Personal Wealth Management / Market Analysis

Why Savings Aren’t Necessarily Economic Rocket Fuel

Don’t presume massive household savings will lead to surging spending.

As vaccine distribution becomes more widespread, many economists we follow are becoming increasingly optimistic about economic growth. One factor underlying the excitement: Households are sitting on a massive pile of savings, with the Office for National Statistics’ latest data showing £60 billion in new savings in Q4 alone.[i] We have seen many financial commentators argue UK consumers have between £120 billion and £170 billion in savings just waiting to be spent. Some claim this is fuel that will power an economic recovery for a long time to come.[ii] But in our view, households are unlikely to spend all these savings, and we think sentiment toward this alleged mountain of pent-up demand is a key place to watch for expectations getting irrationally high.

Bank of England Chief Economist Andy Haldane is perhaps the most high-profile individual we have seen making this argument, stating recently that consumers’ spending savings should power a “rip-roaring recovery.”[iii] Several other analysts have a similar viewpoint. Yet in our view, presuming households will spend all their savings and fuel a long boom when businesses reopen from the latest lockdown seems premature to us. Yes, removing COVID restrictions will likely release some pent-up demand, as economic data from last summer indicated.[iv] A similar phenomenon probably occurs again, though perhaps to a lesser degree since retail sales declined less this winter than during the first lockdown. That suggests less demand is pent up than before.[v] It also seems fair to presume travel and leisure spending will likely get a boost as people take delayed vacations. But that is a far cry from drawing down the entire pool of amassed savings. There is no rule higher savings automatically predicts higher spending, as households could also pay down debt or keep a larger emergency cash stockpile.

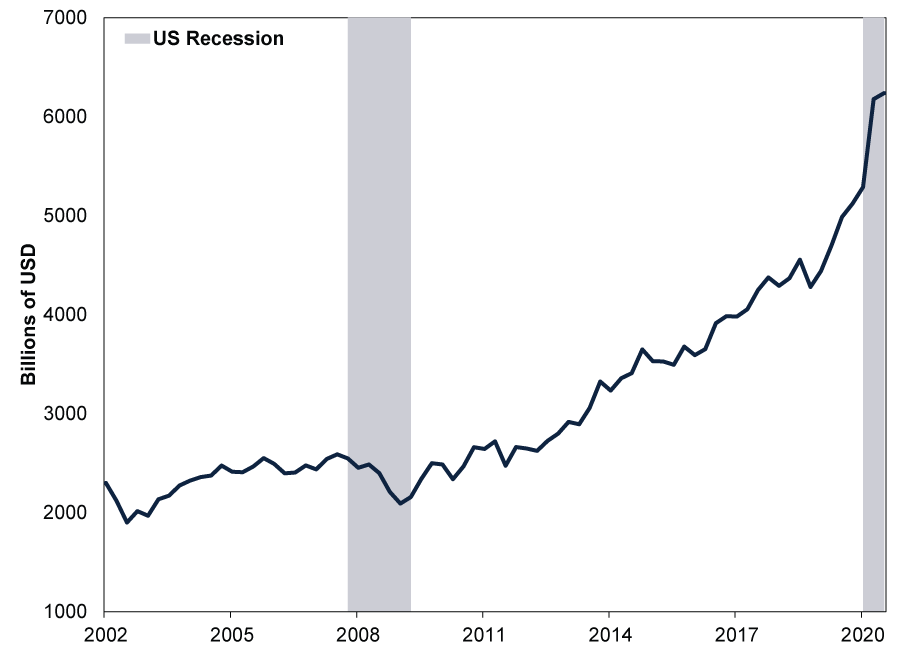

That latter decision wouldn’t be unprecedented. American companies did something similar following the 2008 – 2009 financial crisis, as Exhibit 1’s look at US corporate balance sheets shows.

Exhibit 1: US Nonfinancial Corporate Business Cash Levels Since 2002

Source: FactSet, as of 5/3/2021. Nonfinancial corporate business; liquid assets (broad measure), quarterly, in billions of US dollars. Q1 2002 – Q3 2020. Recession dating is from America’s National Bureau of Economic Research.

For years before the crisis, as the chart shows, corporate cash on hand held fairly steady between $2.0 and $2.5 trillion. The crisis forced companies to draw down a chunk of that, but they quickly rebuilt it—and then kept on saving. That seems to us like a logical reaction, considering the financial crisis showed what happens when money markets are under stress and overall solvent companies lack liquidity and can’t get financing in a pinch. The list of non-bank corporate casualties from that era is long, and our research shows even many survivors had to make deep cuts.

We think Corporate America saw the importance of a sufficient cash cushion to weather tough times and acted accordingly. Anyone who might have seen that cash as pent-up investment and economic rocket fuel likely would have been sorely disappointed. We wouldn’t be shocked if consumers behaved similarly even in a vaccinated, post-COVID world. We have all just seen how quickly emergency government policies can strip people of their livelihoods.

From an investing perspective, we think cheery chatter about a potential household spending surge highlights today’s widespread optimism. But we also think equity markets are forward-looking and have therefore likely already accounted for much of this widely discussed post-COVID spending. We encourage long-term investors to keep this in mind if spending estimates continue climbing in the months ahead. It may signal investors’ expectations are getting ahead of reality—a potential sign of euphoria taking hold.

[i] Source: Office for National Statistics, as of 31/3/2021.

[ii] “UK Economy Bouncing Back Stronger Than Expected Amid Savings Boom,” Phillip Inman, The Guardian, 31/3/2021.

[iii] “Economy Will Bounce Back as People Spend Again – BoE’s Haldane,” Staff, Reuters, 24/3/2021.

[iv] See Note i.

[v] Ibid.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today