Personal Wealth Management /

The Investor’s Guide to Last Week’s Brexit Votes

Last week’s Brexit amendment votes perhaps narrowed potential outcomes somewhat, but uncertainty remains.

MPs voted 29 January on several amendments to Prime Minister Theresa May’s “Plan B” for the terms of Britain’s exit from and future relationship with the EU, following Parliament’s earlier rejection of her deal with the EU. Plan B looked a lot like the initial deal—including the controversial “Irish backstop,” which would leave the UK in the EU’s customs union and Northern Ireland in its single market if negotiators didn’t reach a permanent trade agreement—plus a few small concessions aimed at rallying support from eurosceptic Tories and even some Labour MPs. Of the seven amendments selected by Commons Speaker John Bercow for a vote, only two passed. One was a non-binding rejection of a so-called “no-deal” Brexit, whilst the other instructed May and EU leaders to replace the Irish Backstop with “alternative arrangements.” Their passage prompted rampant discussion throughout financial media, with many observers speculating about the potential impact on financial markets. In our view, they don’t appear to much alter Brexit’s course. They might render a Brexit delay or second referendum less likely than they perhaps appeared before last week, but the endgame still appears unclear. Investors still await clarity, and only time will tell if the next vote—the much-anticipated “meaningful vote”—set for 14 February, delivers it.

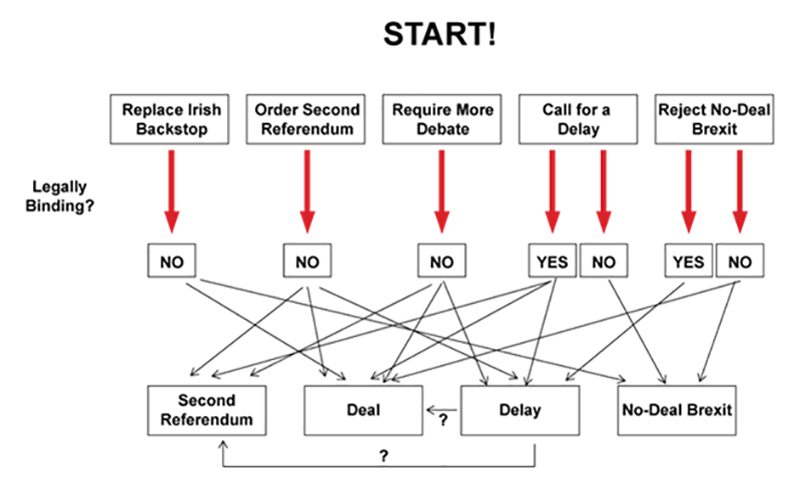

Exhibit 1, whilst a tad oversimplified, aims to summarise the many ways Brexit could have gone before last week’s votes. The starting point is May’s Plan B—her original deal, plus provisions giving MPs more input into a potential free trade deal with the EU, pledging to renegotiate the Irish backstop and increase protections for workers. The second row is a simplified aggregation of the proposed amendments, which combines overlapping amendments into general categories (e.g., combining four different extend the Brexit deadline amendments into one box). The third row specifies whether each would have been legally binding. The fourth, at last, attempts to show how all led, in different ways, to one of four general outcomes: a Brexit deal, a delay, a no-deal Brexit and a second referendum.

Exhibit 1: Simplified Rendering of Brexit Amendment Proposals

Source: Based on various coverage in The Telegraph and The Guardian, as of 29/1/2019.

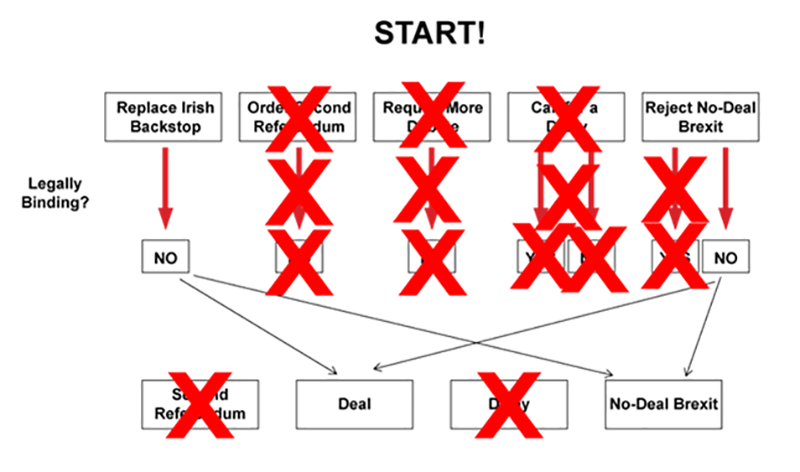

In the end, only two passed: Dame Caroline Spelman’s nonbinding rejection of a no-deal Brexit and Sir Graham Brady’s requirement that May replace the Irish backstop with “alternative arrangements.” The latter, which May’s government supported, may seem redundant considering a pledge to renegotiate the backstop was part of Plan B. But May’s initial provision didn’t go far enough for many eurosceptic Tories, as it didn’t commit to changing the Withdrawal Agreement’s legal text. Several MPs seemingly worried, based on their various media comments, that all she would get from the EU was nonbinding political statements that wouldn’t guarantee against what they considered to be the backstop’s less satisfactory provisions. So they tabled the amendment, which urges changes to the legal text and pre-pledges MPs’ support for the amended agreement. This compromise would theoretically seal mid-February’s meaningful vote.

We say “theoretically” because it, too, is nonbinding. It also seems too vague to mean much, as “alternative arrangements” could seemingly mean anything. Adding a wrinkle, the EU’s response was swift, refusing to reopen the Withdrawal Agreement, and their stance does not appear to have changed in the subsequent days. It takes two to negotiate, and EU leaders aren’t beholden to nonbinding acts of the UK Parliament. They also seem to find “alternative arrangements” vague and don’t appear confident they can concede anything that would pass Parliament.

This leaves Brexit in approximately the same limbo as it was before the amendments, in our view. Whilst this wasn’t MPs’ last chance to influence Brexit terms, MPs’ repeated rejection of delaying Brexit and opening the door to a second referendum likely means those possible outcomes aren’t viable. Some cabinet members have since spoken more of delaying Brexit, but as many political media analysts have noted, it seems meaningful that MPs refused to vote for this option when presented with it. Although they can’t be completely ruled out, the relevant amendments failed by dozens of votes, and it would take a big swing for them to go differently next time. Thus, it seems likely markets can narrow the field to Brexit happening on 29 March with a deal—or without a deal. This doesn’t enable businesses to start executing contingency plans, but it likely gives them fewer options to consider, as depicted in Exhibit 2.

Exhibit 2: Simplified Rendering of Brexit Amendment Results

Source: Based on various coverage in The Telegraph and The Guardian, as of 29/1/2019.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Brazil Review & Outlook2026-06-04

-

Market Analysis Global Bond Calamity Calls for Calm Perspective2026-05-27

-

Economics A May Global Economic Check-In2026-05-26

-

Macro Insights Macro Insights Q2 20262026-05-22

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today