Personal Wealth Management / Market Analysis

Italy’s Debt Likely Remains Affordable

Political uncertainty doesn’t change Italy’s debt affordability much, in our view.

Editors’ note: MarketMinder is nonpartisan, preferring no party nor any politician. Our analysis aims solely to assess political developments’ potential market impact.

According to many commentators we follow, it was supposedly a double whammy for Italian bond markets last Thursday after (now caretaker) Prime Minister Mario Draghi resigned and the European Central Bank (ECB) hiked its benchmark interest rate by half a percentage point (ppt). Italy’s 10-year yield rose 0.22 ppt on the day to 3.58%—its highest since bond markets threw a tantrum during 2020’s initial COVID lockdowns.[i] Commentators now say a financial crisis is brewing, but we don’t think one looks any more likely than last month.

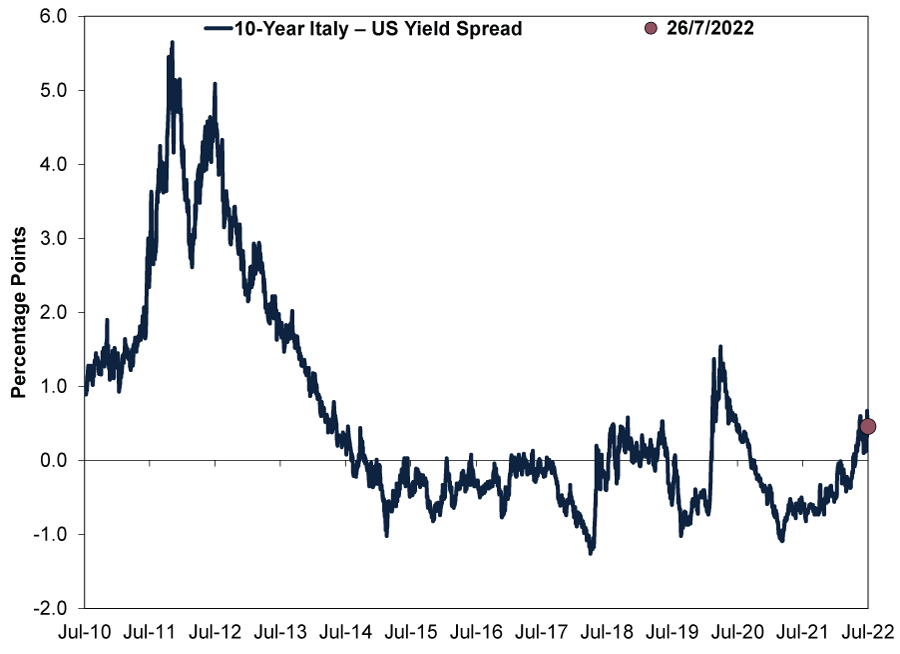

One popular measure of default risk is the credit spread—the difference between the country’s yields and the yields of a country with minimal risk. The wider the spread, the higher the perceived risk of default, as it shows investors require extra compensation to take the excess risk. Exhibit 1 shows Italy’s credit spread versus US Treasurys, which has widened lately. Yet that move alone doesn’t guarantee trouble, in our view. Whilst widening credit spreads can point to possible financial stress, our historical research shows they don’t automatically signal imminent default. Based on our observations, Italy is familiar with this. In April 2020, Italy’s 10-year yield spread against global benchmark US Treasurys widened to 1.54 ppts.[ii] During the eurozone’s debt crisis, it hit 5.65 ppts.[iii] In neither case did Italy default.[iv] (Note: We use US Treasurys as the benchmark—rather than, say, German bunds—because of America’s perceived global financial safe-haven status. In an existential euro crisis, we think capital probably wouldn’t flee to another eurozone member.)

Exhibit 1: The 10-Year Italian-US Credit Spread Widened Some

Source: FactSet, as of 26/7/2022. 10-year Italian yield minus 10-year US yield, 26/7/2010 – 26/7/2022.

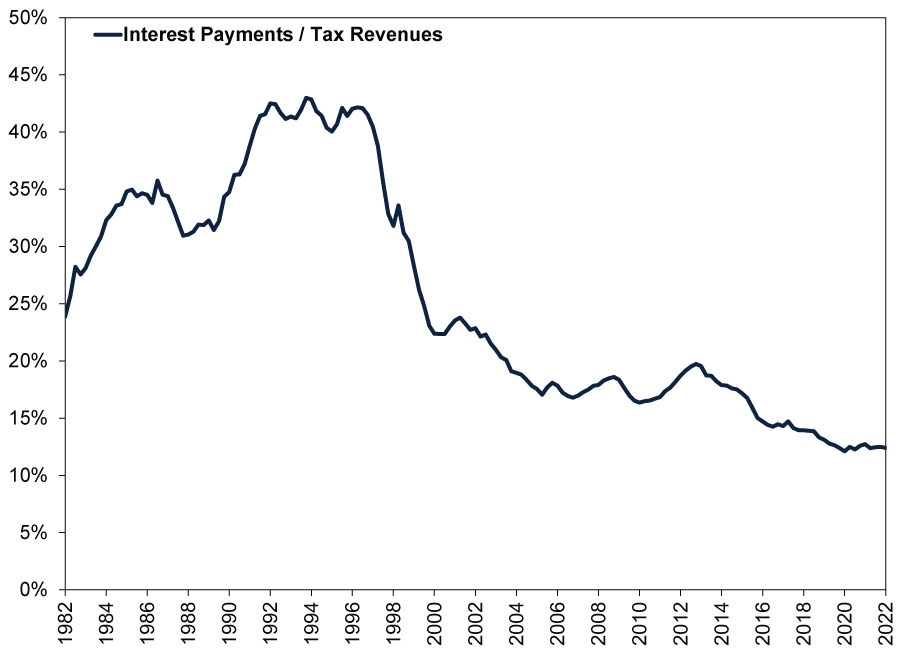

Italian bond yields’ latest move looks mostly sentiment driven to us—fundamentally, the data we find most meaningful indicate Italy can easily service its debts. Exhibit 2 shows Italy’s interest payments are about 12% of tax revenues, well below the 1990s’ 40%+ rates. As Italy didn’t default three decades ago, we don’t think it is likely to now. Commentators we read still warn rising yields will make Italy’s debts increasingly unaffordable, but they likely have a long wait. Italian bonds’ weighted-average maturity is over seven years.[v] From today’s 3.25% 10-year rate—far below early-1990s’ low-teens—yields would have to skyrocket and stay elevated several years for debt payments to balloon unsustainably, in our view.[vi]

Exhibit 2: Italy’s Increasingly Affordable Debt Load

Source: FactSet, as of 26/7/2022. Italian interest payments as a percent of tax revenues, Q1 1982 – Q1 2022.

How likely is that? In the wake of Italy’s centrist technocratic coalition’s demise, news reports suggest that a new government led by the far-right Brothers of Italy—who presently lead polls—won’t adhere to reforms unlocking EU pandemic relief funds, possibly jeopardising the fiscal outlook.[vii] But we find where the next government falls on the political spectrum isn’t the most relevant question for investors. It is: Can it push through radical legislation?

With two months until 25 September’s vote, election outcomes aren’t certain. In our experience, polls aren’t predictive—and they can change. Also, after voters approved constitutional reforms via referendum in 2020, this election will be for far fewer seats in Parliament.[viii] These reforms cut lower-house seats to 400 from 630 and upper-house seats to 200 from 315.[ix] Theoretically, this may make it easier to form a majority, but they have yet to run the experiment. How it all shakes out is anyone’s guess, in our view. At this point, we think the government’s future make up isn’t knowable, and what it can accomplish, even less so.

Italy has seen similar political upheaval before—without much change to its financial standing that we can see. Headline alarms over a populist government takeover became reality in 2018 when the anti-establishment Five Star Movement came to power with the nationalist League’s support.[x] Look back to Exhibit 1: That is when Italian bond yields spiked, albeit only to parity with US Treasurys. But with barely any overlap in the governing parties’ ideology or objectives, political gridlock ensued.[xi] They accomplished little, and the government was short-lived.[xii] Subsequent governments haven’t proved much more active, in our view, and whilst the next might be more ideologically aligned, that doesn’t ensure radical policies’ passage. On both the right and left sides of the spectrum, there are pro- and anti-euro factions, not to mention other internal differences.[xiii] As in the rest of the developed world, it wouldn’t surprise us if gridlock’s reign continues in Italy’s fractured political landscape. In any case, we will be watching.

As for the ECB’s half-point hike to all of 0%, it wasn’t exactly shocking, considering ECB President Christine Lagarde had teed it up earlier in the week.[xiv] It also follows other major monetary policy institutions’ rate hikes. Possibly more relevant for Italy: the ECB’s new Transmission Protection Instrument (TPI)—the so-called anti-fragmentation defence it has been floating for months. The TPI allows targeted ECB bond buying “to counter unwarranted, disorderly market dynamics that pose a serious threat to the transmission of monetary policy across the euro area.”[xv] This is supposed to prevent more indebted eurozone members’ borrowing costs from spiking.[xvi] As the ECB’s thinking goes, its rate normalisation path depends on its monetary policy being appropriate for all member countries.[xvii] In more ECB-speak:

“Subject to fulfilling established criteria, the Eurosystem will be able to make secondary market purchases of securities issued in jurisdictions experiencing a deterioration in financing conditions not warranted by country-specific fundamentals, to counter risks to the transmission mechanism to the extent necessary. The scale of TPI purchases would depend on the severity of the risks facing monetary policy transmission. Purchases are not restricted ex ante.”[xviii]

In our view, this just further formalises Draghi’s 2012 promise to do “whatever it takes to preserve the euro” when he was ECB president.[xix] But as the ECB is the eurozone’s lender of last resort anyway, we don’t see this as particularly necessary—much less for Italy, which appears more than capable of paying its way.[xx] The long-running notion that only the ECB is keeping Italian debt affordable is false, in our view. In December 2018, after the ECB stopped asset purchases and ended quantitative easing (QE), Italian 10-year bond yields fell below equivalent maturity US Treasurys without the ECB’s alleged support—until QE’s March 2020 restart amidst pandemic lockdowns. [xxi]

Note, too, that even with the sentiment-fuelled spike in yields this year, Italy’s Treasury is still refinancing a lot of its maturing debt at a discount.[xxii] 10-year Italian bonds coming due now carry coupons around 5%. Current 10-year yields are below that, meaning Italy’s actual funding costs are continuing to decrease.[xxiii] For investors, we think all the hubbub over Italian debt is just another sentiment brick in the wall of worry. In our view, however the next few months’ political chips may fall, Italy’s underlying economic reality will likely prove better than most commentators we follow suggest.

[i] Source: FactSet, as of 26/7/2022. 10-year Italian yield, 21/7/2022.

[ii] Source: FactSet, as of 26/7/2022. 10-year Italian yield minus 10-year US yield, 22/4/2020.

[iii] Source: FactSet, as of 26/7/2022. 10-year Italian yield minus 10-year US yield, 29/11/2011.

[iv] “BoC–BoE Sovereign Default Database: What’s New in 2021?” David Beers, Elliot Jones, Zacharie Quiviger and John Walsh, Bank of Canada, June 2021.

[v] Source: Italian Department of the Treasury, as of 26/7/2022. Weighted average life of government bonds, June 2022.

[vi] Source: FactSet, as of 26/7/2022. 10-year Italian yield, 26/7/2022.

[vii] “Mario Draghi Resigns, Plunging Italy Into Political Turmoil,” Crispian Balmer, Giuseppe Fonte and Angelo Amante, Reuters, 21/7/2022. Accessed through the Internet Archive.

[viii] “Referendum Costituzionale 2020,” Ministero Dell’Interno, 18/9/2020.

[ix] “Costituzione Italiana,” Senato Della Repubblica, 11/2/2022.

[x] “Italy’s 5-Star, League Government Alarms Country’s Financial Sector,” Valentina Za and Massimo Gaia, Reuters, 18/5/2018. Accessed through Yahoo!

[xi] “Italian Populist Says He and Rival Have Deal on New Premier,” Staff, Associated Press, 20/5/2018.

[xii] “From One Marriage of Convenience to Another: Will Italy’s New M5S-PD Government Last Longer Than Its Predecessor?” Staff, LSE, 5/9/2019.

[xiii] “Explainer: Who Gains or Loses, What’s Next in Italy Crisis,” Frances D’Emilio, Associated Press, 21/7/2022.

[xiv] “ECB Weighs Bigger Rate Hike With Safety Net for Indebted Countries,” Francesco Canepa and Balazs Koranyi, Reuters, 19/7/2022. Accessed through MSN.

[xv] “Monetary Policy Decisions,” Staff, ECB, 21/7/2022.

[xvi] “Factbox: ECB Unveils New TPI Anti-Fragmentation Instrument,” Staff, Reuters, 21/7/2022. Accessed via the Internet Archive.

[xvii] Ibid.

[xviii] “The Transmission Protection Instrument,” Staff, ECB, 21/7/2022.

[xix] “Verbatim of the Remarks Made by Mario Draghi,” Mario Draghi, ECB, 26/7/2012.

[xx] Source: FactSet, as of 26/7/2022. Statement based on Italian interest payments as a percent of tax revenues, Q1 2022.

[xxi] Source: FactSet, as of 26/7/2022. Statement based on 10-year Italian yield minus 10-year US yield, December 2018 – March 2020.

[xxii] Source: Italian Department of the Treasury, as of 26/7/2022.

[xxiii] Source: FactSet, as of 26/7/2022. Statement based on 10-year Italian yield, 26/7/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Assessing Private Credit Risks and Exposures2026-06-09

-

Macro Insights SpaceX IPO and Rising Equity Supply2026-06-09

-

In The News Trump’s tariff turmoil isn’t just delayed – it’s never coming2026-06-08

-

Macro Insights Brazil Review & Outlook2026-06-04

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today