Personal Wealth Management / Politics

An Investor’s Guide to September’s Developed Market Elections

A preview of upcoming election developments in Germany, Canada, Norway and Japan.

Editors’ note: Our election commentary is intentionally nonpartisan. We don’t favour any party or politician as we think political bias blinds and leads to investing mistakes. Thus, we analyse political developments only for their potential market impact.

After a relatively quiet year election-wise in developed markets, political activity will pick up next month. Postal voting has already begun for Germany’s 26 September federal election. Over the weekend, Canadian Prime Minister Justin Trudeau called for a snap election on 20 September. Norway goes to the polls 13 September to elect a new Parliament. Meanwhile, the spectre of a snap election looms over Japan. In our view, the outlook for political gridlock is likely markets’ main consideration: How active (or inactive) will governments be following election results? According to our research, inactive governments decrease markets’ legislative risk aversion, as there is less likelihood of new laws creating winners and losers. More active governments, by contrast, generally raise uncertainty, which our research indicates can dampen equity returns.

Whilst the outcomes remain unclear, here is what we think investors should look out for during a busy month of elections.

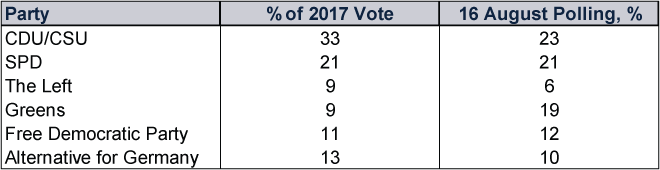

German federal election: The future makeup—and leader—of Germany’s Bundestag is unknown, but some form of coalition government seems likely to us, extending gridlock. Neither party in the current ruling coalition—nor any waiting in the wings—looks able to secure an outright majority, in our view. Exhibit 1 shows three parties—the Christian Democratic Union (CDU, along with its Bavarian sister party, the Christian Social Union or CSU), the Social Democrats (SPD) and the Green Party—running virtually neck and neck at around 20% in the polls.

Exhibit 1: 2017 German Election Results and 2021 Polling, Major Parties

Source: Federal Returning Officer of Germany and Forsa, as of 18/8/2021.

The existing grand coalition between long-serving Chancellor Angela Merkel’s CDU and the SPD hasn’t passed much of substance beyond COVID relief. Finance Minister Olaf Scholz, who is the SPD’s candidate for chancellor, received a popularity boost from heading that relief effort, which could be starting to translate into broader SPD support. The latest polling has the SPD overtaking the Greens but still a couple points behind the CDU/CSU.[i] Polling isn’t predictive, in our view, but the movement strikes us as noteworthy.

Regardless, the next government could take multiple forms. Another CDU-led government is possible, perhaps with the SPD again, but so is a coalition without it. One combo eyed by many commentators we follow is a potential CDU-Green coalition. Whilst that could happen, it may fall short of a majority, opening the door for a three-way agreement, perhaps with Christian Lindner’s pro-business Free Democrats (FDP). Some also point to the possibility of a coalition including the Greens, SPD and FDP, although this grouping would appear to be less aligned ideologically. In our view, all of these potential combinations would likely have a difficult time enacting major legislation, given the parties’ deep ideological divisions.

Much of the market-related election commentary we have seen focuses on what the election means for government spending, as the main parties disagree on the future of Germany’s so-called debt brake, which is a constitutional rule that limits federal structural deficits to 0.35% of GDP—and zero for its sixteen states. (Structural deficits refer to the budget deficits that would exist regardless of economic fluctuations and their temporary impact on public spending and government revenues.) The current coalition suspended the debt brake temporarily under pandemic lockdowns. The CDU advocates its quick restoration, whilst the Greens have proposed sweeping changes to enable higher public spending. In our view, the debate is academic for markets. Additional fiscal assistance may help those in need, but for the overall German economy, we think simply reopening should suffice to restore normal growth patterns.

Whilst coalition gridlock looks likely to us, election results themselves should further resolve lingering political uncertainty, which our research shows can be a market tailwind. One thing seems clear though, in our view: No one with Merkel’s stature—and political capital—appears likely to replace her.

Canadian federal election: From our standpoint, and many political commentators’ we follow, Trudeau’s snap election seeks to capitalise on Canada’s successful vaccination push and win an outright majority for his Liberal Party, which currently has a minority government. This has fostered gridlock since 2019’s election, as Trudeau depends on support from an array of smaller parties to pass legislation. That has stalled most endeavours outside of COVID relief. In our view, this has been a positive for Canadian markets, and losing gridlock could be a modest headwind.

It is an open question whether his Liberal Party can secure a majority—and whether he will resign if it doesn’t. Although Trudeau and his party have strong poll numbers—better than the main opposition Conservatives—Canadians vote by district, or ridings, which national polling doesn’t always reflect very accurately.[ii] Smaller parties like the New Democrats and regional parties—namely the Bloc Québécois—at the district level can spoil larger parties’ national aspirations. Provincial elections in Nova Scotia this week also show pre-campaign polls’ lack of predictive power, in our view. Polls heading into the election put the province’s Progressive Conservative party (the provincial version of the national Conservative Party) 28 points behind, leading many to write off its chances.[iii] But when the results came in, the Tories took 31 of 55 provincial seats in a stunning come-from-behind victory.

If the Liberals succeed in regaining their national majority, it could raise political uncertainty—and legislative risk. But the outcome isn’t knowable now, which in our view makes this an issue to watch but not a reason for portfolio moves today.

Norwegian parliamentary election: In Norway, commentators we follow suggest a left-leaning coalition could defeat Prime Minister Erna Solberg’s Conservative-led coalition.[iv] Like in Germany though, whatever the government’s flavour, no single party seems set to get close to a majority in Norway’s legislature, known as the Storting. Currently, the centre-right coalition, which includes three parties, holds only a minority of seats after the right-wing Progress Party quit in January 2020 over the government’s immigration policies.

The minority government has since mostly stuck to battling COVID, but with the pandemic fading, the main economic issue has apparently shifted to the role Norway’s oil and gas industries should play in the economy.[v] Yet there doesn’t appear to be much daylight between the Conservatives and the main centre-left parties in contention—Labour and Centre—as all back continued drilling. Still, a centre-left coalition could depend on smaller, left-wing parties like the Greens, who want to end oil and gas exploration altogether and wind down fossil fuel industries. For her part, Solberg argues petroleum producers can invest in renewable energy sources and transition toward those new businesses.

In our view, there isn’t much difference between a Conservative-led minority government and a centre-left coalition riddled with internal squabbles—both would seem likely to lead to minimal change as competing interests water down initiatives. Whether Norway’s new ruling coalition is left or right-leaning, we don’t think it will hugely deviate from the present status quo. Political risk likely to surprise markets appears low to us.

Japanese general election: In developed markets, we think Japan is also worth watching politically, as a general election is due there by the end of November. Because the ruling Liberal Democratic Party (LDP) has a leadership election scheduled for September, many political observers we follow speculated that Prime Minister Yoshihide Suga might call an early election to consolidate power before his party’s contest.[vi] But given Japan’s extended COVID state of emergency during and after the Olympics—as well as Suga’s flagging popularity—reports indicate he is less likely to dissolve the lower house imminently. Yet the timing remains unknown, and the vote could be as soon as late September.

Possible leadership struggles and an uncertain election date aside, the LDP looks likely to govern (with Komeito, its longstanding party ally) for the foreseeable future, in our view, as Japan’s opposition parties remain in disarray. Whilst polls suggest LDP approval is relatively low around 30%, other parties garner only single-digit support.[vii] In other words, it seems likely to us Japan’s fall election mostly just extends the existing state of political affairs. We think this favours Japan’s multinational exporters, which have managed to thrive despite the ongoing gridlock and lack of progress on domestic economic reforms.

[i] “German SPD Overtakes Greens, Close in on Conservatives Before Election,” Staff, Reuters, 18/8/2021.

[ii] Source: CBCNews, as of 18/8/2021.

[iii] “Progressive Conservatives Surge to Surprise Majority Win in Nova Scotia Election,” Michael Gorman, CBC, 17/8/2021.

[iv] “Norway Government Faces Big Defeat in Sept Election, Poll Shows,” Staff, Reuters, 9/8/2021.

[v] “Trailing in Polls, Norway’s Prime Minister Says Oslo Remains Committed to Oil and Gas Drilling,” Richard Milne, Financial Times, 21/7/2021.

[vi] “Japan PM Suga Unlikely to Call Election in Early Sept., Late Nov. Possible,” Staff, Kyodo News, 18/8/2021.

[vii] Source: NHK, as of 9/8/2021.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today