Personal Wealth Management / Market Analysis

On the BoE’s Dreary Forecast

In our view, markets don’t seem to agree the UK is heading for dark economic times.

The Bank of England (BoE) announced its biggest interest rate hike since 1995 last Thursday, raising the Bank Rate from 1.25% to 1.75%—but that wasn’t the day’s biggest news, based on our reading of financial commentary.[i] Paired with that rate hike was the BoE’s August Monetary Policy Report, which included the bank’s updated economic forecast. That forecast: Consumer Price Index (CPI) inflation reaching 13% y/y when the household energy price cap resets higher in October and a recession (a period of contracting economic output) starting that quarter and lasting all of 2023.[ii] (CPI is a government-produced measure of goods and services prices across the broad economy.) Looming over all of this is a fierce political debate on the BoE’s mandate and independence, which has featured in this summer’s Conservative Party leadership contest.[iii] We see some potential medium-term risks for UK stocks here, but not the ones that might seem most intuitive. Let us discuss.

When last we left the BoE in May, its top-line forecast was for inflation at 11% y/y and a -0.25% gross domestic product (GDP, a government-produced measure of economic output) contraction in 2023.[iv] Now it says the most probable scenario is CPI hitting 13% this autumn and GDP falling -1.25% in 2023.[v] Our May coverage discussed the BoE’s methodology and inputs at length, so we won’t rehash that here, but suffice it to say they mostly extrapolate recent conditions forward, which we think is a big reason why forecasts often don’t pan out. (Which, in turn, appears to be part of the reason for the political kerfuffle over the BoE’s status, which we will turn to momentarily.)

The BoE could prove correct. Wage growth, whilst strong in nominal terms, has lagged inflation, and in our view, the patchwork quilt of tax credits and rebates hasn’t offset the headwinds of this spring’s tax hikes and spiking household energy costs.[vi] We can envisage a potential scenario where GDP grows steadily in nominal terms (meaning, not adjusted for inflation) but shows as contraction once the inflation adjustment kicks in. That would represent a fall in living standards and, yes, recession by most definitions. Plus, the yield curve, which is a graphical representation of a single bond issuer’s interest rates across the spectrum of maturities, spent the past two weeks ever-so-slightly inverted, and as we write, it is just barely positive.[vii] Couple that with slight falls in broad lending and money supply in June, and we see some indication conditions are tightening.[viii]

But tightening doesn’t automatically mean full-blown credit crunch, in our view. As the Monetary Policy Report also documented, banks haven’t passed the recent rate hikes on to depositors.[ix] In our experience, this is a negative for households because it means inflation can erode their savings’ purchasing power at a swift pace. But it also could keep banks’ net interest margins—the difference between their borrowing costs and loan rates—wider than the yield curve would otherwise imply, especially with mortgage and other lending rates on the rise.[x] In our view, the BoE’s decision to begin selling down its gilt portfolio gradually this autumn, whilst widely viewed as tightening, is also likely to support higher long-term interest rates and the yield curve, which we think theoretically helps boost loan availability. We aren’t saying this points to a strong expansion necessarily, but we do think it builds a case for things going somewhat better than the BoE and most other forecasters we follow presently deem likely.

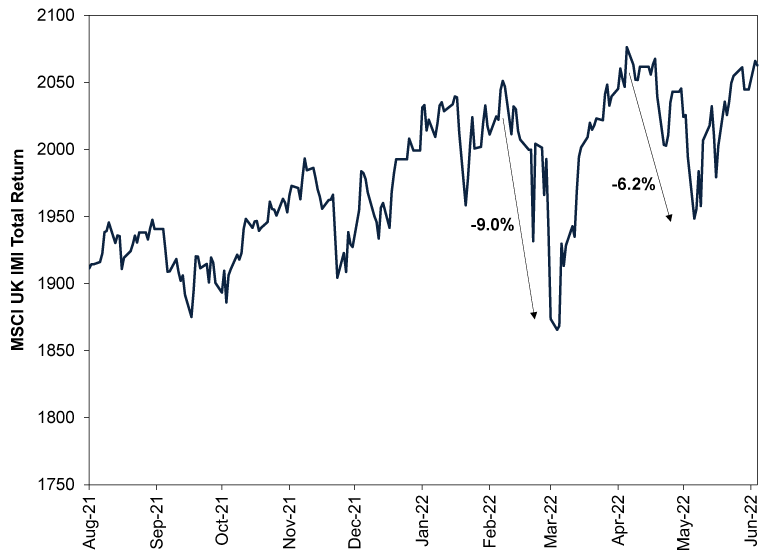

Here is another case: UK stocks don’t seem to agree that dark economic times are in the offing. On a local currency basis, the US, eurozone and many individual eurozone nations have endured bear markets this year.[xi] UK stocks, as Exhibit 1 shows, haven’t. Instead, they had two near-corrections (sentiment-fuelled declines milder than -10%) and, after a sharp rebound since 5 July, are a mere -2.2% below their April high.[xii] This 5 July low came after the BoE’s initial recession forecast, which most observers at the time called too optimistic. Plus, on the way down during that 8 April – 5 July pullback, the UK trailed global markets, with its more economically sensitive sectors and industries trailing—in our view, both consistent with markets pricing in expectations for an economic decline.[xiii] Economic forecasts broadly haven’t improved since that trough, yet UK stocks are climbing.[xiv] If experience is a reliable guide, financial commentators we follow will likely argue stocks are ignoring recession risk, but we think that is nearly impossible after over half a year of economists arguing the cost-of-living crisis would cause a recession.[xv] We think it is more likely markets are stating they perceive the BoE’s credibility as shaky and are assessing future conditions on their own—seeing a reality that goes better than many economists warn is likely.

Exhibit 1: The Resilient UK Stock Market

Source: FactSet, as of 4/8/2022. MSCI United Kingdom IMI total return in GBP, 4/8/2021 – 4/8/2022.

For now, we think this is good news. But longer term, it could set up the aforementioned risks. The BoE’s apparent lack of credibility doesn’t appear to be lost on the general public, the bank itself or—crucially—politicians. Current chief Andrew Bailey went on record this summer with the closest we have ever seen a monetary policymaker get to admitting his institution erred in defying its own forward guidance, not seeing the current inflation spike and generally being late to adapt to changing economic conditions.[xvi] In our view, that appeared to be aimed at heading off politicians from fiddling with the bank’s remit or revoking its independence, but it doesn’t seem to have worked. Foreign Secretary Liz Truss, who polls suggest is leading the Conservative Party’s leadership contest, has campaigned on reviewing the BoE’s mandate.[xvii] Commentators we follow in Conservative-leaning publications have argued in favour of this idea and, in some cases, outright revocation of the bank’s independence. Truss’s statements could be mere posturing, but it wouldn’t be the first time a Conservative government responded to the public’s rock-bottom economic sentiment by undertaking a regulatory review. David Cameron’s government did it after 2007 – 2009’s global financial crisis, resulting in a multiyear inquiry and overhaul that, in our view, extended uncertainty over UK Financials and, given the sector’s outsized presence in the country, UK stocks overall.[xviii] If Truss were to win and stick to her word in a meaningful way, we might see it boost uncertainty, which could weigh on returns.

Now, we aren’t saying all has gone perfectly at the bank, nor are we arguing its mandate to target 2% inflation over time is perfect. But in our opinion, the enforcement mechanism, which amounts to the BoE Governor occasionally answering to Parliament and having to write a letter to the Chancellor whenever the inflation rate deviates from the target by more than a percentage point, hasn’t exactly borne fruit over the years.

However, we think simply raising the question of whether and how to change the current system introduces uncertainty. In our view, in that event, investors would have to consider whether the BoE will start targeting nominal GDP instead of an inflation rate, as some have suggested. Or whether the inflation target will change. Or whether its independence will end, making it an arm of the Treasury and fiscal policy, giving politicians influence over interest rates. Or or or! We have seen opinion pieces arguing for all of these, and we think all are ignoring some potential downstream risks, which is an article for another day, if and when a review zeroes in on a potential change. For now, we find the mere possibility of rising uncertainty most important—and we think it bears watching.

Not that we are picking a horse in the leadership fight, mind you—we aren’t. In our view, either contender has the potential to champion policies that could extend uncertainty and create winners and losers. It is part of the reason why we think political gridlock within the Conservative Party will likely prove beneficial and lower legislative uncertainty. But in our experience, a regulatory review often exists outside of this process and could even extend to a potential Labour government, depending on when the next election occurs and who wins. All of it would probably create a cloudy overhang for UK stocks. We don’t view this as outright bearish, but should the review progress, it might be a factor for relative returns and could weigh on British stocks relative to the rest of the world. So keep an eye out and watch this space for more.

[i] “Monetary Policy Report,” Bank of England, August 2022. Bank Rate refers to short-term interest rates.

[ii] Ibid. A Consumer Price Index (CPI) is a government-produced index tracking prices of commonly consumed good and services. Inflation refers to broadly rising prices across an economy.

[iii] “Liz Truss Threatens to Interfere with Bank of England Mandate After Policy Disagreement,” Jon Stone, The Independent, 4/8/2022.

[iv] “Monetary Policy Report,” Bank of England, May 2022.

[v] See note i.

[vi] Source: FactSet, as of 4/8/2022. Year-Over-Year Percent Change in Average Hourly Earnings of Production and Nonsupervisory Employees and Year-Over-Year Consumer Price Index Percent Change, 31/12/2021 – 4/8/2022.

[vii] Source: Bank of England, as of 4/8/2022. Statement based on 3-month versus 10-year gilt yields.

[viii] Source: Bank of England, as of 4/8/2022.

[ix] See note i.

[x] Ibid.

[xi] Source: FactSet. As of 4/8/2022. Statement refers to MSCI EMU and MSCI Germany returns with net dividends in EUR and S&P 500 total returns in USD, 30/9/2021 – 4/8/2022. Currency fluctuations between the euro and pound and dollar and pound may result in higher or lower investment returns. A bear market is a prolonged, fundamentally driven broad equity market decline of -20% of worse.

[xii] Source: FactSet, as of 4/8/2022. MSCI United Kingdom Investible Market Index (IMI) total return in GBP, 8/4/2022 – 4/8/2022.

[xiii] Ibid. Statement based on MSCI United Kingdom IMI, MSCI United Kingdom IMI Financials and MSCI United Kingdom IMI Industrials total returns and MSCI World Index returns with net dividends in GBP, 8/4/2022 – 5/7/2022.

[xiv] Source: FactSet, as of 4/8/2022. MSCI United Kingdom IMI total return in GBP, 5/7/2022 – 4/8/2022.

[xv] “Britain's Cost of Living Crisis is Pushing Millions To The Brink,” Anna Cooban, CNN, 15/3/2022.

[xvi] “Andrew Bailey Battles to Protect His Empire as Tory Criticism Builds,” Simon Foy, The Telegraph, 19/7/2022. Accessed via MSN.

[xvii] See note iii.

[xviii] “The Independent Commission on Banking: The Vickers Report & the Parliamentary Commission on Banking Standards,” UK House of Commons Research Briefing, 30 December 2013.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Market Analysis February’s Growthy Data—and the Iran War’s Souring Sentiment2026-03-06

-

Market Analysis Putting the Latest Private Credit Implosion in Perspective2026-03-06

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today