Personal Wealth Management / Economics

Another Multi-Decade Inflation High

Falling uncertainty, not inflation, is likely key to returns from here.

Editors’ Note: Inflation has become a hot political topic, and we aren’t commenting on it from that standpoint. We are looking at the investment-related implications only.

9.1%. That is the latest multi-decade high the US’s Consumer Price Index (CPI, a broad measure of goods and services prices) year-over-year inflation rate hit in June.[i] Globally, commentators we follow focussed predominantly on what the acceleration from May’s 8.6% means for Federal Reserve policy, warning that continued aggressive interest rate rises could ripple worldwide, with the UK economy not spared from the dislocations.[ii] We suggest looking at inflation from a different standpoint. One of the most basic investing principles, according to our research, is that stocks move on the gap between sentiment and reality. Based on this, we don’t think stocks need prices to ease or interest rates to stay static. By our count, inflation is just one of seven or eight (at least) items weighing on sentiment globally right now. Therefore, we think the key to recovery isn’t fundamental improvement, but gradually easing uncertainty on a multitude of fronts.

So, what can we glean from US inflation data about the likelihood of stabilising prices stabilising investors’ moods? Based on our read of sentiment, the main source of uncertainty underlying inflation right now is the chief contributor: energy prices. Those rose 34.6% y/y, which included a 48.7% rise in petrol prices.[iii] (Ugh.) That fuelled a sharp divergence between headline and so-called core inflation, which excludes food and energy prices—not because they are meaningless (they aren’t), but because they are quite volatile and can occasionally mask underlying trends. Core CPI actually ticked a wee bit slower, from 6.0% y/y in May to 5.9%.[iv] That doesn’t mean inflation is for sure slowing from here, but we think it cuts against the notion that all prices are accelerating rapidly.

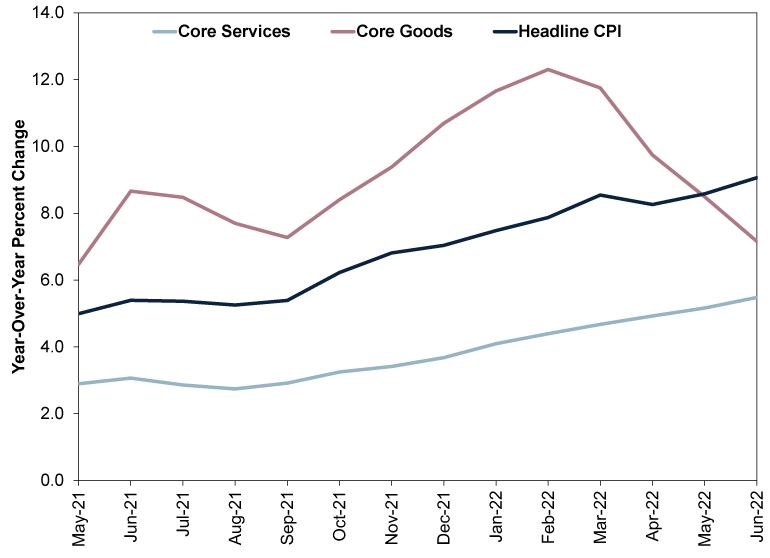

Perhaps equally encouraging, core goods prices (meaning, goods excluding energy and food) continued decelerating. We bring this up because energy prices aren’t the only place where oil prices can affect broader consumer prices. Oil is a raw input or feedstock for a number of consumer products—pretty much anything including plastic or other petrochemical derivatives, such as shoe soles, will have oil as an input. Early-year metal price spikes flowed through to consumer products similarly.[v] Combined, we think these are big reasons core goods inflation spiked to 12.3% y/y in February, as Exhibit 1 shows. But it is down significantly since, which we think reflects easing commodity prices across the board. Core services prices (which exclude energy services) have accelerated a bit, likely tied to higher operating costs, labour shortages and the general supply and demand imbalance caused by lockdowns and reopenings. If you have attempted to travel by air this summer, you know exactly what we are talking about. But the more these dislocations even out, the more prices are likely to stabilise.

Exhibit 1: A Deeper Look at Core Inflation

Source: FactSet, as of 13/7/2022.

In the meantime, though, we think inflation is less of a factor for markets than what we have observed to be a broad fear of it—fear that it will stay this high indefinitely. That fear appears to be combined with a number of intersecting fears, including interest rates, supply chains and China’s intermittent lockdowns, not to mention the all-encompassing recession chatter. We think it has created a massive cloud of uncertainty. The more clarity investors get on these fronts, provided things don’t get massively worse from here, the more we think it is likely to help stocks get over today’s jitters, map out the likely future, and move on. If signs of stabilisation in US core prices help that, great. If the recent relief in oil and other commodity prices helps too, then also great.[vi] But when considering inflation and stocks, whether in the UK, US or elsewhere, we suggest putting your focus there—the potential for falling uncertainty over the foreseeable future—and not inflation’s near-term ups and downs.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-02

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

-

Market Analysis Reviewing America’s Q1 Earnings and What Q2 Expectations Say2026-06-23

-

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today