Personal Wealth Management /

One Year Later Italy Seems Fine

Teaser: Bond yields are down, GDP is growing, and the populist government appears innocuous.

A year ago, financial pundits seemingly couldn’t stop writing of the risks lurking in Italy’s chaotic political scene. Two months after a general election, political leaders still hadn’t formed a government, but the potential for a populist coalition between the anti-establishment Five Star Movement and far-right The League loomed large. Many publications we monitored warned of the possibility for the eurozone’s third-largest economy to spiral into political chaos, recession and—if a populist government implemented all of its parties’ campaign pledges—fail to make interest or principal payments on its sovereign debt. Some thought Italian interest rates would soon soar as the very populist government many dreaded indeed took power at May’s close, and as economic data weakened in 2018’s second half, they suspected the worst fears were coming true.[i] Yet now, a year later, checking in on Italy’s situation reveals the government hasn’t done much, in our view, whilst interest rates are down, and gross domestic product (GDP, a government-produced estimate of national economic output) is growing again.[ii] For investors, we think this highlights a timeless lesson: Financial publications’ big headline fears fizzle frequently, leaving a benign reality in their wake.

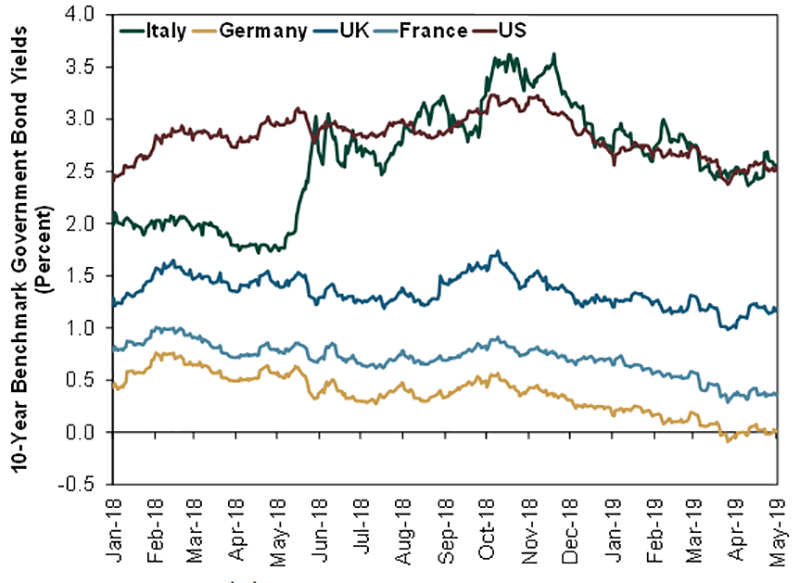

When Italy’s populist parties formed a government, they shook up status quo politics. They pledged bold policy initiatives, made incendiary statements and vowed to take on the eurozone political establishment. They hinted they wouldn’t abide deficit limits and edicts from Brussels bureaucrats, whilst championing greater social welfare, flat taxes and infrastructure improvements. We think it is fair to say populist parties’ manifestoes shook Italy’s traditional political centre and, for a while, its markets. Italian 10-year government bond yields jumped from below 2% on the early-March election day to more than 3.6% in October, amidst budget disagreements between Rome and Brussels, which sparked debt default fears.[iii] Meanwhile, Italian GDP fell two straight quarters in Q3 and Q4 2018, meeting one popular definition of recession.[iv]

Today, the political, economic and financial environment appears calmer. Rome and Brussels resolved their budget dispute, and Italian 10-year yields are down to 2.55%, effectively even with 10-year US Treasury yields.[v] Q1 Italian GDP rose 0.2% q/q, perhaps signalling the start of an economic recovery.[vi] Even last year’s GDP contraction looks more benign than many initially thought, with government spending and a drop in private inventories being the sole negative contributors in Q4 2018.[vii] Pure private sector components, which we view as final consumption expenditure and gross fixed capital formation, were positive.[viii] Q4 growth in these areas wasn’t spectacular, in our view, but it also wasn’t negative. Now that GDP overall has resumed growing, we think Italy’s underlying growth drivers may be more visible.

Another lesson we think is valuable: Beware reading too much into any single country’s interest rate movements in the short term. Last year we observed financial pundits singling out threats from rising Italian bond yields, but a look at other major nations’ interest rates shows they were merely part of a global move in 2018’s second half. As Exhibit 1 shows, other major developed markets’ yields also rose last summer and autumn before reversing course in late November. Italian yields were more volatile than the others during this time, but directionally, they more or less matched. Historically, any one major developed nation’s yields generally hasn’t deviated from the rest over sustained periods.

Exhibit 1: 10-Year Government Bond Yields

Source: FactSet, as of 3/5/2019. 10-year benchmark government bond yields for Italy, Germany, the UK, France and the US, 1/1/2018 – 2/5/2019. US yield is the constant-maturity 10-year US Treasury yield.

Populists have apparently also moderated. Despite some continued bluster, the new government hasn’t accomplished much, in our view. Instead, we think reality has set in. A seeming hodgepodge of leftists, so-called techno-libertarians, anti-establishment types without strong ideological leanings, and hard-right types was likely never going to agree on much. Rather than revolution, this government appears mired in gridlock. Reforms passed by the prior centrist administrations have largely gone untouched—a good example of what founder, Fisher Investments worldwide, Ken Fisher, likes to call the “pancaking” of western developed nations’ politics. Political spectrums, which can resemble bell curves when envisaged as a chart, once concentrated in the centre, but they have flattened out as formerly fringe parties have eroded centrists’ power. We think that tends to bring more coalitions like Italy’s, cobbled together from parties that likely agree on little to nothing. For markets, this shouldn’t be a problem—in our view, it keeps legislative risk low, easing the fears that accompanied this coalition’s political emergence.

Our advice: The next time big seemingly scary stories dominate financial headlines, remember Italy during this period. Even when the thing many people feared actually happened, disaster didn’t strike, and markets started recovering long before many suspected they would.

[i] “EU Fears New Italian Policies Could Set Stage for Next Euro Zone Crisis,” Jan Strupczewski, Reuters, 17/5/2018. https://www.reuters.com/article/us-italy-politics-eu-worry/eu-fears-new-italian-policies-could-set-stage-for-next-euro-zone-crisis-idUSKCN1II1R9

[ii] Source: FactSet, as of 3/5/2019. Statement based on Italy’s 10-year benchmark government bond yield, 3/5/2018 – 3/5/2019, and real GDP growth, Q1 2019.

[iii] Ibid. Italian 10-year benchmark government bond yield, 4/3/2018 – 18/10/2018.

[iv] Ibid. Real GDP growth, seasonally adjusted, Q3 2018 – Q4 2018.

[v] Ibid. Italian 10-year benchmark government bond yield and constant-maturity 10-year US Treasury yield, 3/5/2019.

[vi] Ibid. Real GDP growth, seasonally adjusted, Q1 2019.

[vii] Source: Istat, as of 3/5/2019. Quarterly National Accounts, Q4 2018.

[viii] Ibid.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today