Personal Wealth Management / Behavioral Finance

A Quick Reminder: Feelings Don’t Foretell

Plunging sentiment gauges don’t mean the economy or markets will follow.

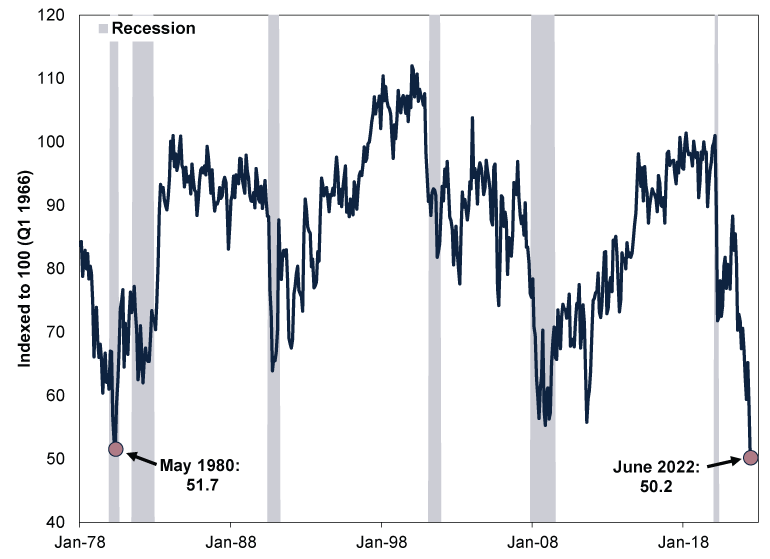

In America, the University of Michigan’s (U-Michigan) widely watched US consumer sentiment index fell to 50.2 this month—a record low, if the final reading confirms the preliminary estimate on 24 June.[i] This confidence measure matches other recent dour polls highlighted in financial headlines we monitor: See Bank of America’s June fund manager survey (73% of respondents anticipate a weaker US economy over the next 12 months) or GfK’s May UK Consumer Confidence Barometer, which hit a record low in May.[ii] In our view, the U-Michigan index’s record figure is an opportunity to revisit an important lesson for investors globally: Sentiment gauges, at best, reflect respondents’ feelings at the present moment. However, moods don’t foretell economic activity, and we think it is often wiser to view them as a sign of what markets already incorporated into share prices than what is to come.

All components of the U-Michigan index fell in June, from the outlook on business conditions over the next year (-24% m/m) to consumers’ assessment of their personal financial situations (-20% m/m).[iii] Amongst consumers, 46% attributed their negative views to inflation (broadly rising prices across the economy)—the second-highest share since 1981.[iv] Half of respondents “spontaneously” mentioned rising petrol prices in survey interviews, up from 30% in May and just 13% in June 2021, with consumers projecting petrol prices to rise by a median of 25 cents over the next 12 months.[v] From a historical perspective, the U-Michigan’s sentiment measure undercut its prior record low of 51.7 in May 1980, amidst that year’s recession (a prolonged and widespread economic contraction).

Exhibit 1: Feelings at a New Low?

Source: FactSet, as of 13/6/2022. University of Michigan Consumer Sentiment Index, monthly, January 1978 – June 2022 (preliminary). Recession shading based on National Bureau of Economic Research’s (NBER) monthly business cycle dating. NBER is America’s official arbiter of recessions.

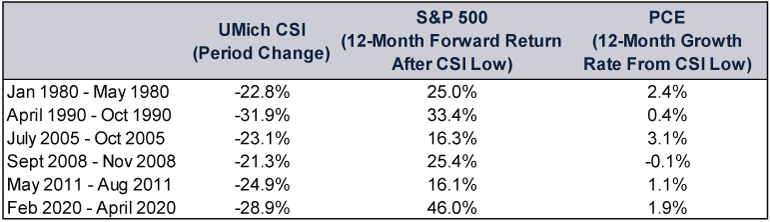

But based on our research, past steep drops in consumer confidence said little about what stocks and consumer spending did afterwards. Consider: From April – June, the U-Michigan consumer sentiment index fell -23.0%.[vi] Using -20% as a threshold, we found six similar sharp index declines over short timeframes since 1978 (when monthly data begin), depicted in Exhibit 2.[vii] Some stretches came amidst broader bear markets (typically extended, fundamentally driven market downturns of -20% or more), including 2008. Other periods didn’t (2005 and 2011). Yet nearly all of them show prior market and economic conditions—or fears of them (e.g., Hurricane Katrina’s landfall in 2005, which devastated New Orleans and America’s Gulf Coast and led some economists we follow to argue US economic growth would suffer)—afflicted confidence.[viii] Yet that didn’t foretell poor market returns in the next 12 months, and only one (2008) coincided with falling consumption.

Exhibit 2: Plunging Sentiment Didn’t Hurt Consumer Spending or Stocks

Source: FactSet and Global Financial Data, Inc., as of 14/6/2022. University of Michigan Consumer Sentiment Index, monthly, January 1978 – June 2022 (preliminary), S&P 500 Total Return Index, monthly, January 1978 – April 2021, and real personal consumption expenditures, in billions of chained 2009 dollars, January 1978 – April 2022. S&P 500 returns presented in US dollars. Currency fluctuations between the pound and dollar may result in higher or lower investment returns.

On the flipside, soaring confidence hasn’t meant automatic rising market returns, either. The U-Michigan survey’s all-time high was January 2000—just a few months before the dot-com bubble popped and US stocks’ bear market began.[ix] Based on our observations at the time, broad-based euphoria had taken hold, blinding investors from deteriorating fundamentals. In our view, how people feel today just doesn’t tell you where markets and the economy will head tomorrow.

Rather, we think gauges like U-Michigan’s highlight mostly what investors were experiencing, fearing and therefore pricing into stocks already. We understand times today are difficult for many households and businesses globally, and the latest sentiment surveys provide a snapshot of real hardships. Those challenges may persist for a while, which is frustrating. But in our view, sentiment measures can provide a sense of where expectations are relative to reality. Today, our coverage of widely watched surveys of consumers and experts alike paint a similar picture: Few seem optimistic about economic growth, with forecasts of economic troubles or recession increasingly common.

We don’t dismiss the myriad perceived negatives taking turns at weighing on stocks today, but given how widespread the dour discussion is, we think efficient markets have likely pre-priced those issues already, sapping surprise power. In our view, these low expectations set the stage for upside surprise, as even weak-but-positive numbers could provide relief—especially with so many foreseeing the worst. We think finding disconnects between expectations and reality could indicate where markets—which often do what the crowd doesn’t expect—are headed next.

[i] Source: FactSet, as of 10/6/2022.

[ii] “Stagflation Fears Surge and ‘Sentiment Is Dire’ in BofA Survey,” Ksenia Galouchko, Bloomberg, 14/6/2022, accessed via Yahoo!Finance, and “Consumer Confidence Down Two Points to Lowest-Ever Score of -40,” Staff, GfK, 20/5/2022.

[iii] “Preliminary Results for June 22,” Surveys of Consumers – University of Michigan, 10/6/2022.

[iv] Ibid.

[v] Ibid.

[vi] See note i.

[vii] Note: According to our research, monthly data readings can be volatile, so we selected periods featuring consecutive monthly declines only. Our intent is to highlight stretches in the University of Michigan Consumer Sentiment Index that resembled the recent decline.

[viii] “Katrina’s Shock to the System,” Jad Mouawad, The New York Times, 4/9/2005. Accessed via the Internet Archive.

[ix] Source: FactSet, as of 17/6/2022. S&P 500 Total Return Index, in USD, 24/3/2000 – 9/10/2002. Currency fluctuations between the pound and dollar may result in higher or lower investment returns.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today