Personal Wealth Management / Market Analysis

Assessing the Impact of the Latest Sanctions on Russia

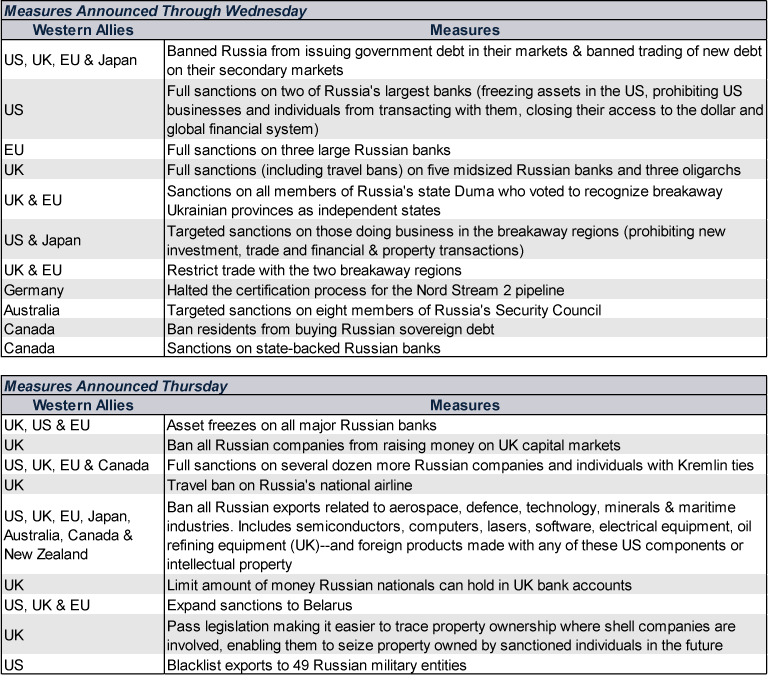

Rounding up measures announced thus far.

In the aftermath of Russian President Vladimir Putin’s full-scale invasion of Ukraine, the free world’s leaders announced fresh—and much tougher—sanctions Thursday.[i] What have the Group of Seven (G7—a group of major international leaders) allies announced thus far, which institutions are most exposed, and is there much risk of a downstream impact for the UK, US and Europe? Read on for the details and our analysis.

Now, to be clear, this article is a discussion of the intended effects of Western sanctions based on trade statistics and the announcements to date. However, our research shows sanctions’ real impact rarely matches the intent. Even rogue leaders like Vladimir Putin will likely find some third-party nation willing to trade with them, avoiding the sanctions for a small fee. Hence, we think sanctions’ likely economic impact—on Russia and the world—is smaller than the estimates that follow.

Until Thursday, the Western powers and their allies had refrained from some of the toughest measures in their arsenal, including banning Russia from the Society for Worldwide Interbank Financial Telecommunication (SWIFT) network, which facilitates international financial transactions, and cutting off semiconductor shipments. Instead, they opted for a gradual initial approach, promising to ratchet the punishment up if Putin didn’t back down.[ii] He didn’t, and now global leaders are starting to follow through on their earlier warnings.

UK Prime Minister Boris Johnson was first to announce a tougher response, including banning Russian companies from Britain’s capital markets and widening asset freezes and sanctions against banks, businesses and individuals.[iii] The US, EU, Japan, Australia, Canada and New Zealand soon followed, as part of a coordinated effort hammered out at emergency G7 and EU summits.[iv] Many of these announcements came after UK and European stock markets had closed for the day, yet US markets were still open, and we think their behaviour on the day is instructive. The S&P 500 index fell in the morning, echoing the declines across Europe.[v] Yet it rallied late in the day, finishing up 1.5% in USD.[vi] We don’t love reading into short-term gyrations, but we think it is noteworthy that US stocks turned up as the world got clarity on the Western response. As forecast by many news outlets we follow, Western leaders employed sanctions and stressed they would strengthen defenses in NATO nations, an effort to deter violence spilling beyond Ukraine.[vii] As we wrote earlier this week, we think uncertainty is the primary stock market negative where geopolitical conflict is concerned. That uncertainty has fallen substantially over the past 48 hours, after Russia declared war and other world leaders responded accordingly, even if the human toll has worsened significantly.

This situation is evolving quickly and there is a lot to track. To help, we made an omnibus table of everything announced thus far, keeping in mind that the EU has only issued a broad outline of its latest measures as we write.

Exhibit 1: Sanctions Announced Through Thursday

Source: CNN, The Yomiuri Shimbun, Reuters, UK Government, European Council and US Commerce Department, as of 25/2/2022.

More sanctions could come, as could a Russian response. Some financial commentators we follow speculate Russia could retaliate by barring exports to the West of key metals, gases and fertilisers, which could hamper production of catalytic converters (palladium), fighter jets (titanium) and semiconductors (neon).[viii]

We think one other notable omission is expulsion from SWIFT. In his speech to Parliament, Johnson noted that this remains on the table, but that “for all these measures to be successful, it is vital that we have the unity of our partners and the unity of the G7.”[ix] Biden’s statement later echoed this, implying some EU nations weren’t on board, perhaps tied to Germany’s and other EU nations’ reliance on Russian oil and gas.[x] Now, in the unlikely event things escalate and the West does agree to bar Russia from SWIFT, we think this would probably be where sanctions hit hardest, as it would interfere with Russia getting money for energy and other commodities. Yet, we think it would be a short-term effect in all likelihood, as there are other payment mechanisms they could use—and we think there are plenty of incentives on both sides to do so.

Wednesday’s measures were pretty light, as many financial observers we follow noted. Some just extended sanctions applied after Russia’s 2014 invasion of Crimea and the poisoning of several high-profile individuals including Russian opposition leader Alexei Navalny.[xi] The restrictions on debt issuance are new, but Russia has curbed its need for Western money since 2014. The Bank of Russia raised its foreign reserves from $486 billion (£362 billion) in March 2014 to $630 billion (£469 billion) at December’s end.[xii] That arsenal helped the bank put a floor under the rouble Thursday, halting a crash as currency and Russian stock markets swiftly incorporated the latest developments into share prices.[xiii]

As for debt sustainability, the sanctions and currency volatility impact external debt—Russian debt issued in global markets and currencies—only. Total external debt is down from $729 billion (£543 billion) at 2013’s end to $491 billion (£366 billion) in September 2021, the latest figure available.[xiv] Of that, only about $68 billion (£51 billion) is federal government debt, and only about $2.1 billion (£1.6 billion) matures over the next year, so Russia’s near-term financing needs are small.[xv] The near-term interest burden, which is where a plunging rouble would hurt, is also tiny.[xvi] Losing access to New York, London and Frankfurt will hurt Russian companies, in our view, but we think markets are already pricing this in, judging from the big hit Russian stocks have taken in recent days.[xvii]

We think Thursday’s measures, particularly the export controls, will likely have a larger impact—on Russia, not the allied exporters. The Biden administration estimates the bans will vaporise over half of Russia’s high-tech imports and cause severe headwinds for the country’s aerospace, defence and shipbuilding industries.[xviii] At the same time, Russia isn’t exactly a huge global consumer of these items—consistent with its economic clout being much, much smaller than its presence on the world’s political stage. The Semiconductor Industry Association estimates Russia buys less than 0.1% of the world’s computer chips.[xix] As for the broader restrictions, Russia received just $6.4 billion (£4.8 billion) of the US’s total $1.75 trillion (£1.3 trillion) in exports last year.[xx] Similarly, Russia accounted for just 0.9% of UK exports and 2.9% of the eurozone’s.[xxi] In other words, whilst we think this might be an incremental negative for some continental European nations, it is likely nowhere near enough to render a regional or global recession (broad decline in economic activity).

As for potential spillover effects in the financial world, at present, the risk seems miniscule, in our view. Like their Russian counterparts’ exposure abroad, Western banks have reduced direct exposure to Russia since 2014, limiting sanctions’ potential impact.[xxii] European banks are the most exposed, given their closer geographic links, but even there, major banks’ loans to Russia and Ukraine range from 0% to just 12% of total lending activity, and the banks on the high end aren’t enormous institutions overall.[xxiii] Given Russian banks secure the vast majority of their funding domestically—part of their efforts to reduce geopolitical risk to their operations after the Crimea invasion—Western banks’ counterparty risk to any problems in Russia’s banking sector appears small to us.[xxiv] We think the same goes for European banks’ Russian bond exposure, which ranges from 0.37% to 0.49% of total European bank assets.[xxv]

On the bond front, overall US residents—corporations and individuals—own just $14.3 billion (£10.7 billion) worth of Russian bonds.[xxvi] London real estate has some obvious exposure, given how many Russian oligarchs own mansions there, but most of that is through elaborate shell companies, and the government has had difficulty tracing ownership for years. There is now legislation in the works to address this, but it seems unlikely to prompt immediate change.[xxvii] Therefore, the likelihood of a sudden wave of forced sales dragging property values into the gutter therefore seems low to us.

If sanctions were to spiral into a full-blown trade war that upended the commodity supply chain, we think that could bring some pain. However, we think markets move on probabilities, not possibilities. Russia’s government revenue depends on the export of natural resources, and cutting off the West would be a severe hit, in our view.[xxviii] It would also hit Putin’s oligarch friends where it hurts most, and we think their personal support is critical to his maintaining power. We think it unwise to underestimate incentives in the country’s mafia-like political system. Furthermore, given a bit of time, commodities are pretty fungible (meaning, suppliers are interchangeable) and Western supply chains could shift—presenting a lasting headwind to Russia’s economy, in our view, if it were to lose clients in the long term.

As with the conflict at large, we will continue monitoring and sharing updated analysis and viewpoints as needed. But as it stands, sanctions thus far appear to fall far, far short of the scale necessary to materially harm the global economy and the likelihood violence spreads beyond Ukraine looks low, in our view. We think a few billion pounds here and there is a far cry from the few trillion pounds in damage it would take to cause a global recession.

[i] “The List of Global Sanctions on Russia for the War in Ukraine,” Michelle Toh, Junko Ogura, Hira Humayun, Caitlin McGee, Isaac Yee, Eric Cheung, Sam Fossum and Niamh Kennedy, CNN Business, 25/2/2022.

[ii] “Explainer: Western Sanctions on Banks Only Scratch Surface of Fortress Russia,” Tommy Wilkes and John McCrank, Reuters, 23/2/2022.

[iii] “Boris Johnson Announces ‘Largest Ever’ Set of Sanctions Against Russia,” Jessica Elgot, Heather Stewart and Aubrey Allegretti, The Guardian, 24/2/2022.

[iv] “G7 Leaders’ Statement on the Invasion of Ukraine by Armed Forces of the Russian Federation,” European Council of the European Union, 24/2/2022.

[v] Source: FactSet, as of 24/2/2022. Statement based on daily price movement of the S&P 500, MSCI UK, DAX, CAC 40 and Stoxx Europe 600 Indexes in local currencies. Currency fluctuations between the pound and dollar, euro and other currencies may result in higher or lower investment returns.

[vi] Source: FactSet, as of 24/2/2022. S&P 500 price return on 24/2/2022. Presented in US dollars. Currency fluctuations between the dollar and pound may result in higher or lower investment returns.

[vii] See Note i.

[viii] “Supply-Chain Threats from Russia-US Tensions,” Techcet, 1/2/2022.

[ix] “Everything Boris Johson Said in the Commons as He Condemned Putin and Imposed Sanctions on Russia,” Tom Beattie, The Chronicle, 24/2/2022. Accessed through MSN.

[x] “Remarks by President Biden on Russia’s Unprovoked and Unjustified Attack on Ukraine,” Speeches and Remarks, the United States White House, 24/2/2022.

[xi] See Note ii.

[xii] Source: Bank of Russia, as of 25/2/2022.

[xiii] Source: FactSet and Bank of Russia, as of 25/2/2022. Statement based on MSCI Russia price return in roubles on 25/2/2022. Currency fluctuations between the pound and rouble may result in higher or lower investment returns.

[xiv] See Note xii.

[xv] Ibid.

[xvi] Ibid.

[xvii] See Note xiii.

[xviii] “FACT SHEET: Joined by Allies and Partners, the United States Imposes Devastating Costs on Russia,” Statements and Releases from the United States White House, 24/2/2022.

[xix] “SIA Statement on Sanctions on Russia,” Semiconductor Industry Association, 24/2/2022.

[xx] Source: FactSet, as of 24/2/2022.

[xxi] Ibid.

[xxii] Source: Bank for International Settlements, as of 24/2/2022.

[xxiii] Source: Fisher Investments Research and company filings, as of 23/2/2022.

[xxiv] Source: Fisher Investments Research, as of 23/2/2022.

[xxv] Source: FactSet and Bank for International Settlements, as of 24/2/2022.

[xxvi] Source: US Treasury, as of 23/2/2022.

[xxvii] See Note vii.

[xxviii] “Why Russian Invasion Peril Is Driving Oil Prices Near $100,” Christopher M. Matthews and Collin Eaton, The Wall Street Journal accessed via Mint.com, 14/2/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today