Personal Wealth Management / Market Analysis

Q3 US Corporate Earnings Take Shape

Whilst backward-looking, the results can offer clarity and clear some fog.

With about 85% of America’s S&P 500 companies reporting Q3 corporate earnings, what can global investors glean from them?[i] As US stocks constitute 70% of the MSCI World Index’s market capitalisation, we think a look at their earnings—and what they reveal about how Corporate America is weathering this year’s storms—can provide useful insights.[ii] Beneath the surface of what we think are overall mixed headline results, we see strong indications that inflation (rising goods and services prices across the broad economy), supply chain issues and other headwinds are working their way through the system. We don’t think this predicts stocks, but it adds colour to what markets have spent this year pricing in and suggests to us warnings from commentators we follow of much greater pain from here will likely miss the mark.

As many analysts we read point out, earnings that exclude the Energy sector are down—not terribly much, but perhaps consistent with what this year’s mild bear market (typically prolonged fundamentally driven decline exceeding -20%) in US dollar terms hinted at in advance.[iii] Whilst the S&P 500’s Q3 earnings are up 2.2% y/y (combining actual results and remaining estimates in US dollars), Energy’s 138.6% haul is swelling the figure.[iv] Excluding Energy, they fell -5.3% y/y, the second-straight decline after Q2’s -4.0%.[v]

The weakest sectors were Communication Services, Financials and Materials, which are facing year-over-year earnings declines of -22.2%, -20.0% and -15.9%, respectively.[vi] Based on our research, declining ad revenue was Communication Services biggest detractor, whilst Financials’ decline is partially an accounting construct—banks’ loan loss provisioning is contributing to their earnings weakness, especially after releasing reserves last year. US accounting rules require banks to set aside reserves based on projected potential losses over the life of a loan, which can fluctuate with economic forecasts, and this gets booked as a cost in their financial results. Banks are also allowed to release these provisions as their forecasted future losses change, which gets booked as income in their financial results. Then, by our analysis, commodity prices’ steep drop from a year ago seems mostly behind Materials’ profit slide. All this is backward looking, which our research shows doesn’t affect forward-looking stocks fundamentally. So we wouldn’t presume any of it signals worse to come for the sectors in question or the S&P 500 overall. Nor do we think Energy’s jump is some massively bullish feature looking forward—it is an artefact of higher oil and gas prices, in our view.

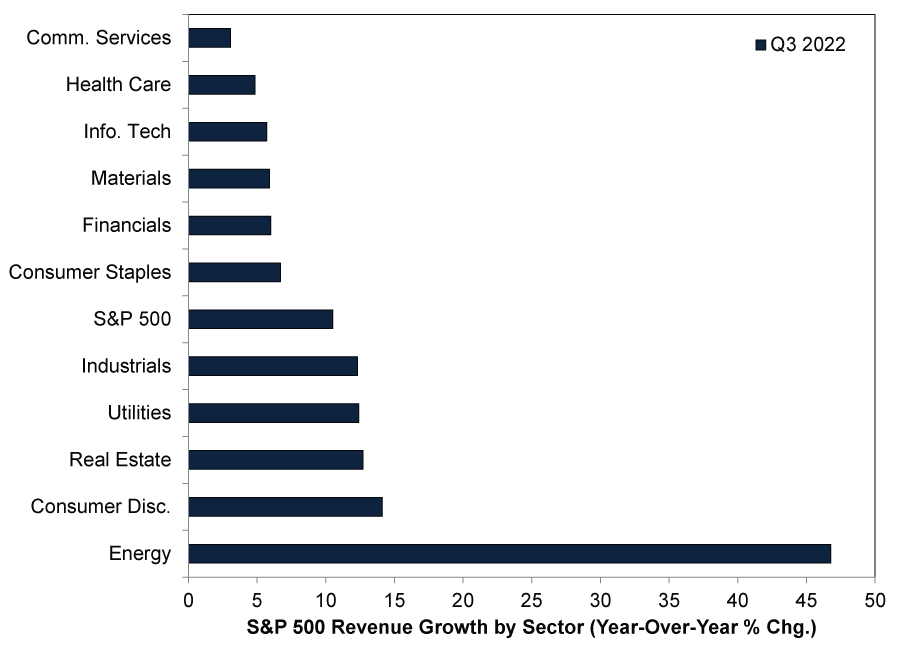

Notably though, whilst sales have decelerated, they remain historically strong—and broad-based: All sectors are seeing year-over-year revenue growth. (Exhibits 1 & 2)

Exhibit 1: Sales Growth Is Decelerating, but Still Relatively Strong

Source: FactSet, as of 4/11/2022. US recession shading based on National Bureau of Economic Research business cycle dates. A recession is a prolonged, broad-based contraction in economic activity.

Exhibit 2: Positive Sector Revenue Growth Across the Board

Source: FactSet, as of 4/11/2022.

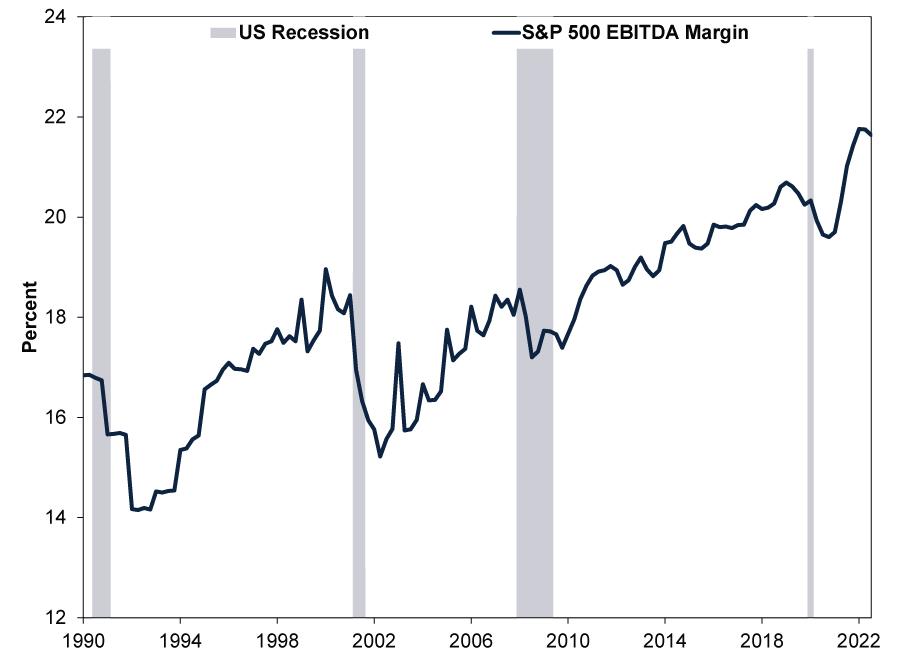

We think this means that, in general, earnings are largely down on costs eating into profit margins. However, businesses’ (overall and on average) having the luxury of using fat margins as a buffer to absorb more cost increases without passing them on to customers speaks to Corporate America’s better-than-appreciated resiliency, in our view. Consider: Even with this, Exhibit 3 shows profit margins remain high by historical standards. (Note: We use earnings before interest, taxes, depreciation and amortisation, or EBITDA, to better aggregate companies’ and industries’ profitability on a like-for-like basis.)

Exhibit 3: Profit Margins Are Under Pressure, but Still Relatively High

Source: FactSet, as of 4/11/2022. US recession shading based on National Bureau of Economic Research business cycle dates. A recession is a prolonged, broad-based contraction in economic activity.

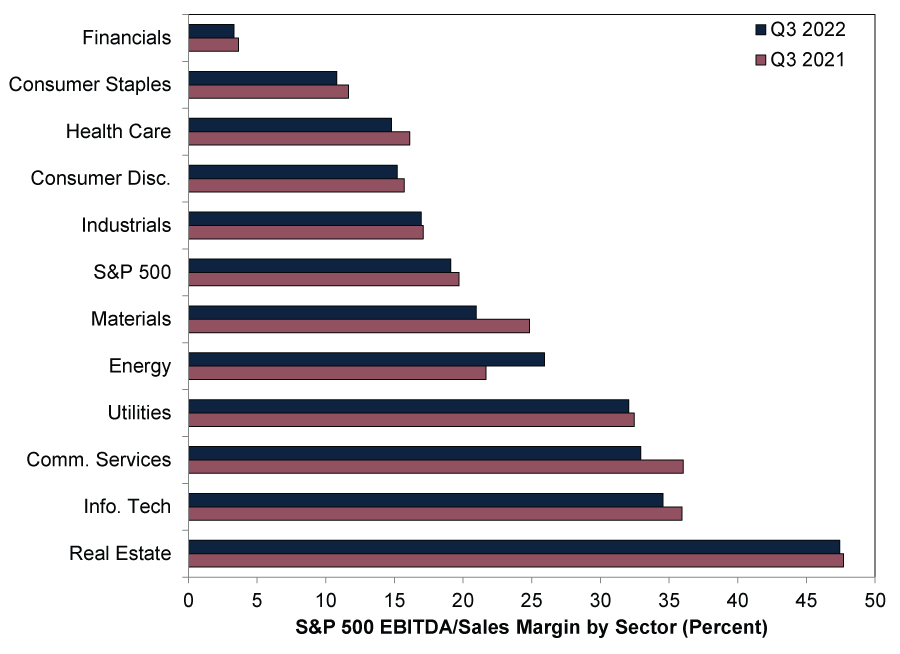

And it isn’t just because of Energy, as Exhibit 4 shows. Although most sectors have seen margins shrink somewhat, they have done an admirable job maintaining margins within sight of peak levels, in our view. Earnings may be down, but with S&P 500 revenue up a strong 10.5% y/y and margins holding up relatively well, profits’ two-quarter retrenchment doesn’t look disastrous to us—it looks shallow.

Exhibit 4: Corporate Profitability by Sector

Source: FactSet, as of 4/11/2022.

We think the question for stocks—and sector positioning—is what the next 3 – 30 months will bring relative to what stocks have priced in by now. In our view, stocks, which peaked at 2022’s start in US dollar terms, appear to have anticipated Q2 and Q3’s S&P 500 Ex. Energy earnings dip ahead of time.[vii] With the bear market going on 11 months, Energy is the only sector with positive year-to-date returns.[viii] On the other hand, Communication Services has faced the toughest sledding, with Consumer Discretionary and Real Estate not too far behind.[ix] Considering our research shows stocks move ahead of corporate earnings, we think it seems fair to surmise that stocks already reflect what these earnings results show.

Of course, we think past performance says nothing about what to expect going forward. Take Real Estate and Energy. By Q3’s backward-looking numbers, Real Estate enjoyed wide margins on top of above-average revenue growth. (Exhibits 2 & 4) Yet as many commentators we follow note, the sector faces headwinds in America, which markets seem to be pricing in. On the residential side, record housing units in the construction pipeline increase supply, and mortgage rates at two-decade highs likely limit demand.[x] Then on the commercial front, vacancy rates remain elevated post-pandemic—rents have stagnated as a result.[xi]

Energy has benefitted from substantial tailwinds—the big (and only) inflation winner this year—but will that last? Oil prices, which we think are Energy’s main driver, peaked 8 March in US dollars.[xii] West Texas Intermediate crude—America’s benchmark oil price—has fallen -28.7% since.[xiii] Meanwhile, the US Energy Information Administration released figures on Halloween noting crude production is closing in on 12 million barrels per day.[xiv] Output rose 0.9% m/m in August and 6.2% y/y to its highest level since March 2020.[xv] (Also notable: Natural gas production hit a new record high.)[xvi] Then, too, global supply has exceeded demand since July, even with OPEC’s production cuts.[xvii]

As Exhibit 2 showed, Energy’s revenue growth is still running at 46.8% y/y, but that is almost half Q2’s rate and appears tied largely to base effects. We doubt triple-digit earnings growth persists. We aren’t alone. Analysts are pencilling in year-over-year decline starting in Q2 next year.[xviii]

Maybe commercial property resurges, driving rents higher—or oil prices rocket anew from here as demand outstrips supply—for whatever reason, say, in-office work and commutes come back in vogue. The discrepancy between current forecasts and the ensuing reality might favour Real Estate and Energy. But it will be how each sector’s supply and demand fundamentals actually turn out—relative to the earnings prospects embedded in their prices—that will determine their performance moving forward, in our view. We don’t think Q3 earnings can predict that.

Many sectors have seen earnings declines this year—to greater or lesser degree. But this looks to us largely consistent with the market moves we have already seen year to date. This doesn’t say anything about returns ahead, but we think seeing profit downturns’ actual extent helps markets move past lingering concerns.

[i] Source: FactSet Earnings Insight, as of 4/11/2022.

[ii] Source: FactSet, as of 4/11/2022. US stocks’ market capitalisation percentage of the MSCI World Index, 3/11/2022. Market capitalisation—a stock or index’s price multiplied by the number of shares outstanding—is a measure of total market value.

[iii] Ibid. Statement based on MSCI World Index return with net dividends, 4/1/2022 – 3/11/2022. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[iv] Source: FactSet, as of 4/11/2022.

[v] Ibid.

[vi] Ibid.

[vii] Source: FactSet, as of 4/11/2022. Statement based on S&P 500 total returns in USD, 3/1/2022. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[viii] Source: FactSet, as of 4/11/2022. Statement based on year-to-date S&P 500 sector total returns in USD, 31/12/2021 – 3/11/2022. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[ix] Ibid.

[x] Source: Federal Reserve Bank of St. Louis, as of 4/11/2022. 30-Year Fixed Rate Mortgage Average in the United States, 5/4/2002 – 3/11/2022. “September Housing Starts: Record Number of Housing Units Under Construction,” Bill McBride, Calculated Risk, 19/10/2022.

[xi] “Reis: Office Vacancy Rate Unchanged in Q3, Mall Vacancy Rate Unchanged,” Bill McBride, Calculated Risk, 5/10/2022.

[xii] Source: FactSet, as of 4/11/2022. WTI crude oil price per barrel in USD, 8/3/2022 – 3/11/2022.

[xiii] Ibid.

[xiv] “U.S. Oil Production Nears 12 Mln Barrels/Day, at Pre-Pandemic High,” Arathy Somasekhar, Reuters, 31/10/2022.

[xv] Ibid.

[xvi] Ibid.

[xvii] Source: FactSet, as of 4/11/2022. Monthly global oil supply and demand, July 2022 – October 2022.

[xviii] Source: FactSet Earnings Insight, as of 28/10/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

-

Market Analysis Reviewing America’s Q1 Earnings and What Q2 Expectations Say2026-06-23

-

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-23

-

Macro Insights SpaceX IPO and Rising Equity Supply2026-06-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today