Personal Wealth Management / Economics

What Investors Can Glean From Q4’s GDP Slowdowns

Q4 GDP slowdowns—and even some contractions—surprised few.

One month into 2021 and several major economies have released their government-produced measures of economic output—known as gross domestic product or GDP—for Q4 2020. After huge accelerations in Q3 GDP growth rates, many Q4 readings ranged from slowing growth to an actual return to contraction. Though these data are old news for markets, which we think are forward-looking, the numbers confirm several trends. Perhaps the biggest such trend: The broad reaction to the data is largely rational based on the news coverage we read—a sign of rising optimism, in our view, and worth noting for investors.

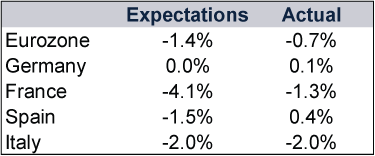

After the US announced Q4 GDP on 28 January—growth slowed from a 33.4% annualised rate to a 4.0% rate (an annualised rate is the rate at which GDP would grow in an entire year if the quarter-over-quarter growth rate repeated all four quarters)—the eurozone followed suit.[i] Prior to the release, many economists’ expectations were low, as targeted lockdowns returned across the Continent in November and December. The results indicate projections were rational, as eurozone GDP contracted, but the numbers also largely beat expectations—signalling some economic resiliency. Germany and Spain even managed meagre Q4 growth.

Exhibit 1: Q4 Eurozone GDP

Source: FactSet, as of 3/2/2021. Q4 GDP quarter-over-quarter percentage change.

These preliminary readings are subject to revision, and subsequent releases will provide more colour as they will include more detailed data. But the headline results, even the contractionary readings, surprised basically none of the financial commentators we reviewed—and surprises sway share prices most, in our view. So we don’t think it was a shock that equities didn’t react negatively.

Among major Emerging Markets (EM), China’s 6.5% year-over-year Q4 GDP growth beat economists’ consensus expectations for 6.0%.[ii] Much of the financial news coverage focused on the country’s full-year growth of 2.3%—the only major economy to expand in 2020.[iii] Whilst that information may be interesting trivia, that distinction doesn’t influence the economic and political factors impacting corporate profits that equities focus on, in our view..

Taiwan was the rare country that didn’t impose a national COVID lockdown, and the numbers show the economic benefits: Q4 GDP rose 4.9% y/y, the fourth straight quarter of year-over-year growth.[iv] The pandemic also stoked global demand for tech and electronics, driving a semiconductor shortage—a boon for both Taiwan and South Korea (Q4 GDP: 1.1% q/q, -1.4% y/y), two integral hubs in the global tech supply chain.[v] In our view, the strong demand for electronic goods illustrates the fundamentals supporting the global Tech sector.

Other EM GDPs—e.g., Mexico (3.1% q/q, -4.6% y/y) and the Philippines (5.6% q/q, -8.3% y/y) mirrored the Q4 resiliency seen in America and the eurozone.[vi] Similar to developed world economies, economists think EM recoveries largely depend on a return to normalcy—a vaccinated world in which households and businesses operate as they did pre-pandemic. We think equities are looking ahead to that world now.

In our view, the past 12 months illustrate how equity markets function as leading economic indicators. After a calm start to 2020, global shares plunged into a bear market (a fundamentally driven equity market decline of -20% or worse) in February – March.[vii] We think equities suddenly shifted focus to the very near term to incorporate the lockdown-driven severe economic contraction. Then we think markets looked out further—to eventual reopenings—as a new global bull market (an extended period of rising equities) began in late March—right as official economic data began confirming contraction.[viii] Today, we think equities are fathoming a time when vaccine distribution is more widespread and economic normalcy gradually returns. We think it would take a new shock to knock equities off this view. The lockdowns that drove slower GDP growth and contraction in Q4 were no such thing, in our view, and increasingly optimistic investors appreciated that.

As for China, we think it previews what growth will look like in a vaccinated world. Economic data improved quickly following the country’s reopening, and official indicators show a state-driven credit boom aided the recovery.[ix] As in the West, data suggest slower growth ahead. Credit growth already seems to have crested, and officials have voiced their intentions to rein shadow lenders (financial institutions whose business occurs outside the traditional state-run banking system) back in. Prior to the pandemic, data from 2018 and 2019 suggest the government’s shadow banking crackdown contributed to slower GDP growth rates.[x] China’s leadership has publicised its comfort with slower economic growth so long as it doesn’t imperil social stability.

Developed world recoveries likely won’t look exactly like China’s since the US, UK and eurozone don’t have economies in which the government intervenes heavily to steer growth. However, we anticipate the general course repeating. We have already seen growth surge on reopenings once, last summer. We think there will likely be another pop, albeit to a much smaller extent, when current restrictions lift. But the pop will likely be fleeting, in our view. Many data points have already returned close to pre-pandemic levels—in some cases, like goods consumption, beyond them. In terms of magnitude and pace, this highlights a key point: We think most of the recovery is already behind us.

Based on our experience, many investors think slower growth is bad for equities. That thinking is overstated, in our view. Today, slower growth would signal some economic normalcy returning—and we think that is a plus. Besides, our research indicates that what matters more to share prices is how sentiment aligns reality than specific GDP growth rates. Based on what we consider to be a largely rational mainstream reaction to the latest GDP numbers, sentiment seems broadly optimistic now—and, with the economy set to return toward normalcy, we think that would be a great backdrop for equities.

[i] Source: FactSet, as of 5/2/2021.

[ii] Source: FactSet, as of 3/2/2021.

[iii] Source: National Bureau of Statistics of China, as of 5/2/2021.

[iv] See note ii.

[v] Ibid.

[vi] Ibid.

[vii] FactSet, as of 5/2/2021. Statement based on MSCI World Index returns with net dividends in GBP, 20/2/2020 – 16/3/2020.

[viii] Ibid. Statement based on MSCI World Index returns on 16/3/2020 and the release of IHS Markit’s March flash purchasing managers’ indexes on 24/3/2020.

[ix] Source: FactSet, as of 5/2/2021. Statement based on Chinese industrial production, retail sales and total social financing.

[x] Source: FactSet, as of 5/2/2021. Statement based on Chinese GDP year-over-year growth rates from Q4 2017 – Q4 2019.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments UK has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

Politics Japan’s Revolving Door Premiership Spins Again2025-09-12

-

Market Analysis To See Long Bond Volatility Clearly, Look Globally2025-09-05

-

In The News Fisher Investments UK Reviews the Limits of Long-Term Forecasts2025-09-02

-

Market Analysis A Market Lesson From Germany’s Economic Data Revision2025-08-26

Contact Us

Learn why 185,000 clients* trust Fisher Investments and its affiliates to manage their money and may be able to help you achieve your financial goals.

*As of 30/06/2025

New to Fisher? Call Us.

Contact Us Today