Personal Wealth Management / Market Analysis

Checking In on Business Surveys, US Durable Goods and UK Retail Sales

How are developed economies holding up in the face of myriad headwinds?

As we approach Q1’s close, discussions about the global economy’s health abound in the financial publications we monitor. Besides ongoing warnings about rising prices, supply bottlenecks and COVID outbreaks potentially posing headwinds, Russia’s invasion of Ukraine added a new wildcard. Whilst dour projections are myriad, we think it is beneficial for investors to focus on actual data—and we got a bunch last week.[i] Here we break down both the numbers and the broad reaction to them from financial commentators we follow.

March Business Surveys Flash Some Positive Signs

First up: S&P Global’s March flash purchasing managers’ indexes (PMIs, which are widely watched business surveys)—the artists formerly known as IHS Markit PMIs.[ii] These are surveys measuring whether companies’ purchasing managers reported improvement or deterioration across a range of categories. Despite a few soft patches, they broadly showed continued growth across the developed world. (PMIs above 50 imply expansion.)

Exhibit 1: March Flash PMIs

Source: S&P Global, as of 28/3/2022.

March’s preliminary results surprised largely to the upside based on financial coverage we track.[iii] We found many experts projected weaker readings due to Russia-Ukraine fallout—both directly (due to the eurozone’s reliance on Russian gas) and indirectly (the potential spillover effect on already strained global supply chains).[iv]

Now, the war has likely weighed on economic activity to an extent, particularly in eurozone nations: Germany’s composite PMI dipped a point to 54.6 as manufacturing businesses reported slower growth due to supply problems and weaker demand tied to the conflict.[v] But we have observed economic forecasters argue the eurozone risked a recession due to Ukraine-related disruptions (e.g., soaring energy costs would crimp growth).[vi] So far, we think PMI data argue against that. A major escalation in the war could hurt a larger share of global gross domestic product (GDP, a government-produced measure of economic output), but we think that is only a possibility, not a probability, today.

Our review of the data also shows an offset to the war’s negative economic impact right now: easing COVID restrictions. Our research shows reopenings benefit the services sector in particular—especially those in people-facing industries (e.g., hospitality and travel)—and March’s flash PMIs highlighted this positive trend. France’s composite PMI hit an eight-month high thanks primarily to services’ growth, and the UK’s reopening buoyed its services PMI to a nine-month high as workers returned to the office, which boosted urban foot traffic, and demand increased for travel and leisure activities.[vii] Whilst Japan’s services PMI indicated contraction, businesses there reported a milder decline in output thanks to falling COVID cases and the lifting of the quasi-state of emergency across the country late in the month.[viii]

PMIs reveal the breadth of growth, not its magnitude, which means we don’t know the extent to which output grew. Perhaps Q1 economic output slowed or even contracted in some nations—we will know only when quantifiable data come out in the coming weeks. But in our view, the latest PMIs suggest economic activity is holding up better than many economic commentators we follow appreciate.

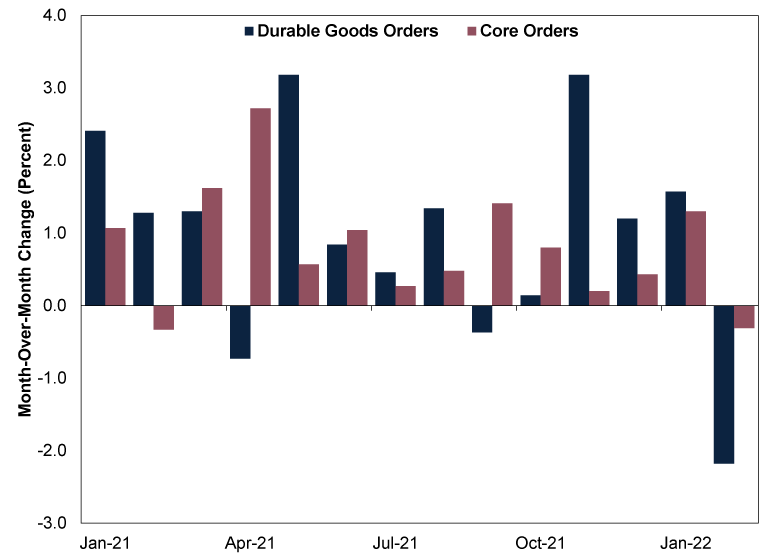

What to Make of US Durable Goods Orders’ Dip?

US February durable goods orders fell -2.2% m/m, their first dip in five months.[ix] (Durable goods refer to infrequently purchased consumer products expected to last for at least three years—an automobile, for example.) Moreover, the widely watched core orders component—nondefense capital goods orders excluding aircraft, which many economists we follow treat as a proxy for US business investment—fell -0.3%, its first decline in 12 months.[x] Economists we follow pinned the drop-off on two volatile categories: motor vehicles and parts (-0.5% m/m) and nondefence aircraft and parts (-30.4%).[xi]

Some financial coverage we track posited current economic headwinds—e.g., the Russia-Ukraine war or new COVID outbreaks in China—could knock durable goods demand, though we think this projection seems a bit premature.[xii] For one, not all categories were weak, as defence capital goods orders rose 14.2% m/m in February after jumping 18.5% m/m in January.[xiii] Defence aircraft and parts soared 60.1% m/m last month, and we think the surge in demand was likely due at least partially to the conflict in Eastern Europe.[xiv] Two, a single monthly dip doesn’t negate the growthy longer-term trend, in our view. (Exhibit 2) Durable goods orders’ resilience has persisted despite supply shortage and bottleneck issues over the past year, and we doubt the Russia-Ukraine war is the gamechanger that derails demand.

Exhibit 2: US Durable Goods Orders and Core Orders, January 2021 – February 2022

Source: FactSet, as of 28/3/2022.

UK Retail Sales: More Than a Case of Rising Prices

UK retail sales volumes—which measure the quantity of goods bought—dipped -0.3% m/m in February, short of expectations of 0.2%.[xv] Since retail sales values (which reflects the amount spent) rose 0.7% m/m, we observed some economists argue elevated prices were now taking a bite out of UK consumers’ spending power.[xvi] But reality is more complicated, in our view. Some spending shifted away from food stores (-0.2% m/m) as the UK ended its most recent COVID restrictions, allowing people to dine out again.[xvii] Since the Office for National Statistics (ONS) doesn’t track food service (e.g., restaurants and pubs) in its retail sales report, that spending shift likely detracted from the headline number. Excluding food stores, sales volumes rose 0.6% m/m.[xviii] The ONS also noted some retailers reported less footfall due to February’s stormy weather.[xix] Our research has found inclement weather has negatively impacted economic data before, as was the case during 2018’s big winter storm (dubbed the “Beast from the East”), which weighed on UK retail sales early in the year.[xx]

In our view, this is a timely reminder to dig beyond the dominant headline—in this case, elevated inflation (economy-wide rise in prices). We don’t dismiss rising prices, as our research shows they are likely impacting many households’ spending decisions today. Yet higher inflation is but one factor impacting consumers’ choices, in our view. Recognising headlines don’t tell the whole story can help investors filter through the noise, in our view, and help them determine whether reality aligns with the consensus view or not—a useful perspective to have in investing.

[i] “IMF Expects to Cut Global Growth Forecast in Response to Russia-Ukraine War, Managing Director Says,” Krystal Hur, CNBC, 10/3/2022.

[ii] Our spellcheckers and autocorrect tools are grateful for this change.

[iii] “Euro Zone March Business Growth Strong but Outlook Darkens – PMI,” Jonathan Cable, Reuters, 24/3/2022.

[iv] Ibid.

[v] Source: S&P Global, as of 28/3/2022.

[vi] “War Fallout: U.S. Economy to Slow, Europe Risks Recession and Russia to Suffer Double-Digit Decline,” Steve Liesman, CNBC, 6/3/2022.

[vii] See note v.

[viii] Ibid.

[ix] Source: FactSet, as of 28/3/2022.

[x] Ibid.

[xi] Source: Census Bureau, as of 28/3/2022.

[xii] “US Durable Goods Orders Slip in February, Marking First Decline in 5 Months,” Megan Henney, Fox Business, 24/3/2022.

[xiii] See note xi.

[xiv] Ibid.

[xv] Source: FactSet, as of 28/3/2022.

[xvi] Source: ONS, as of 28/3/2022.

[xvii] Ibid.

[xviii] Ibid.

[xix] Ibid.

[xx] “High Street Sales Feel Chill From ‘Beast From the East’,” Richard Partington, The Guardian, 28/3/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-14

-

Politics Can Germany Engineer Faster Growth at Last?2026-07-08

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-02

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

Contact Us

Learn why 210,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 30/06/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today