Personal Wealth Management / Market Volatility

The Benefits of Keeping an Even Keel in a Fearful Time

Wednesday’s news of new restrictions in Europe and a couple American cities is a development worth noting, but we think extrapolating this to something much larger raises the risk of investing errors.

This terrible year’s twists and turns continued Wednesday, as COVID’s spread continued accelerating in Europe, leading the eurozone’s two largest economies—Germany and France—to install month-long restrictions on select businesses and activities. Politicians also announced new restrictions in a few American cities, most notably Chicago and Newark, which neighbours New York City. Like those in recent weeks, these moves prompted many financial commentators we follow to warn of a renewed lockdown on par with the spring, which we think contributed to global markets’ drop on the day.[i] As hard as it is, we think this is a time when keeping an even keel and not reacting to every headline is critical for long-term investors. In our view, it would take very restrictive measures to wallop this young bull market, given an autumn resurgence was so widely expected.[ii] Our research indicates nothing to date is on par with that. Developments are worth watching, no doubt, but we think it is important for long-term investors to be aware of the risks inherent in extrapolating current headlines into a much more locked-down future.

The day began with Germany and France planning to unveil new measures in response to swift increases in cases and hospitalisations. Early in the evening, German Chancellor Angela Merkel followed through, announcing she had reached agreement with Germany’s 16 states to shutter bars, restaurants, gyms and other leisure establishments from Monday through November’s end. Social gatherings are capped at 10 people from no more than 2 households. Hotels may admit only business travelers. Merkel, who reportedly faces no shortage of criticism for this move, noted that efforts to trace those who come in contact with people who test positive for the virus have failed, and with no way to identify how transmission is occurring and isolate that, she argues more extreme steps became necessary.

Hours later, French President Emmanuel Macron—who previously downplayed the likelihood of nationwide measures—took more extreme action. In a televised address, Macron announced that, effective Monday, bars, restaurants and non-essential retailers will close. Domestic travel and public gatherings are banned, and he encouraged companies to use remote work rather than have workers come into the office. Macron said these measures will last through 1 December, but that he will re-evaluate in two weeks with an eye toward easing restrictions if there is improvement.

Across the Atlantic Ocean, Newark, New Jersey’s Mayor Ras Baraka responded to a spike in infection rates by reinstating restrictions in his city. Every non-essential business is required to close at 8 PM, with outdoor dining permitted until 11 PM (though how well that will work in November in New Jersey’s cold climate is an open question). Hair salons and barbershops will operate by appointment only, with fitness centres remaining open but facing new, heightened sanitation requirements. In Illinois, Governor JB Pritzker announced he will require bars and restaurants in the Chicago suburbs to cease indoor service effective Wednesday, and he limited public gatherings to a maximum of 25 people or 25% of room capacity, whichever is lower. These same measures are slated to begin in Chicago proper on Friday.

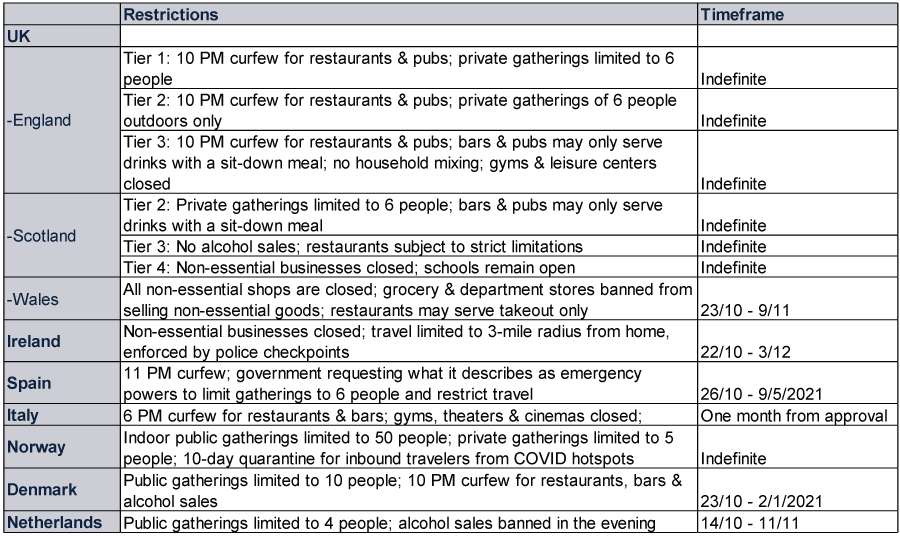

In sum, all this news hitting at once has many financial commentators we follow harkening back to the dark days in mid-March, and warning more and more stringent lockdowns will likely follow. Perhaps they will prove to be correct, but in the meantime, we think it is worth noting the differences between this week’s announcements and the spring’s. In Germany, schools remain open. So do most non-essential retail establishments that aren’t eateries—and hair salons. Merkel’s provisions mostly target places where people congregate, as opposed to being blanket lockdowns. France’s moves are more extreme, hitting many more non-essential businesses. But here, too, schools are unaffected and factories will remain open—a change from earlier this year. Curiously, in our view, France will still allow retirement homes to permit visitors. In the American cities, rules are obviously local and far less extreme than either those in the spring or those abroad now. As for the rest of Europe and the UK, Exhibit 1 rounds up measures announced in recent weeks—all, with the exception of Wales and Ireland, are thus far much less stringent than those in place earlier this year.

Exhibit 1: European and UK Restrictions at a Glance

Source: The Telegraph, BBC News, Welsh government, NPR, French government, Financial Times, Reuters, Bloomberg, France24 and TheLocal.dk, as of 26/10/2020. Note: Spain’s curfew is set to expire nationally on 9 November. The emergency powers the government is seeking would last longer.

In our view, renewed lockdowns that equal or exceed the spring could present a material negative for equity markets in the UK, Europe and globally. But we don’t think that outcome is assured. Based on our research, a COVID autumn wave has understandably been investors’ chief concern since before the first wave ebbed, with pretty much every news outlet we follow publishing hypothetical infection charts showing an even worse second surge. Comparisons with 1918’s flu pandemic, which had two distinct waves, were everywhere. Now, these latest restrictions dot the front pages of news sites from Helsinki to Houston. We may not know what politicians will do from here, but we do have significant experience in studying how markets work, and we have studied vast troves of market history. This leads us to conclude that equity markets reflect all widely discussed information, including mass fears and opinions, and tend to move ahead of widely expected events. This research and analysis informs our opinion that markets likely reflect a great deal of today’s fear already in share prices. We think that likely limits shock power, unless such moves are extreme. If they continue to be less than the full lockdown resumption that seems so widely feared, we think that would actually spell a measure of relief for equities. That doesn’t negate the potential for sharp wobbles like Wednesday’s as events occur, but it does argue against a more lasting, much deeper decline, in our view.

As difficult as it is in this incredibly challenging year, we think keeping an above-the-fray perspective is key for investors seeking long-term market-like returns. It is likely very tempting to extrapolate current measures to something much more restrictive—and damaging. We think doing so is just plain human nature. But we also think it is a behavioural risk that confronts investors worldwide now, carrying the risk of grave error if that extrapolation proves to be incorrect—or if equity markets don’t react to it the way most financial commentators we follow seemsto anticipate. For an investor whose long-term goals require equity-like returns on some or all of their portfolio, we think deviating from equities is perhaps the single biggest risk out there—and that can be avoided by remaining coolheaded.

Again, we aren’t dismissing the risk renewed lockdowns could present. But when confronted with so many unknowns and widespread fear, we think it is important to start with first principles. Today, we think that means remembering how markets generally work and where our research indicates they typically look hardest: at publicly traded corporations’ likely earnings over the next 3 – 30 months. Unless you know something others don’t on that front—or have a strong opinion, based on rock-solid evidence, that mass expectations are too positive—then we suggest thinking long and hard about exiting equities. Bull markets have historically always followed bear markets (prolonged, fundamentally driven equity market declines exceeding -20%).[iii] But being out of equities during a bull market can be a severe setback for those needing stocks’ long-term returns to finance a comfortable retirement, in our view.

[i] Source: FactSet, as of 28/10/2020. Statement based on MSCI World Index return with net dividends, 28/10/2020.

[ii] A bull market is a prolonged period of generally rising equity markets.

[iii] Source: FactSet, as of 29/10/2020. Statement based on MSCI World Index cycles, 31/12/1969 – 28/10/2020.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today