Personal Wealth Management / Market Analysis

A Counterpoint to Dour Economic Forecasts

Rising bank lending is one factor arguing against a global recession, in our view.

Forecasts of recession—broad, economy-wide weakness—have dominated financial headlines we have seen this year. That is understandable, in our view, given the global economy’s soft patches and risks (e.g., Europe’s energy situation). Moreover, today’s economic headwinds, from elevated inflation (rising prices economy-wide) to possible energy rationing, may heighten the prospect of recession in certain regions.[i] That said, projections of a severe global downturn seem overstated, in our view. Based on our research, fundamental drivers—key amongst them bank lending—suggest reality isn’t as poor as many outlooks we have seen anticipate and underpin the recovery we think is coming.

Our review of headlines has found many prominent outlets and voices say things are going to get worse before they get better. A recent Wall Street Journal survey found a majority of polled economists think America will enter recession in the next 12 months.[ii] World Bank President David Malpass warned of a “real danger” of a worldwide contraction next year.[iii] The International Energy Agency lowered its global oil demand growth forecast because major institutions downgraded their latest global GDP estimates.[iv]

But the kicker: The IMF’s latest “World Economic Outlook” (WEO) cranked recession warnings into overdrive, according to our review of coverage. Interestingly (and unsurprisingly to us), most coverage we reviewed focussed on one line in the WEO’s foreword: “In short, the worst is yet to come, and for many people 2023 will feel like a recession.”[v] (Boldface ours) We don’t dismiss people’s emotions or hardships, but feelings don’t predict people’s economic behavior, based on our market research. Looking a bit deeper at the report, the IMF isn’t even forecasting a global GDP contraction next year—it is predicting annual growth of 2.7%, 0.2 percentage point below its July WEO estimate.[vi] Yes, that is slower growth—but it is still growth.

Now, to be clear: Though we don’t think forecasts are assured to prove prescient, they don’t seem completely off base, either. For example, amongst major economies, the IMF forecasts annual GDP contractions in Germany, Italy and Russia next year.[vii] In the IMF’s view, the Continent’s high energy prices will likely knock the first two due to their reliance on natural gas—and for Germany in particular, due to its dependency on Russian energy.[viii] Russia’s projected contraction is tied to economic sanctions due to its despicable invasion of Ukraine.[ix] We wouldn’t be surprised if those estimates held up, as our economic analysis has found evidence of soft patches in Europe and other parts of the global economy, and German industry is uniquely dependent on petrochemicals, which feed its chemicals industry and others.[x] However, whilst a shallow recession is possible, eurozone stocks’ behaviour this year implies they have been digesting these weaker economic prospects for some time.[xi] This is how forward-looking markets work, in our view: Rather than wait for official data to confirm contracting GDP, they pre-price probabilities and move on.

In our view, economic forecasts have value for investors, but not because they are crystal balls. Rather, we think they provide a useful snapshot of sentiment. In our experience, forecasts reveal supranational organisations’ views, which can influence others’ opinions, including other research outfits, policymakers, commentators and investors. The reaction to popular, widely followed forecasts can reveal insight about people’s feelings. This combination helps set the market’s baseline expectations—critical information, in our view, for investors as they assess how outlooks square with reality.

On that reality front, economic fundamentals currently argue against a deep, severe recession, in our view—and firm loan growth in major developed economies is one telling piece of evidence. Consider the lending environment in the US, which we think is worth monitoring since the country accounts for about 70% of developed-world stock market value.[xii] America’s biggest banks recently reported Q3 earnings, and we have seen myriad analysts scour the numbers to paint a picture about the US economy. Similar to the chorus of concerns tied to recent global economic forecasts, we found headlines focussed on weak areas (cooling mortgage lending due to rising rates) or dour outlooks (e.g., some bank executives’ stated recession concerns).[xiii]

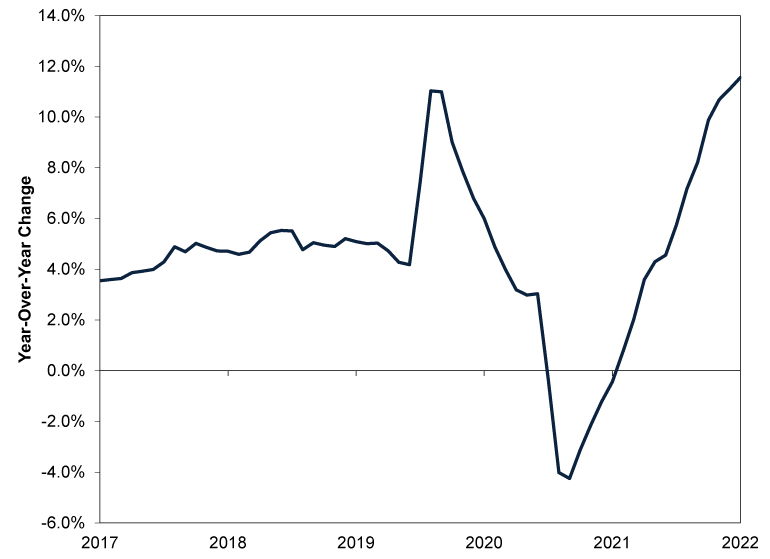

But in our view, this negative emphasis overshadowed some positive news in banks’ primary business: lending. America’s big banks reported brisk Q3 loan growth, which brought in more interest income.[xiv] This doesn’t appear to be a blip, either, as US lending has picked up over the past 12 months. (Exhibit 1)

Exhibit 1: US Lending Has Been Picking Up

Source: St. Louis Federal Reserve, as of 18/10/2022. Loans and leases in bank credit for all commercial banks, in billions of USD, seasonally adjusted, monthly, September 2015 – September 2022.

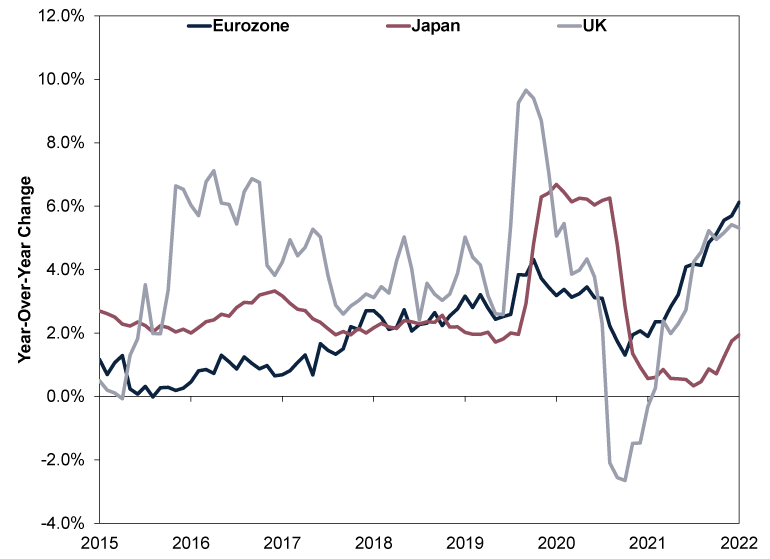

Loan growth has also picked up in other major developed nations, albeit at slower rates. (Exhibit 2)

Exhibit 2: Loan Growth Is Up in the UK, Eurozone and Japan, Too

Source: European Central Bank, Bank of Japan and Bank of England, as of 11/10/2022. August 2015 – August 2022.

Based on our research, loan growth implies money is flowing to businesses, which can underpin investment in growth-orientated endeavours. Going back to America, US nonresidential private investment (i.e., business investment) suggests this has been happening, as the measure rose 7.9% annualised in Q1, 0.1% in Q2 and 3.7% in Q3.[xv] Note: These numbers are adjusted for inflation, so although investment appears to have slowed since Q1 due to elevated prices, it hasn’t cratered, either—a sign of business spending’s resiliency, in our view. Moreover, we don’t think headline business investment figure tells the whole story. On a category basis, structures investment (down -15.3% annualised in Q3 after Q2’s -12.7%) has detracted the most this year.[xvi] However, equipment spending (10.8% annualised) and intellectual property products spending (6.9%) both rose in Q3—and whilst the former has been mixed, the latter has remained steadily positive thus far in 2022.[xvii] If a deep recession loomed, we would likely see investment plunge broadly, and we don’t see that in these data.

Based on our review of other fundamentals, lending isn’t the only positive. Others include easing supply chain pressures and gridlocked politics in many developed nations, the latter of which discourages major legislative change that can stir uncertainty, which our research shows stocks dislike. Whilst pessimism dominates now globally, low expectations mean reality has a low bar to clear. For investors we think it is worth remembering that stocks don’t need perfection to rise—better-than-expected can often be the grounds for a recovery.

[i] Source: FactSet, as of 26/10/2022, and “Energy Crisis: Can the EU Tame Soaring Prices?” Nik Martin, Deutsche Welle, 30/8/2022. Statement regarding inflation based on UK consumer prices and the eurozone’s harmonised consumer prices.

[ii] “Odds of Recession in Next 12 Months Now 63 Percent in Survey of Economists,” Zach Schonfeld, The Hill, 16/10/2022.

[iii] “World Bank’s Malpass, IMF’s Georgieva See Rising Risks of Global Recession,” Andrea Shalal and David Lawder, International Business Times, 10/10/2022.

[iv] “OPEC Could Tip the World Economy Into Recession, Warns IEA,” Hanna Ziady, CNN Business, 13/10/2022.

[v] “Countering the Cost-of-Living Crisis,” IMF, October 2022.

[vi] Ibid.

[vii] Ibid.

[viii] Ibid.

[ix] Ibid.

[x] “German Chemical Industry Has No Gas Left to Cut, Warns Association,” Patricia Weiss and Miranda Murray, Reuters, 19/7/2022. Accessed via Yahoo! Finance.

[xi] Source: FactSet, as of 24/10/2022. Statement based on MSCI EMU Index returns with net dividends, in GBP, 31/12/2021 – 21/10/2022.

[xii] Ibid. Statement based on America’s composition within the MSCI World, as of 25/10/2022.

[xiii] “Recession Threat Looms Large Over US Bank Earnings,” Max Reyes and Katherine Doherty, Bloomberg, 12/10/2022. Accessed via Yahoo! Finance.

[xiv] Source: Fisher Investments research, as of 17/10/2022. Statement based on review of company filings of JPMorgan, Bank of America, Wells Fargo, Citigroup and US Bank. MarketMinder Europe doesn’t make individual security recommendations, and the companies we highlight here are part of a broader theme we wish to highlight.

[xv] Source: FactSet, as of 28/10/2022. The annualised growth rate is the rate at which business investment would grow if the quarter-on-quarter growth rate repeated for four consecutive quarters.

[xvi] Ibid.

[xvii] Ibid.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today