Personal Wealth Management / Market Analysis

For Underappreciated Growth, Look East

February services PMIs point to growth in a large part of the global economy.

New month, new batch of business surveys. We highlighted February flash purchasing managers’ indexes (PMIs, monthly surveys that track the breadth of economic activity, where readings above 50 indicate expansion, below 50, contraction) for the US, UK and eurozone recently, and we noted that we don’t think the final readings revealed much new insight. But on Friday, S&P Global released a spate of expansionary services PMIs. February growth, particularly out of the Asia and Pacific region, suggests activity from a big part of the global economy is likely rebounding—an overlooked positive, in our view.

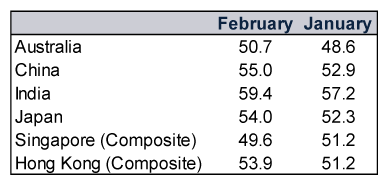

Most of S&P Global’s services PMIs out of the Pacific topped 50 in February—implying expansion. (Exhibit 1)

Exhibit 1: Services PMIs Out of the Pacific

Source: FactSet, as 3/3/2023. Composite PMIs combine services and manufacturing output.

Easing COVID restrictions contributed to higher services sector activity in China, Hong Kong and Japan in particular.[i] Now, we have seen this type of rebound before, both in China and elsewhere, but February’s growth wasn’t tied solely to the removal of pandemic measures, in our view.[ii] According to S&P’s release, resilient domestic demand and strong new orders drove India’s fastest services PMI expansion in 12 years—an encouraging sign after India’s gross domestic product’s (GDP) slowdown from Q3’s 6.3% y/y to Q4’s 4.4%.[iii] Australia’s services PMI edged above 50 for the first time since last September thanks to stable demand and businesses catching up on outstanding orders.[iv] PMIs indicate economic growth’s breadth, not its magnitude, and our research finds they don’t always correlate with output measures. But simple maths dictate that even slow growth contributes to global GDP.

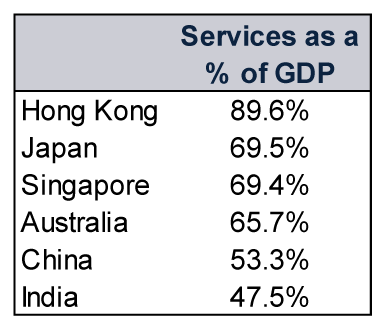

We think services growth is noteworthy given the attention some Asian manufacturing numbers received from financial publications we follow earlier last week. Though commentators cheered the jump in China’s factory activity—the official February manufacturing PMI rose to 52.6 from January’s 50.1—many observers we follow focussed on Japan’s February manufacturing PMI falling to 47.7 from January’s 48.9, its worst reading since September 2020.[v] But similar to major economies in North America and Western Europe, the services sector drives the lion’s share of activity in major Asian and Pacific economies. (Exhibit 2) Even in China, services comprises the majority of output. Combined, these six economies make up nearly 30% of global GDP—so reaccelerating growth here contributes nicely to the global economy.[vi]

Exhibit 2: Services’ Share in Select Asia and Pacific Economies

Source: The World Bank, as of 3/3/2023. All figures reflect 2021 except for Japan (2020).

Consider, too, that Asia does a lot of the heavy lifting for the global economy. According to the International Monetary Fund (IMF), growth in the region slowed sharply last year—as was the case worldwide.[vii] Though the supranational organisation projects growth in North America, Western Europe and advanced economies in general will decelerate again this year, it projects growth in Asia and the Pacific will accelerate.[viii] Now, we always take these forecasts with a grain of salt, as they are regularly revised as new data come in and conditions evolve. But even if other regions slow as the IMF forecasts (e.g., the eurozone and the UK), we think faster expansion in the Pacific may pull the weaker areas along and buoy demand for goods and services provided by publicly traded companies the world over. We think February PMIs are an early indication this may be happening—an underappreciated positive worth noting for global investors, in our view.

[i] “How China’s New No.2 Hastened the End of Xi’s Zero-COVID Policy,” Julie Zhu, Yew Lun Tian and Engen Tham, Reuters, 2/3/2023. Accessed via the Internet Archive. “Japan to Lower COVID-19 to Flu Status, Further Easing Rules,” Mari Yamaguchi, Associated Press, 19/1/2023. Accessed via Yahoo! Finance. “Hong Kong Ends Last Covid Curbs in Bid to Revive Finance Hub,” Jinshan Hong, Bloomberg, 28/12/2022. Accessed via MSN.com.

[ii] Source: FactSet, as of 7/3/2023. Statement based on China and US GDP, Q1 2020 – Q4 2022.

[iii] Source: FactSet and S&P Global, as of 3/3/2023. GDP is a government-produced measure of economic output.

[iv] Source: S&P Global, as of 3/3/2023.

[v] Source: FactSet, as of 3/3/2023.

[vi] Source: The World Bank, as of 3/3/2023. Statement based on GDP (constant 2015 USD) for World, China, Japan, Hong Kong, Singapore, Australia and India in 2021.

[vii] Source: The IMF, as of 3/3/2023. IMF Data Mapper based on World Economic Outlook (October 2022).

[viii] Ibid.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

-

Market Analysis Reviewing America’s Q1 Earnings and What Q2 Expectations Say2026-06-23

-

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-23

-

Macro Insights SpaceX IPO and Rising Equity Supply2026-06-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today