Personal Wealth Management / Market Analysis

Russian Oil Price Caps Seem Mostly Symbolic

For global energy markets, we think supply-demand fundamentals likely outweigh the West’s new moves against Russia’s oil industry.

EU members agreed to a $60 per barrel price cap on seaborne Russian oil last Friday, following through on a US-led aim to limit, if not sever, financing sources for Moscow’s brutal war in Ukraine—without destabilising global oil markets.[i] The EU, Group-of-Seven nations (G7) and Australia implemented it Monday, although there is a 45-day transition period before it is enforced.[ii] Coverage suggests this “watershed” moment ushers in an “unpredictable new phase” for oil markets, with Turkey’s premature enforcement efforts getting wide attention from commentators we follow as alleged evidence.[iii] But in our view, there are few surprises here, as the cap has been under public discussion for months. Furthermore, it was set above discounted levels Russia reportedly sells oil at now—mainly to Chinese and Indian buyers, who aren’t even party to the agreement.[iv] Hence, we don’t see this changing much for markets.

Western governments first proposed a price cap this summer.[v] But only now, after hemming and hawing for weeks, has the EU been able to settle on a $60 ceiling for Russian oil delivered by ship.[vi] This filled in a key detail from the G7’s September plan, coming alongside the EU’s embargo on buying Russian crude, which has gradually taken effect this year.[vii] In practice, the new price cap bans Western companies from insuring, financing or shipping Russian oil bought above $60.[viii] That price level is subject to change and will be reviewed every two months starting in mid-January.[ix] Theoretically, it will be adjusted to stay at least -5% below average Russian crude oil prices—as tabulated by the International Energy Agency (IEA), not necessarily actual transactions, which are harder to track—if all 27 EU member countries and the G7 agree unanimously. Upon any change, there would be a 90-day grace period for ships at sea to comply.

Also note what the price cap doesn’t cover: Russian natural gas, which Europe is more dependent on (though it is growing less so).[x] Whilst a gas price cap is being discussed, talks have been contentious. EU meetings scheduled for 13 December could yield a breakthrough on this front, but energy ministers are reportedly far apart.

Besides leaving Russian gas arrangements untouched, we think the price cap has some other pretty big holes. Russian crude prices—as measured by its Urals blend—are estimated to be around $49 – $53.50 per barrel.[xi] That is quite obviously below the $60 cap, supporting the widespread view amongst political analysts we follow that this measure was only ever intended to be symbolic.[xii] Will January’s review see this differently, i.e., putting the IEA’s baseline closer to actual prices buyers are paying? Can Western parties even pull off unanimous agreement on a lower ceiling?

We think the seeming incoherence of a price cap above Russia’s current discount market prices and the complex mechanism to lower the cap highlights the tension during its negotiation between sapping Russian coffers and ensuring enough supply to meet global oil demand. Whilst the price cap could sink below market levels, squeezing Russia’s oil revenues—and oil flows to the world—the unanimity required suggests this would be a tall order, in our view. For now, it appears to us the policy goal of preserving adequate global oil supplies—and preventing price spikes—has the upper hand.

To that end, for global oil markets, Russian supply continues flowing to big consumers China and India.[xiii] According to recent reports, Russia shipped around 2.7 million barrels per day (bpd) of its oil products in November, just under February’s pre-sanction 2.9 million level.[xiv] As Europe has stepped back, other buyers have stepped in. We don’t see the price cap and embargo changing that. Whilst Western firms dominate trade finance and insurance, throttling Russian oil transport through the developed world, non-Western shipping and maritime services companies have filled the void to direct flows to China and India.[xv] Middle Eastern and Asian firms, for example, are buying up old Greek and Norwegian tankers—at record prices—to take advantage of sky-high charter rates in this trade.[xvi]

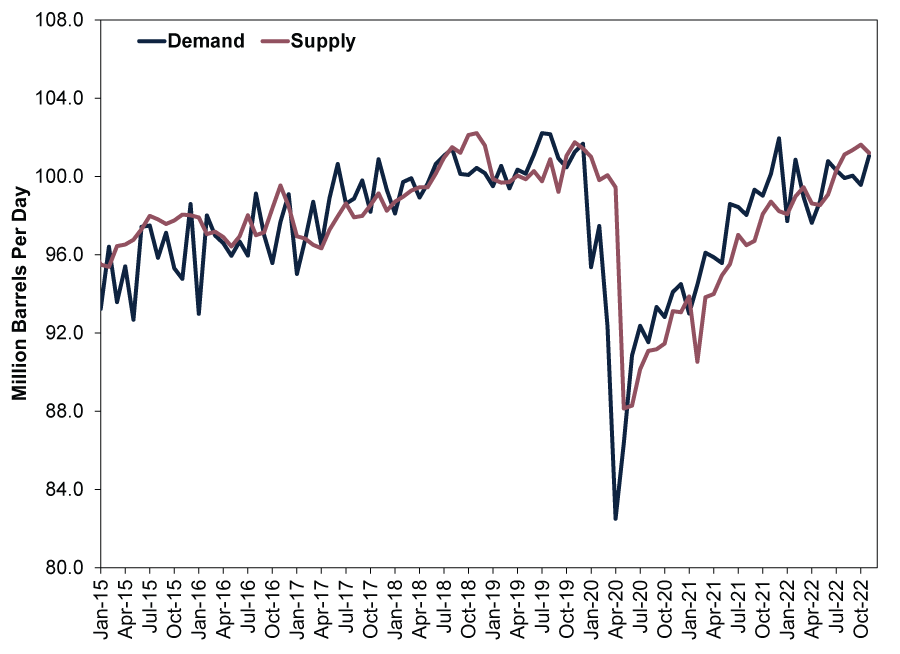

This is what we think matters for oil prices and Energy stocks: global supply and demand. Exhibit 1 shows supply was just above demand in November. Maybe demand exceeds supply in coming months—maybe not. This may depend partly on what OPEC+ (the Organisation of the Petroleum Exporting Countries and its partners, which includes Saudi Arabia and Russia, the world’s second and third largest oil producers, respectively) decides.[xvii] On Sunday, it left its production quotas unchanged, after cutting them by 2 million bpd on 5 October.[xviii] However, OPEC+ wasn’t meeting its daily quotas—by more than 2 million barrels—so the decision just brought it closer to what it was already producing.[xix]

Exhibit 1: Global Oil Supply and Demand in Balance

Source: FactSet, as of 9/12/2022. Monthly global oil supply and demand, January 2015 – November 2022.

Meanwhile, oil prices in US dollars have declined -18.9% since October’s quota cut, bringing the decline since 8 March’s peak to -42.6%, as world-number-one producer America has cranked up output.[xx] In the wake of Russia’s Ukraine invasion, many commentators we follow warned the West’s sanctions might remove Russian oil from markets altogether, but that has proven unfounded—global supply has exceeded demand since July.[xxi] In our view, oil prices ultimately key more off overall production-consumption fundamentals. Marginal moving parts within that—like the price cap and OPEC+ quotas—may affect the bigger picture, and we think they are worth paying attention to. But based on our analysis, if global oil supply and demand stay roughly in balance going forward as we suspect, oil prices probably won’t sway massively in either direction.

From a broader market perspective, we think all the handwringing over the West’s Russian oil price cap shows sentiment continues to underrate reality. Markets are working largely as usual, in our view. Although perhaps disappointing from the perspective of hurting Russia’s revenue, global energy supplies and trading have been more resilient at meeting demand than many commentators we follow deemed likely at the war’s onset. Trade routes for Russian petroleum products have reshuffled, but their new alignments still contribute to total output.[xxii] India’s Russian oil imports have jumped to around a quarter of the total from about 2% pre-invasion.[xxiii] China’s have risen to over a fifth from 16% last year.[xxiv] India and China buying leaves more from non-Russian sources for others. For better or worse, we think that likely helps the world avoid disruption headlines we read warn about.

From our perspective, the global economy—and Europe—face headwinds this winter, and risks from unintended policy consequences remain. But the likelihood of a catastrophic oil supply shock and ever-escalating oil prices seems increasingly remote to us. We think this would be a better-than-expected outcome—bullish for markets.

[i] “Factbox: G7 Price Cap on Russian Oil: What Are the Main Elements,” Staff, Reuters, 4/12/2022. Accessed via the Internet Archive.

[ii] Ibid.

[iii] “Oil Price Wavers After Russia Cap Kicks In,” Joe Wallace, The Wall Street Journal, 5/12/2022. Accessed via Yahoo! “Factbox: Why Are Oil Tankers Stuck in Turkish Waters?” Jonathan Saul, Reuters, 8/12/2022. Accessed via the Internet Archive.

[iv] “China Buys Russian Oil at Multi-Month Low Discounts, Brushes off Price Cap,” Muyu Xu and Chen Aizhu, Reuters, 7/12/2022. Accessed via the Internet Archive.

[v] “US in Talks With Allies on Russian Oil Price Cap, Says Yellen,” David Lawder, Reuters, 20/6/2022. Accessed via the Internet Archive.

[vi] See note iii.

[vii] Ibid.

[viii] “EU Agrees to Set $60 Price Cap Level for Russian Oil Exports,” Ewa Krukowska, Alberto Nardelli and Jorge Valero, Bloomberg, 2/12/2022. Accessed via SupplyChainBrain.

[ix] See note i.

[x] “‘Heated’ and ‘Really Ugly’: Europe Fails to Thrash out Details on Gas Price Cap as Talks Turn Sour,” Silvia Amaro, CNBC, 25/11/2022.

[xi] See note iii.

[xii] “Analysis: G7 Russian Oil Price Cap Evolves From Revenue Squeeze to Market Anchor,” David Lawder and Timothy Gardner, Reuters, 6/12/2022. Accessed via the Internet Archive.

[xiii] See note iv.

[xiv] “Russia Is on Track to Ship Its Highest Amount of Oil Products Since the War as Europe Struggles to Wean Itself off Russian Energy Supplies,” Jennifer Sor, Markets Insider, 29/11/2022. Accessed via MSN.

[xv] “Europe’s New Sanctions on Russian Oil Kick In: What Changes?” Alex Longley, Bloomberg, 2/12/2022. Accessed via Business Standard.

[xvi] “Russian Oil Sanctions Fuel Boom for Old Tankers,” Julia Payne and Jonathan Saul, Reuters, 5/12/2022. Accessed via the Internet Archive.

[xvii] Source: US Energy Information Administration, as of 9/12/2022. Statement based on total oil production by country, August 2022.

[xviii] “OPEC+ Keeps Steady Policy Amid Weakening Economy, Russian Oil Cap,” Alex Lawler, Ahmad Ghaddar and Olesya Astakhova, Reuters, 4/12/2022. Accessed via the Internet Archive.

[xix] “OPEC+ Is Now 3.6 Million BPD Below Its Oil Production Target,” Tsvetana Paraskova, OilPrice.com, 19/9/2022.

[xx] Source: FactSet, as of 9/12/2022. Brent crude oil price per barrel, 5/10/2022 – 8/12/2022 and 8/3/2022 – 8/12/2022. Also see note xvii.

[xxi] Source: FactSet, as of 9/12/2022. Monthly global oil supply and demand, July 2022 – November 2022.

[xxii] See note xxi.

[xxiii] “India Says Russia Oil Deals Advantageous as Yellen Visits Delhi,” Shivam Patel and Krishna N. Das, Reuters, 8/11/2022. Accessed via the Internet Archive.

[xxiv] “China Increases Crude Oil Imports From Russia,” Bojan Lepic, Rigzone, 22/9/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today