Personal Wealth Management / Market Volatility

Our Perspective on April’s Return to Rocky Markets

Our research shows continued volatility—and even a possible retest of March’s low—isn’t uncommon for a correction.

War and atrocity. Food and energy price spikes. Widening Chinese lockdowns and supply chain disruption. Big swings in both stock and bond markets.[i] Thus far, based on our observations of investor sentiment and behaviour, we find 2022—which features this bull market’s (period of generally rising equity prices) first correction (typically a short, sharp, sentiment-driven -10% to -20% pullback)—has been difficult for many investors. After 8 March’s low, stocks rose to close the month, only to see renewed volatility in April send markets close to retesting that mark on Tuesday.[ii] Many commentators we follow warn worse lies ahead. But, whilst such volatile times like this can be hard, we think they aren’t atypical during corrections. To us, they call for calm—and perspective: Corrections are never easy, but as we will show, they are a normal part of bull markets. Patience is likely to prove beneficial, in our view.

Corrections are chiefly sentiment swings, which often start with some plausible seeming negative story, in our experience. In this case, it seems to us inflation, war and more recently China’s latest lockdowns underpin the move, with tragic news out of Ukraine stirring investors’ emotions alongside volatility. Our research shows being sentiment-driven gives corrections one of their toughest features: They are impossible to predict—and time. We aren’t aware of anyone with a proven history of circumventing sentiment-driven negativity and corrections. We also find such shifts happen suddenly; there generally won’t be any warning one is about to start—and no all-clear signal when it is over. The beginning and end are apparent in hindsight only.

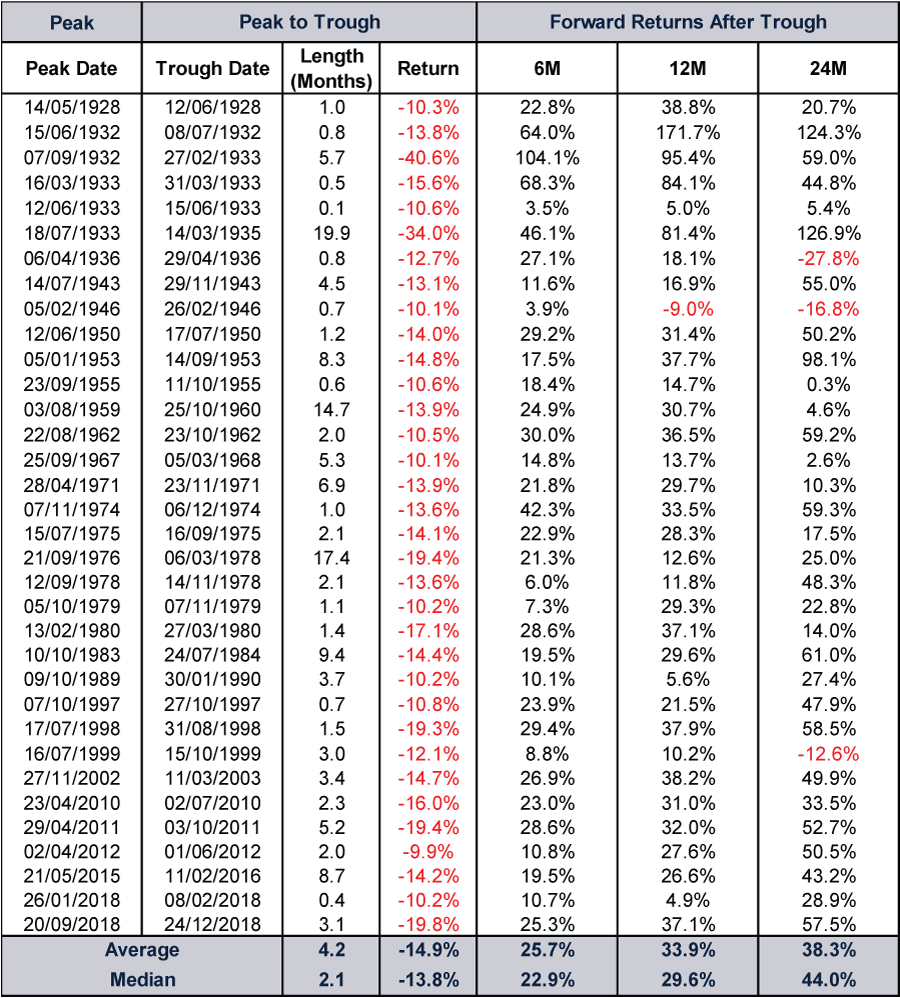

But based on our historical research, there is a silver lining: Recoveries are usually about as fast as the drop, with stocks normally continuing to churn higher thereafter. Exhibit 1 shows all of America’s S&P 500 corrections since 1928 presented in US dollars, which we use for its long history. If the current correction resolves as others have—and we see little reason to think this time is different—the recovery to new highs and beyond could come much sooner than many commentators we follow seem to anticipate today.

Exhibit 1: Historical S&P 500 Corrections

Source: Global Financial Data, Inc., as of 5/4/2022. S&P 500 Index price returns during and after corrections, 3/1/1928 – 31/12/2021. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

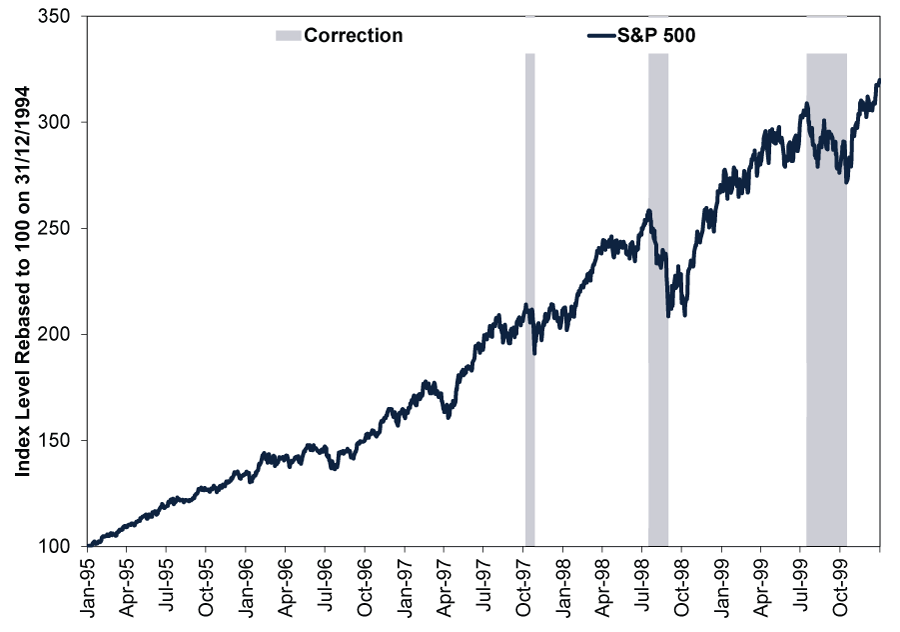

Those recoveries are rarely straight lines, according to our analysis—there is very often volatility after the low, or even W-shaped corrections. Exhibit 2 depicts three late-1990s’ corrections from the table, which we think offers some historical perspective on corrections’ frequency and variety—length, magnitude and shape—during a bull market. The first, in 1997, was a V-shaped correction, in our view. The latter, 1999’s, was arguably more W-shaped. But we think 1998’s W-shaped correction quintessentially illustrates double-bottom corrections. From its July peak to August trough, the -19% drop was swift. But it wasn’t a smooth recovery. An initial jump in September faded, with stocks retesting the lows by early October. To many investors at the time, we imagine that may have felt like a gut punch—discouraging. But three months after August’s low, stocks were back to new highs, even with the retest. Full-year returns ended up being great after a strong, late rally wiped away bad memories from the correction—if investors held on. Corrections can try investors’ patience, but given their unpredictability, we think that patience is the best tool today for an investor seeking long-term growth.

Exhibit 2: 1998’s Correction Wiped Out Year-to-Date Gains, but Stocks Still Finished (a Lot) Higher

Source: FactSet, as of 26/4/2022. S&P 500 Index price returns, 31/12/1994 – 31/12/1999. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

Our research shows bear markets (typically prolonged declines exceeding -20% with fundamental causes) start one of two ways, and neither cause is present currently. We call them the wall and the wallop. The wall refers to the proverbial wall of worry bull markets are often said to climb. As Sir John Templeton described famously: “Bull markets are born on pessimism, grow on scepticism, mature on optimism and die on euphoria.”[iii] In our view, it appears pretty clear we are far from euphoria. We define a wallop as when a multitrillion-pound negative—like worldwide pandemic lockdowns—wipes out global economic growth unexpectedly. Widely watched warnings circulating in the news may be grounded in reality, but we don’t think they qualify as wallops because they lack the scale—although we are monitoring them in case they snowball—and enough surprise power to pack a wallop.

In our view, the speed of the drop, widely publicised nature of the associated news stories, sentiment impact and lack of wallop scale strongly suggest the negativity we have seen in early 2022 is a correction, not a bear market. It is hard, and we hate to sound repetitive, but we think corrections call for calm—not action. Enduring sometimes-rocky roads isn’t fun, but for investors needing equity-like returns to finance their long-term goals and objectives, there is no avoiding them, in our experience.

[i] Source: FactSet, as of 27/4/2022. Statement based on MSCI World Index returns with net dividends and 10-year gilt yields, 31/12/2021 – 26/4/2022.

[ii] Ibid.

[iii] “Bull Markets Are Born on Pessimism, Grow on Skepticism, Mature on Optimism, and Die on Euphoria,” Barry Popik, The Big Apple, 15/12/2010.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-02

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

-

Market Analysis Reviewing America’s Q1 Earnings and What Q2 Expectations Say2026-06-23

-

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today