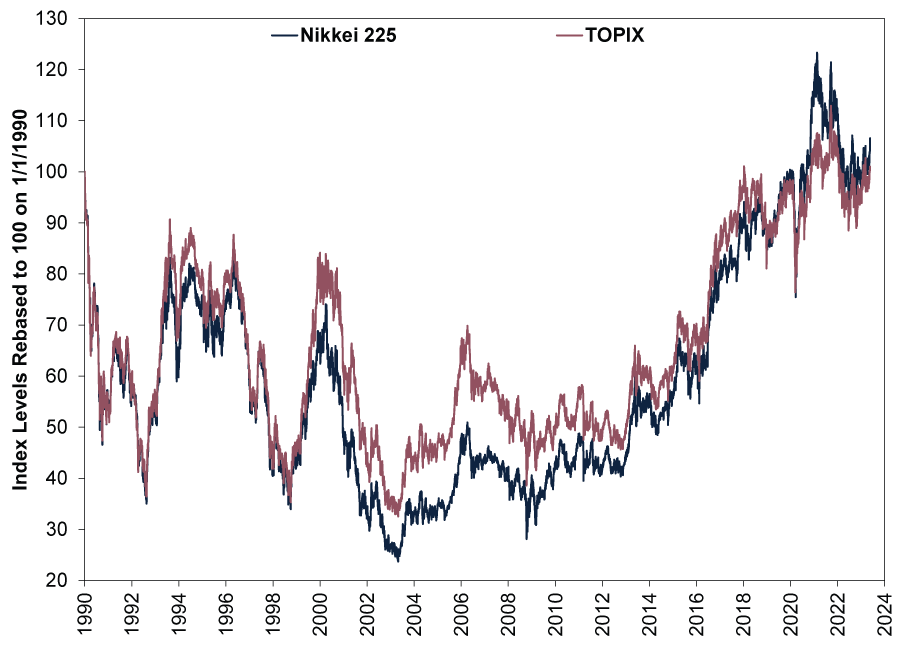

A few things for global investors to note here, though. Japanese stocks’ apparent strength evaporates after currency conversion. In yen terms, they may have usurped late-2021 highs, but in pounds, they are still off their peaks—just like other developed markets. (Exhibit 2) Global investors aren’t reaping outsized returns in Japan. Interestingly, too, the pound-denominated TOPIX and Nikkei 225 surpassed their 1990 peaks in 2018 and 2019, respectively, and we didn’t see many making a fuss at the time.

Exhibit 2: Japanese Equities Deflated by Pounds

Source: FactSet, as of 22/5/2023. Nikkei 225 and TOPIX price indexes in pounds, 1/1/1990 – 19/5/2023.

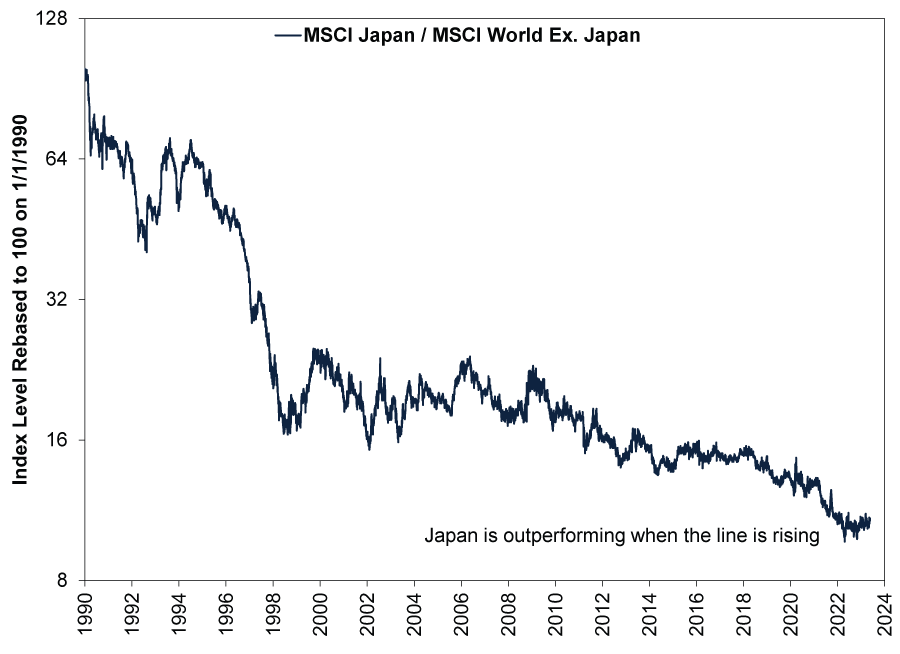

Also consider MSCI Japan relative to the MSCI World excluding Japan. (Exhibit 3; we use MSCI indexes here for comparison, but MSCI Japan hews very closely to the TOPIX, according to Fisher Investments’ research.) Japanese stocks’ recent outperformance is barely perceptible, in our view. Bigger bursts have come and gone in the last couple decades. This doesn’t rule out a change in trend, but so far at least, we have seen this movie before.[vi]

Exhibit 3: A Reversal in Japan’s Decades-Long Relative Downtrend?

Source: FactSet, as of 22/5/2023. MSCI Japan price index divided by MSCI World Ex. Japan price index, 1/1/1990 – 19/5/2023.

Of course, all that is backward looking. Some reports we read note Japanese stocks’ attractive valuations and Q1 economic improvement bode well for a continuation.[vii] But there are problems with this logic, in our view. For one, our research shows valuations aren’t predictive. Whilst Japan’s have been arguably attractive over the last decade—for naught thus far—the country’s 12-month forward price-to-earnings ratio has been continuously below the rest of developed world markets’ since 2014.[viii] Better-than-expected economic growth last quarter was nice, but past data aren’t predictive, either.[ix] Prior growth spurts haven’t done much to boost returns, and economics are only one driver.[x]

As always when investing, we think it is better to assess a country’s (or sector’s) forward-looking prospects relative to expectations versus everyone else’s. Here the latest enthusiasm stands on firmer ground, at least philosophically, in our view, considering the potential for improved corporate governance amidst increasing shareholder activism amongst high-profile global investors. Helping draw such interest: Western allies’ geopolitically motivated supply-chain shifts appear to favour select Japanese industries. For example, recent thawing of Japan’s diplomatic ties with South Korea is starting to yield greater trade and investment between the countries, like for advanced semiconductor manufacturing.[xi] Japan opening up to further foreign direct investment and stakeholders could jumpstart moribund sectors.

Whilst we welcome developments on these fronts, they don’t seem exactly new and likely lack surprise power. Japanese-South Korean bilateral trade hit record highs last year—before their current rapprochement.[xii] Maybe trade grows faster now than it would have otherwise. But it doesn’t strike us as a sea change no one expected.

Investors, foreign and domestic, have pressed for better corporate efficiency for years, too—without much impact.[xiii] Perhaps this time they will garner more change amongst corporate leaders—something we are watching. But we don’t see it as a widespread occurrence outside select stocks and industries thus far.

Meanwhile, other headwinds linger, such as Bank of Japan (BoJ) monetary policy, which we think continues to be counterproductive. Its policies of quantitative easing, negative interest rates and yield-curve control were never useful, in our view. The BoJ could always stop doing what hasn’t worked, but alas, it has balked at many chances to do so.[xiv]

Another issue: very slow progress on structural reform. We find Japan’s outdated labour laws and cross-shareholding arrangements disadvantage large swaths of its corporations, particularly domestically oriented ones insulated from foreign competition. Whilst there have been some changes over the past decade, those were well short of campaign pledges, and we don’t see much political appetite for tackling this under the present administration.

That said, some Japanese equity exposure does make sense to us, picking and choosing amongst Japan’s globally competitive multinationals, whose returns are less tied to domestic factors, according to our research. Like others, we appreciate the potential for corporate governance trends to help unlock long-neglected shareholder value in Japanese markets. However, adding heavily to Japanese holdings seemingly remains premature—in our view, it isn’t clear today’s hope will prove any more lasting than prior waves.

[i] Source: FactSet, as of 22/5/2023. Nikkei 225 and TOPIX price indexes in yen, 1/1/1970 – 19/5/2023. Currency fluctuations between the pound and yen may result in higher or lower investment returns.

[ii] “What Warren Buffett Is Buying in Japan’s Berkshire Hathaway Look-Alikes,” Tim Hornyak, CNBC, 5/5/2023.

[iii] “The Asset Price Bubble in Japan in the 1980s,” Shigenori Shiratsuka, Bank of International Settlements, 1/4/2005.

[iv] “Lost Decade in Japan: History and Causes,” Clay Halton, Investopedia, 27/9/2021.

[v] Source: FactSet, as of 22/5/2023. MSCI World returns with net dividends, 8/12/2021 – 19/5/2023.

[vi] Though we wouldn’t say no to more Kaiju (giant monster) flicks.

[vii] “A $518 Billion Rally Shows Japan Stocks Are All the Rage in 2023,” Ishika Mookerjee, Winnie Hsu and Elena Popina, Bloomberg, 19/5/2023. Accessed via Yahoo!

[viii] Source: FactSet, as of 22/5/2023. Statement based on MSCI Japan and MSCI World Ex. Japan next 12 month price-to-earnings ratios, January 2014 – April 2023.

[ix] Source: FactSet, as of 22/5/2023. Statement based on actual and consensus estimate for Japan GDP, Q1 2023.

[x] Source: FactSet, as of 22/5/2023. Statement based on Japan GDP, Q1 1990 – Q1 2023, and MSCI Japan returns with net dividends, 1/1/1990 – 19/5/2023.

[xi] “Samsung Eyes Chip Facility in Japan Amid Thaw in Seoul-Tokyo Relations,” Jo He-rim, The Korea Herald, 15/5/2023.

[xii] Source: FactSet, as of 22/5/2023. Statement based on Japan-South Korea bilateral trade, January 2022 – December 2022.

[xiii] “Japan’s Coming Wave of Reform,” Kei Okamura, Harvard Law School Forum on Corporate Governance, 11/1/2022.

[xiv] “Bank of Japan Defends Yield Curve Control Measures, Intends to Stick to Ultra-Easy Monetary Policy,” Sam Meredith, CNBC, 20/1/2023.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-14

-

Politics Can Germany Engineer Faster Growth at Last?2026-07-08

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-02

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today