Personal Wealth Management / Market Analysis

On Wednesday's Dreary British and Canadian Inflation Data

As inflation gets worse, so does sentiment.

The Anglosphere suffered another inflation blow Wednesday, this time courtesy of May data from Canada and the UK. Unsurprisingly, in our view, inflation (broadly rising prices across the economy) worsened in both nations, with consumer price index (CPI) inflation speeding to 7.7% y/y in Canada and 9.1% y/y in Britain.[i] And similarly unsurprisingly, in our view, coverage from commentators we follow was quite dour. We think that is understandable, considering inflation makes life difficult for many. It has also become a thorny political issue, so please understand that we are addressing this from an investing perspective only and don’t intend any political statements. To that end, whilst we don’t think either report yields any great insight from a data analysis standpoint, we find observers’ reactions rather illuminating on sentiment, as we think they show how far market outlooks have deteriorated. We hesitate to call it capitulation, but we think it does indicate it shouldn’t take much for reality to surprise positively later this year, which, in our view, could help bring stocks some relief.

In both countries, coverage from commentators we follow fixated on the alleged failure of monetary policy institutions to act against rising prices sooner and forecasts for inflation to get even worse before it gets better. There was a lot of blame tossed around by politicians, and a chorus of calls from publications we follow for the Bank of Canada and Bank of England (BoE) to do more to tackle the problem. Many of them also bemoaned that the rate hikes they view as necessary to beat inflation also risked “possibly” inducing recession (a decline in broad economic output), echoing US Federal Reserve head Jerome Powell’s comments to Congress Wednesday.[ii]

These forecasts for worse to come stem largely from the knowledge that oil and petrol prices continued rising in June, with food and metals prices also jumping.[iii] The weaker Canadian dollar and British pound also factored into warnings from observers, as they raise import costs.[iv] That got the blame for Canadian services prices rising 5.2% y/y, which we think seems rather suspicious considering US services inflation is even faster at 5.7% y/y in May and the dollar has soared this year.[v] In our view, a better explanation is that services prices are under a trio of pressures from reopening-fuelled demand, supply costs and labour shortages, creating a supply and demand mismatch. We think it is a global pandemic-driven dislocation that, whilst frustrating, is likely to ease as economies gradually return to pre-lockdown trends. But if observers’ hyper-focus on weak currencies creates much more dismal forecasts, then so much the better for stocks, in our view. Surprise power to lift markets up will theoretically be that much easier to attain.

We think there is very little monetary policy institutions can do to fix this. Monetary policy hits the economy at a lag, with many studies showing the effect materialises roughly 6 – 18 months out.[vi] Our research also finds it also tends to impact private investment more than consumer demand, which doesn’t solve the immediate problem, in our view. On the consumer goods front, monetary policy institutions have even less power, as our research shows inflation stems primarily from food and commodity prices. The Bank of Canada and BoE can influence money supply growth through their benchmark interest rates and their efforts to encourage or discourage the accumulation of bank reserves. But they can’t drill oil wells. They can’t build liquefied natural gas export and import terminals to increase supply into Europe. They can’t build next-generation nuclear power plants or arrange government permits for private entities to do so. They can’t reopen mothballed nuclear facilities and coal or natural gas-fired plants in Europe. They can’t open mines. They can’t end the war in Ukraine, plant grain or raise chickens and cattle. They can’t make China’s government abandon its zero-COVID strategy. You get the point. So, in our view, calls for aggressive rate hikes to solve this mess miss the mark.

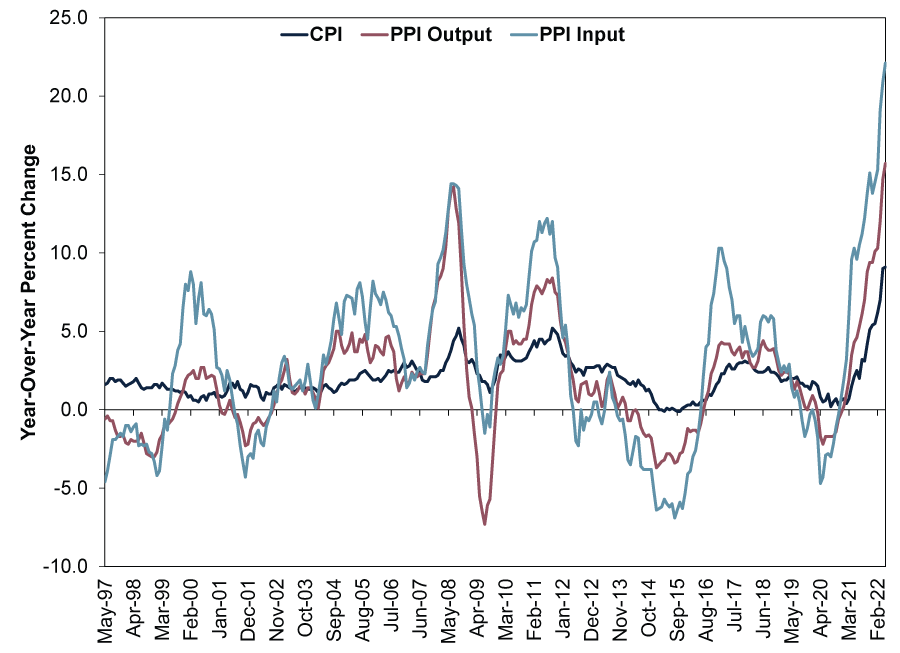

Some commentators we follow seemingly acknowledged this in their calls for inflation to get much worse from here, but we think their logic has some other holes—holes that should offer some encouragement, in our view. The UK released producer price inflation (PPI, a government-produced index tracking prices producers pay for inputs and charge wholesalers for finished goods) alongside CPI, and it was ugly. Manufacturers’ input prices jumped 22.1% y/y, and their output prices—the prices factories charge the wholesalers they sell to—rose 15.7%.[vii] Hence, many UK commentators warned businesses have plenty more cost increases to pass on to consumers, seemingly on the theory that consumer prices don’t yet fully reflect wholesale prices, which don’t yet fully reflect input costs.

However, we think a look at these series’ history dispels the myth that input prices predict wholesale prices predict consumer prices. As Exhibit 1 shows, all three have moved pretty similarly in terms of direction, with producer prices not leading consumer prices on a consistent basis. Many of their inflection points coincide. The differences are largely in magnitude, not direction.

Exhibit 1: Directionally, Consumer and Producer Prices Often Move Together

Source: UK Office for National Statistics, as of 22/6/2022. UK CPI, UK Output PPI and UK Input PPI, year-over-year percent change, May 1997 – May 2022.

When you consider how supply chains work, this makes sense, in our view. Commodity costs tend to swing wildly, leading to those outsized input PPI swings. But those don’t translate exactly to wholesale prices, which also reflect labour and fixed overhead costs plus markup to support profits—all of which can temper the amount factories have to raise their prices of finished goods. Similarly, wholesale prices are but one ingredient in consumer prices, which also reflect costs of labour, marketing, distribution and retailers’ fixed overhead as well as markup. So, even if retailers pass on the full wholesale price increase, those other factors may swing less, keeping the consumer price index relatively milder.

So, in our view, nothing about Wednesday’s PPI report should automatically suggest UK inflation will soar far higher from here. Now, we do think there is still more pain in store, stemming partly from ongoing fuel price increases and October’s pending increase to Britain’s household energy price cap, which fresh estimates show could rise about 50% from April.[viii] Given oil is also a key feedstock for all manner of consumer goods, we will likely continue seeing it impact non-energy inflation as well.[ix] The BoE currently sees UK inflation hitting 11% y/y later this year, and it could prove correct.[x] But those forecasts aren’t new or likely to be surprising to markets, which we think are also discounting the hysteria over PPI and handwringing over monetary policy institutions’ fecklessness. All of these perceived negatives and projections are getting baked into stock prices, in our view.

The lower expectations go, the easier we think it is for reality to deliver a positive surprise. Less bad than feared often suffices in this environment. We recognise that isn’t what people will want to hear about inflation at a fundamental day-to-day living level, as rising living costs can have a devastating personal impact. But, in our experience, markets are cold-hearted to such things, and we suspect any indication that inflation won’t peak as high or last as long as commentators we follow warn would generate some welcome relief for stocks.

We think investors should always remember: Markets don’t wait for perfection and all-clear signals. Our research shows they move first, and recoveries often happen when things look darkest. Again, we aren’t saying that time is now—inflection points are only ever visible in hindsight. More negativity could be in store. But if stocks are at all efficient—which we think they are—then we think a recovery will probably begin before the world fathoms inflation relief. With commentators basing dreary forecasts on (in our view) faulty inputs and logic, that relief could arrive much sooner than suggested, in our view.

[i] Source: FactSet, as of 22/6/2022. A Consumer Price Index (CPI) is a government-produced index tracking prices of commonly consumed goods and services.

[ii] “Powell Says Soft Landing ‘Very Challenging;’ Recession Possible,” Craig Torres and Diego Areas Munhoz, Bloomberg, 22/6/2022. Accessed through Yahoo! Finance.

[iii] Source: FactSet, as of 22/6/2022. Statement based on Brent Crude Oil spot prices, and “Inflation and the Cost of Living for UK Households, Overview: June 2022,” UK Office for National Statistics, 22/6/2022, and “Weekly Pricing Pulse: Commodity Prices Edge Up Reversing Last Week’s Declines,” Michael Dall, S&P Global, 9/6/2022.

[iv] Source: FactSet, as of 22/6/2022. Note: Having a weaker currency means companies importing goods to produce their own, have to spend more to import component parts. Whilst this can sound harrowing initially, we think investors need to remember the other side of the equation, and a key mitigating factor: those companies’ exports become cheaper and therefore experience higher demand.

[v] Source: FactSet, as of 22/6/2022.

[vi] “The Role of Forecasting in Meeting Inflation Targets: The Case of New Zealand,” Gregory B. Christainsen, Cato Journal, Vol. 17, No. 1, Cato Institute, Spring/Summer 1997.

[vii] Source: UK Office for National Statistics, as of 22/6/2022.

[viii] Source: FactSet, as of 23/6/2022. Statement based on Brent Crude Oil spot prices, and “Energy Price Cap in Britain Could Near £3,000 This Autumn,” Harry Taylor, The Guardian, 20/6/2022.

[ix] “Uses of Crude Oil,” Staff, BBC, 2022.

[x] “Bank Rate Increased to 1.25% - June 2022,” Bank of England, 16/6/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today