Personal Wealth Management / Economics

Keeping Tabs on the Latest Economic Data

Amidst unsettling volatility, what do developed-world data say?

A bevy of economic data came out recently—to a fairly consistent negative reception amongst commentators we follow. But in our view, sour sentiment tied to the ongoing correction (short, sharp, sentiment-driven -10% to -20% decline) is causing many investors to underrate economic conditions today. Here are the major official releases from the developed world that hit the wires over the last week and our thoughts on what they signal.

The latest eurozone economic releases provide a glimpse at how inflation and the war in Ukraine are affecting data, as March reports reflect the first full month since the invasion. Real eurozone retail sales fell -0.4% m/m in March, led lower by a -2.9% drop in petrol sales.[i] But we think these data mostly just add detail to the currency bloc’s Q1 slowdown in gross domestic product growth (GDP, a government-produced measure of economic output). Since that report was released on 29 April, sales’ fall doesn’t seem like a shock to us.

Meanwhile, March German and French industrial production fell -3.9% m/m and -0.5%, respectively.[ii] An -11.2% m/m decline in vehicle production led Germany’s drop as component shortages weighed.[iii] A similar circumstance struck in France, as motor vehicle production slid -7.3% m/m.[iv] In our view, the situation is likely to improve when China reopens from its latest lockdowns and global supply chains adjust to the war’s impacting components usually sourced from Ukraine. We don’t think the process will be frictionless, but it does appear likely to see gradual improvement in due time.

Furthermore, data out on German factory orders and trade in March show continued weakness, as the former declined -4.7% m/m, again led lower by a -15.7% drop in vehicle production.[v] Manufacturing export orders fell -6.7% m/m with orders outside the eurozone down -13.2%.[vi] We think German trade data give some insight there. Germany’s overall exports declined -3.3% m/m in March, with sales to Russia plunging -62.3%, which Germany’s federal statistics office blamed on sanctions hitting trade.[vii] Exports to China, its biggest trading partner, fell -4.3% m/m amidst Chinese lockdowns.[viii] Whilst we don’t think this is great, these downswings are also largely one-offs—especially the drop in business to Russia, which greatly reduced Germany’s already small exports to the country.[ix] As for China, it may see continued negativity in the short term, but reopening is likely to boost exports eventually, in our view, as factories there resume sourcing German components.

Across the pond, US productivity garnered many headlines amongst financial publications we follow, as it suffered its biggest fall in 75 years. Whilst that perhaps sounds alarming, the data are just a twist on America’s Q1 GDP report, in our view, and the -7.5% annualised decline was simply a function of maths.[x] Productivity, as the US Bureau of Labor Statistics defines it, is output per hour. We suggest taking it apart, looking at the denominator first. Workers’ hours rose at a 5.5% annualised rate last quarter, suggesting growth created more work and jobs.[xi]

Meanwhile, output—as measured in this data series by GDP excluding government, non-profit and household sectors (i.e., private sector business production)—fell -2.4% annualised.[xii] But as we detailed earlier, private sector inventories mainly drove Q1 US GDP down; the inventory drawdown came after massive stockpiling in Q4 to counteract supply chain problems. Stripping out inventories, business spending and investment rose 9.2% annualised in Q1, a historically strong rate.[xiii] Bigger picture, we think productivity measures are backward-looking, and they normally fluctuate during an expansion.[xiv]

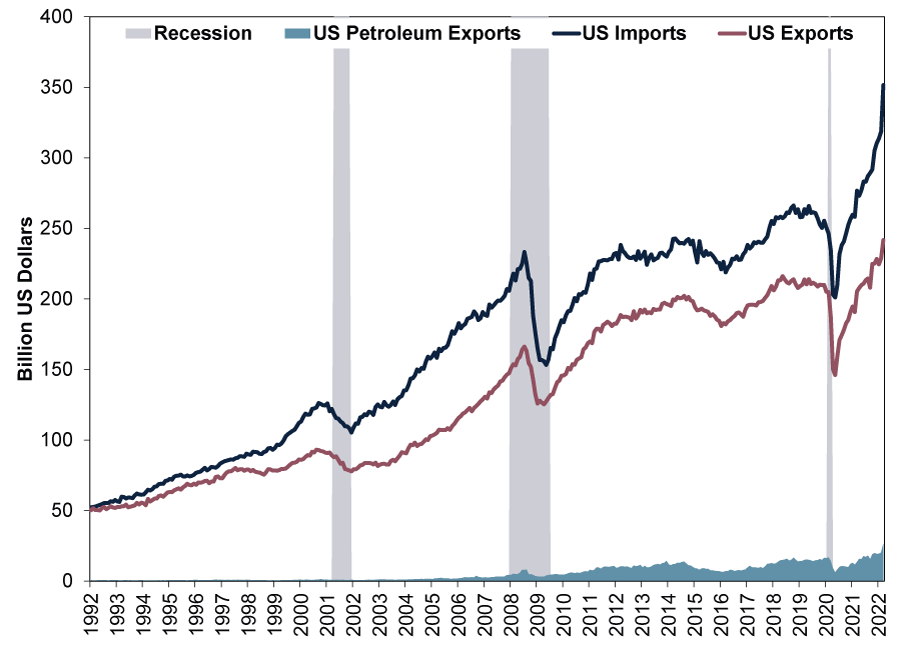

Headlines we followed last week were also abuzz over the US’s record-high trade deficit (meaning, the amount by which imports exceed exports). But we don’t think this was very meaningful for investors, either—not least because it reflected late-lagging March data, already embedded in Q1 GDP. Moreover, whilst deficit implies something wrong—and that belief appears widespread based on our coverage of financial commentary—imports exceeding exports isn’t inherently bad, in large part because imports reflect consumer demand. We think trade data showing they hit record highs is good![xv] (Exhibit 1) Even better, in our view, exports hit a record, too.[xvi] Judging by this measure, global trade doesn’t seem in retreat to us. Some commentators might say, yah but record amounts of trade just reflect sky-high prices—it is only inflation, as US monthly trade figures aren’t inflation-adjusted. But using quarterly US GDP data, which are inflation-adjusted, US trade still hit new highs in Q1.[xvii] Notably, US petroleum exports also hit new highs.[xviii] Worries about whether America’s oil industry will respond to high global prices abound amongst commentators we follow—in our view, this is one sign amongst many those concerns aren’t warranted.

Exhibit 1: US Trade Is Booming

Source: Federal Reserve Bank of St. Louis and US Census Bureau, as of 4/5/2022.

As Exhibit 1 shows, American imports have exceeded exports for the series’ entire history. The US habitually runs trade deficits, so that isn’t a relevant feature, in our view. More interesting, to us: The trade deficit is normally wide when the economy expands. Historically, the deficit usually shrinks when the economy is in recession, like 2008.[xix] So whilst the data are backward-looking, America’s record-high deficit today seems to us less like a sign of trouble and more like evidence the economy was growing at Q1’s close.

For investors, we don’t think stocks need perfection. Our research shows the bull market (period of generally rising equity prices) just needs reality to exceed current dour expectations. With so many commentators we follow expecting a lasting economic downturn, dour takes on mixed data suggest reality has a low bar to clear—a reason to remain bullish, in our view.

[i] Source: FactSet, as of 6/5/2022.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid.

[v] Ibid.

[vi] Ibid.

[vii] Source: Destatis, as of 4/5/2022.

[viii] See note i.

[ix] Source: Destatis, as of 4/5/2022. German exports to Russia were €0.9 billion in March, just 0.7% of Germany’s exports in the month.

[x] Source: US Bureau of Labor Statistics, as of 5/5/2022.

[xi] Ibid.

[xii] Ibid.

[xiii] Ibid.

[xiv] Ibid.

[xv] Source: US Census Bureau, as of 4/5/2022.

[xvi] Ibid.

[xvii] Source: Federal Reserve Bank of St. Louis, as of 4/5/2022.

[xviii] See note xv.

[xix] See note xvii.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

-

Market Analysis February’s Growthy Data—and the Iran War’s Souring Sentiment2026-03-06

-

Market Analysis Putting the Latest Private Credit Implosion in Perspective2026-03-06

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today