Personal Wealth Management / Market Analysis

What to Glean From the UK’s May Monthly GDP Release

Stripping away COVID skew, we think plenty of strong areas remain.

A curious thing happened on the way to the UK’s allegedly surefire recession Wednesday: Some of the data that many commentators we follow previously argued confirmed its existence were revised away.[i] Not only did monthly gross domestic product (GDP, a measure of economic output) grow in May, but April’s contraction was milder than initially reported, and March’s slide flipped to a slight gain.[ii] Now, analysing the numbers here probably won’t give you much insight into whether a recession is or isn’t underway, in our view—that much is still rather muddy, as we find it often is when pockets of weakness and relative strength abound. But we think the revised wobbles show why getting bogged down in headline data isn’t too productive for long-term investors. In our view, stocks look forward, not at backward-looking numbers that won’t be final until long after the fact.

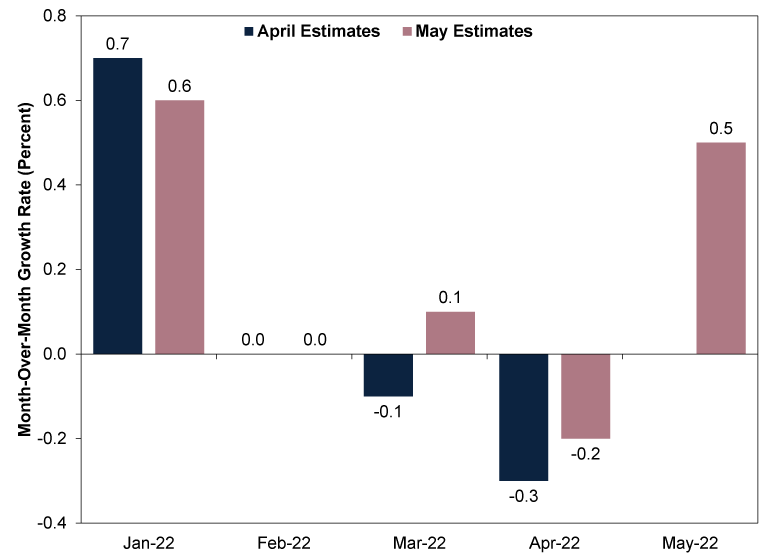

Exhibit 1 shows how this year’s results evolved between April and May’s estimates. Overall, we don’t find the changes terribly significant, but they did shift some analysts’ GDP growth projections pretty radically. Until Wednesday, most commentators we follow had seemingly pencilled in a Q2 decline. Now, with April falling less than expected and May up, some commentators we follow argue that will be enough to offset the impact the extra bank holiday during the Platinum Jubilee will have on June’s data, perhaps making Q2 GDP flat or even slightly positive. Moreover, the data no longer show GDP falling two straight months after a flat February, which had caused financial commentators we follow to extrapolate declines forward.[iii] In our view, a Q2 GDP contraction was always more if than inevitable, and we guess the data now just make that a bit clearer to some (notwithstanding the potential for further revisions, of course).

Exhibit 1: The Ever-Changing UK GDP Data

Source: Office for National Statistics, as of 14/7/2022. Numbers are from the official time series accompanying April and May’s monthly GDP reports.

The main reason we hesitated to read much into monthly GDP is the reason underpinning the revision and May’s rebound: volatility in the Human Health & Social Work Activities component. Initially, the Office for National Statistics (ONS) estimated this fell -5.6% m/m in April due to the end of the National Health Service’s (NHS’s) COVID test-and-trace programme and vaccination drive.[iv] That got revised up to 5.0% in the updated figures, which doesn’t shock us: As the ONS noted at the pandemic’s outset, COVID created some statistical and logistical challenges that led to big revisions, due in part to the way NHS activity is tabulated.[v] That category also was partly responsible for May’s rebound, growing 2.1% as normal GP appointments returned.[vi]

We hesitate to call this category economic activity in the traditional sense of the term. Since the NHS is free at the point of service, there is no market price for activity, which the ONS has stated makes calculating its economic contribution difficult. The monthly measure is an output measure—the quantity produced or served. But quarterly GDP is an expenditure measure. Since there are no market expenditures in the vast majority of the UK’s healthcare sector, the ONS estimates a market value based on cost per unit. In our view, that renders this imaginary economic activity from a pure maths standpoint, and even the ONS warns the set is “challenging” even in normal times, with COVID only adding complexity.[vii]

So when evaluating the economic health of the mighty services sector, we generally look past health (and education, which the ONS warns has similar measurement challenges) and focus on consumer-facing services. There, we think the picture of how April’s cost-of-living jump affected demand is mixed, with supply shortages muddying the waters.[viii] Consumer-facing services growth was revised down to 2.1% m/m in April.[ix] Now, given this is still a strong growth rate, it may be tempting to say this is surefire proof that households overcame the sharp increase to the home energy price cap and a suite of tax hikes, but keep in mind that this followed a drop in March, which stemmed from vehicle shortages.[x] So, in our view, April’s consumer growth at least partly reflected pushed-back demand. That wasn’t the only driver, as personal services also did well, but we think an objective look is important.

In May, consumer-facing services fell -0.1% m/m, with retail, dining and entertainment contributing to the decline.[xi] We think it seems fair to say weaker demand and supply both played roles here, given the many reports of labour shortages and the ongoing dislocations in the global supply chain whilst China remained under lockdown. But we don’t think the picture was entirely bleak. Professional services and transport services rose nicely—and these are output measures, not skewed by inflation (broadly rising prices across an economy). So it may be that continued reopening merely shifted demand from goods to services consumption as people returned to the office.

In our view, one month doesn’t make a trend, so it is impossible to know which explanation holds—we will need more data to discern that. We are merely pointing out the many possible interpretations to underscore why we think making snap judgments on headline data is an error. We think they are too volatile, too subject to revision and too open to interpretation to yield much insight. They are also backward-looking. Here we are, in mid-July, analysing data reflecting a month that ended six weeks ago. Meanwhile, we think stocks are busy looking 3 – 30 months ahead of now. In our experience, about all the data can do is hint at whether investors have been too pessimistic.

There is every chance they have been and that UK stocks have ample positive surprise power ready to boost them. It is also possible a recession is underway, in which case, given the constant drumbeat of recession chatter, stocks probably already reflect a chunk of the weakness—given our research shows stocks deal efficiently with widely expected events. But crucially, we see nothing here indicating a deep, painful contraction is underway—the sort that would likely take a huge bite out of investment and corporate earnings. Rather, we see pockets of good and bad. That may not mean robust economic growth lies ahead, but it likely also means negative surprise power should be limited from here.

[i] Source: ONS, as of 13/7/2022. Statement based on GDP monthly estimate, UK: May 2022. A recession is a period of contracting economic output.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid

[v] Ibid.

[vi] Ibid.

[vii] “Coronavirus and the Effects on UK GDP,” UK Office for National Statistics, 6/5/2020.

[viii] Source: ONS, as of 13/7/2022. Statement based on GDP monthly estimate, UK: May 2022.

[ix] Ibid.

[x] Ibid. Statement based on GDP monthly estimate, UK: March 2022.

[xi] Ibid. Statement based on GDP monthly estimate, UK: May 2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics This Week in Gridlock: Europe Edition2026-03-27

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-18

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-18

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today