Personal Wealth Management / Market Analysis

Why Terrorism Doesn’t Terrorise Markets

Our research shows markets are a lot more resilient than many commentators give them credit for.

Amidst all the gut-wrenching images and stories emerging from Afghanistan, equity markets globally have largely held steady—in our view, a testament to markets’ seemingly coldhearted ability to see through local tragedies and continue pricing in the world’s economic future.[i] Encouragingly, we haven’t seen commentators argue the country’s destabilisation and Taliban control of American weapons and war materiel are directly negative for markets. But we have seen several claim there is an indirect impact that looms over the future, courtesy of the heightened risk of terror attacks in the West now that some geopolitical researchers we follow presume the Islamic State and Al Qaeda have safe quarter. They point to the US equity market’s severe reaction to the 9/11 World Trade Center attacks and warn of repeats. To be clear, the societal risk of terrorism is real and omnipresent, and attacks can destroy lives and property on an unfathomable scale. But for equities, we think the calculus is different, and as we will show, the past 20 years have demonstrated terrorism doesn’t cause lasting declines.

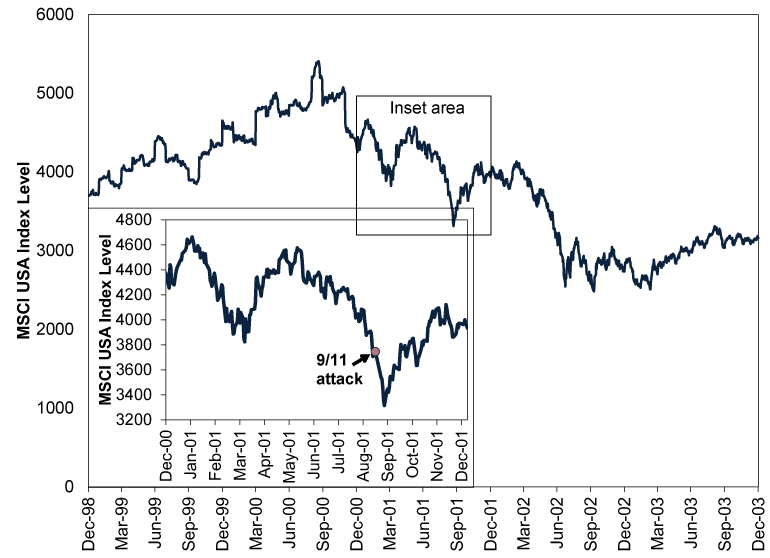

Perhaps counterintuitively, we think 9/11 both demonstrates this and explains why it is so. As Exhibit 1 shows, the MSCI USA Index plunged -11.5% between market close on 10 September and 21 September, the post-attack low.[ii] An attack of that scale on the World Trade Center and Pentagon was unprecedented and unexpected, a shocking tragedy that cut America deeply. This plus the associated uncertainty understandably is what sent markets reeling, in our view. But then the rout stopped, and in retrospect, we think it is easy to see why. People in lower Manhattan went back to work. Society pulled together and got on with it. It soon became clear that the economic effects weren’t huge—utterly disproportionate with the impact on thousands of families and the national psyche. Business continued. Markets callously accepted the reality that terrorism was part of our lives, and moved on. Just 19 trading days after 9/11, markets regained 10 September levels.[iii] The MSCI USA Index finished the year higher than its pre-attack level. The bear market that had begun back in September 2000 would last until October 2002 as investors continued dealing with the dot-com bubble’s implosion and other related issues our research has pointed to, but 9/11’s negativity was a small pocket. (A bear market is a broad, lasting equity market decline of -20% or worse with an identifiable fundamental cause.)

Exhibit 1: US Equity Markets and 9/11

Source: FactSet, as of 25/8/2021. MSCI USA Index with net dividends in GBP, 31/12/1998 – 31/12/2003.

Before 9/11, a potential large-scale terror attack on home soil wasn’t front-of-mind for most Americans. Yes, many of a certain age had seen the 1993 World Trade Center bombing, so-called lone wolf attacks like the Oklahoma City bombing, and violence from domestic terror groups like the Weather Underground. Al Qaeda’s attack on the USS Cole was also rather fresh in the national memory, alongside the US embassy bombings in Africa. But all had seemingly conditioned Americans to view terror attacks as small and isolated. As society watched the collapsing towers, smashed Pentagon and smoldering wreckage of Flight 93 that bright September morning, the frame of reference and expectations changed instantaneously.

Hence, on 9/11, terror attacks—even huge ones—lost their surprise power over society and equity markets. Even as America was spared from major incident, attacks in Madrid, London, France and elsewhere in Europe reiterated the constant threat. Every airport security check reminds us of it. If anything, we think the seismic shift in Afghanistan likely prevents Western societies (and investors) from getting complacent, keeping the surprise factor at bay.

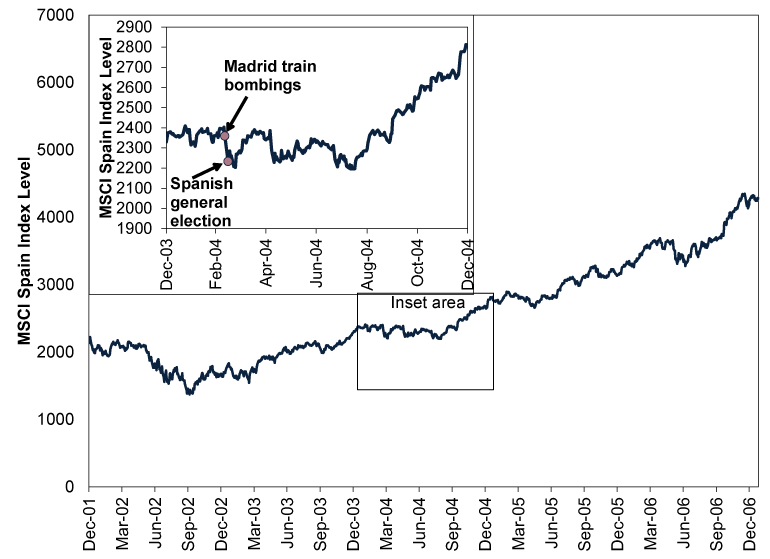

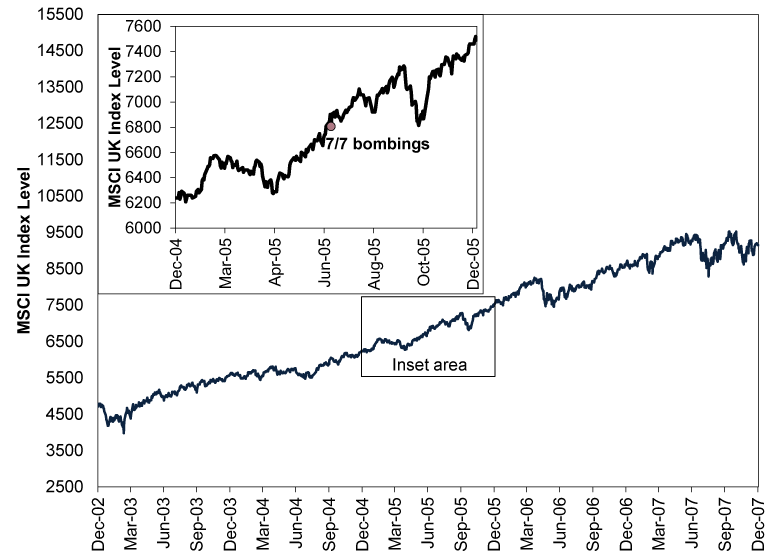

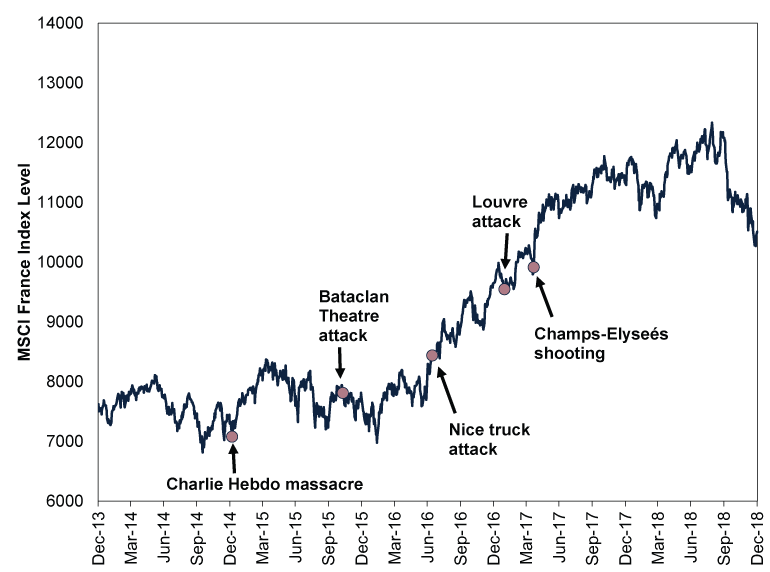

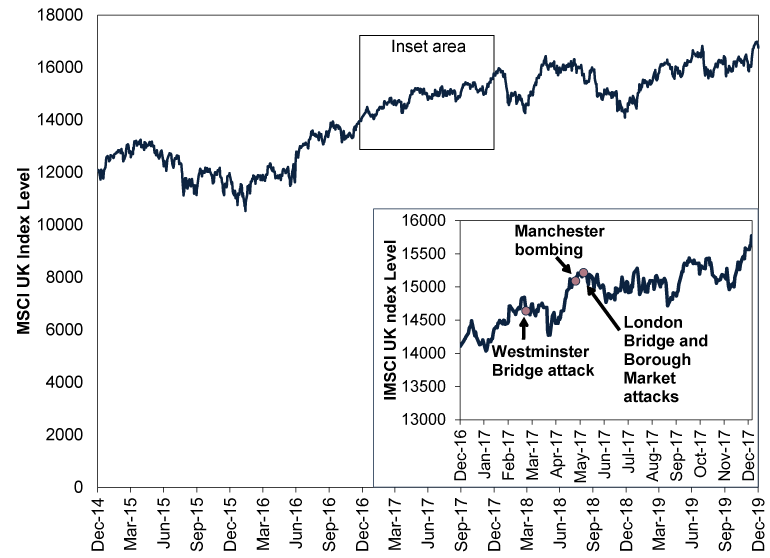

As terror attacks big and small continued, their market impact grew small and increasingly difficult to isolate from other variables. As Exhibit 1 shows, whilst Spanish shares tumbled the week of the Madrid train bombings in 2004, this incident happened on the home stretch of a contentious Spanish general election campaign—often a time of heightened uncertainty for shares, according to our research. The following year, UK shares’ apparent reactions to the 7/7 London bombings lasted all of one day. (Exhibit 3) A decade later, a stream of attacks in France (Exhibit 4) arrived during a global equity market correction that, according to our research stemmed from investors’ overreaction to currency reforms in China, not terror. (A correction is a sharp, sentiment-fuelled drop of -10% to -20%). In 2017, a tragic run of attacks in London and Manchester largely blended in with UK shares’ day-to-day volatility. (Exhibit 5)

Exhibit 2: Spanish Equity Markets and the Madrid Train Bombings

Source: FactSet, as of 25/8/2021. MSCI Spain Index with net dividends in GBP, 31/12/2001 – 31/12/2006.

Exhibit 3: UK Equity Markets and the 7/7 Bombings

Source: FactSet, as of 25/8/2021. MSCI UK Index total return in GBP, 31/12/2002 – 31/12/2007.

Exhibit 4: French Equity Markets and the Mid-2010s Attacks

Source: FactSet, as of 25/8/2021. MSCI France Index with net dividends in GBP, 31/12/2013 -31/12/2018.

Exhibit 5: UK Equity Markets and the 2017 Attacks

Source: FactSet, as of 25/8/2021. MSCI UK Index total return in GBP, 31/12/2014 – 31/12/2019.

In our view, this is all a striking testament to the power and resilience of free societies. Like the people whose transactions they register, markets are defiant. They stand because we stand, even despite threats and, sometimes, very real tragedies. We hope and pray that attacks won’t happen. We don’t really know if they are any more likely now than a month, year or three years ago. But we think it is quite likely that if terrorist strikes come, society and markets shall overcome, as they have before.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today