Personal Wealth Management / Market Analysis

Steep Selloff Sign of Correction—Not Bear

We believe recent volatility looks like the start of a correction, not a bear market.

UK shares capped their worst week since January 2016 on Friday, with the MSCI UK Index’s -4.6% weekly decline bringing its total drop to -8.8% since its 12 January peak.[i] Global markets also took it on the chin, with US shares officially entering correction territory on Thursday when denominated in USD. Scary stuff, until you remember bull markets usually die with a whimper, not a bang. We believe this looks like a classic bull market correction, and likely not the start of a bear market—and not just because American markets bounced on Friday. The selloff could very well resume on Monday, and short-term volatility is always impossible to predict. But given corrections tend to end as suddenly as they begin, we think the wisest move for long-term growth investors now is to sit tight, lest you sell after a drop and get whipsawed by the recovery.

As a refresher, corrections are sharp, quick, sentiment-driven declines of -10% to -20% or so. They start suddenly and usually end equally quickly, with further gains on the other side. Bear markets, by contrast, are deeper (-20% or worse), longer and have identifiable fundamental causes. Corrections are fleeting and a normal part of any bull market. They help keep sentiment in check, preventing equity markets from overheating and helping extend the bull’s lifespan. They aren’t possible to predict or time repeatedly, so in our view, enduring them is the toll we all pay for bull markets’ stellar longer-term returns. However, we believe it is possible to navigate bear markets and cut out a chunk of the downside if you can spot one early enough.

Big down days like last Monday and Tuesday morning do happen during bear markets, but usually not at the beginning. Bear markets usually roll over gradually, lulling investors into complacency with a gentle decline. The average monthly decline of a bear market is around -2% to -3%, with declines escalating at the end due to negative compounding. Those tame early declines suck people in, throwing more and more money at what they see as buying opportunities—they focus only on price movement, without looking at forward-looking fundamental indicators. They don’t announce themselves with steep early drops—if they did, they wouldn’t lure people back. Yet big down days during bull markets aren’t uncommon, either. For example, when America’s S&P 500 fell -4.1% on Monday, it was the index’s largest drop since mid-2011 but also the 10th daily decline of -3.5% or worse during this bull market.[ii] Not so rare.

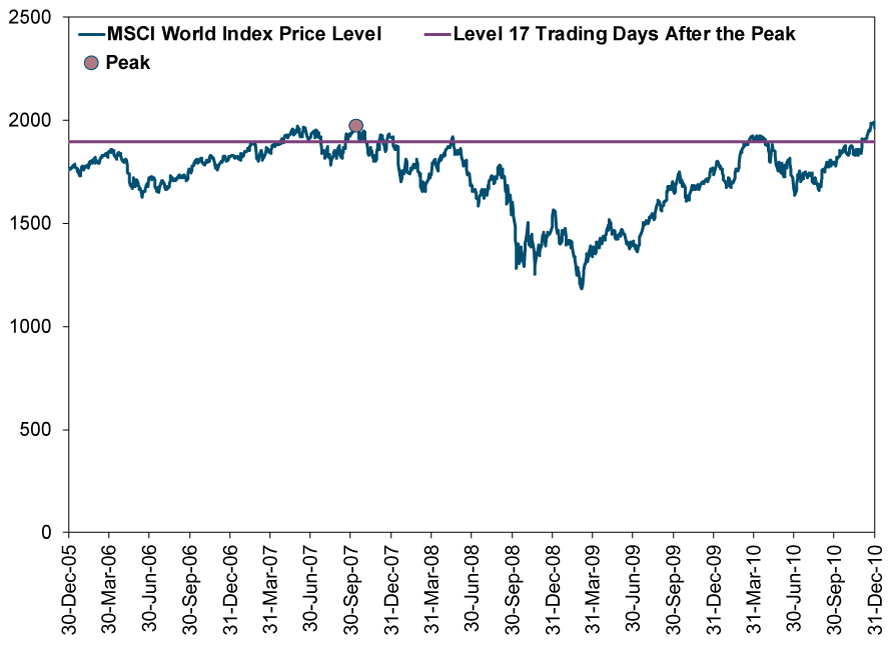

Bear markets generally don’t begin with spike tops. Even when they stumble hard out of the gate, they often pare those losses over the ensuing weeks, affording investors time to assess the fundamental landscape before deciding whether to sell. The 2007 – 2009 bear, which many remember for its violent down days, had a gradual onset. (Exhibit 1) Equity markets rolled over slowly, and the decline didn’t really escalate until the following March, when Bear Stearns imploded. Even then, equities pared some of those losses in the spring before the decline resumed in earnest in summer. The big one-day drops didn’t appear until September 2008.

Exhibit 1: The Global Financial Crisis’s Rolling Top

Source: FactSet, as of 6/2/2018. MSCI World Index price level in GBP, 13/12/2005 – 31/12/2010.

In our view, if you need long-term growth to reach your investment goals, being out of the market is the biggest risk you can take. If you are on the sidelines while equities rise, that can be a hefty setback. So we always urge investors to stay measured and rational, and not bolt at the first sign of trouble. If you sell after a week of bad volatility, and then equities snap back, all you have done is locked in those losses and potentially handicapped your potential recovery.

So we generally encourage folks to follow a simple rule: Never go defensive until at least three months have passed from the most recent peak. That gives you time to monitor fundamental indicators and weigh whether it is a correction—painful, but over quickly—or bear market. Bear markets begin one of two ways: atop the proverbial wall of worry, or with a wallop. Both are fundamental features. Euphoric or complacent investors ignoring some creeping signs of trouble, like an inverted yield curve or falling Leading Economic Index. Or, the wallop: an unseen negative development capable of knocking a few trillion off global GDP, like a world war or destructive piece of regulation. Neither impact is super sudden—this affords you time to do the careful study required to identify a bear unfolding. Corrections, by contrast, are sentiment-driven. They flip fast and without an identifiable cause or driver.

Today, we don’t see evidence of the wall or the wallop. Investors are cheerier now than in years past, but they aren’t out of worries. Even before the selloff began, people feared high valuations, higher budget deficits, inflation, more central bank rate rises and the potential for an overheating economy. At an actual peak, investors would probably spend most of their time searching for reasons shares could still rise despite this, that and the other. As for wallops, we don’t see any presently. American tensions with North Korea remain unlikely to snowball into a full-fledged global war. Most governments in the developed world are gridlocked, reducing the likelihood of legislation with wallop-potential. Central banks globally are moving timidly, reducing the likelihood of a sudden monetary error. Protectionism is a risk, but the Trump administration isn’t doing much the Obama and Bush administrations didn’t do before. Neither US president started a trade war.

Corrections can occur for any or no reason. Sometimes they have a big scary story associated with them. Sometimes they don’t. Senseless freakouts happen. They are unsettling, but they aren’t the end.

So stay cool. If this does turn out to be a bear market, you will likely have more time to make your move. And if it is just a correction, as we believe is likeliest, you will be ready to capture the bounce back.

[i] Source: FactSet, as of 9/2/2018. MSCI UK Index price return, 2/2/2018 – 9/2/2018 and 12/1/2018 – 9/2/2018.

[ii] Ibid. S&P 500 daily price returns in USD, 9/3/2009 – 5/2/2018.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today