Personal Wealth Management / Market Commentary

Italy’s Recession Isn’t Likely Contagious

We see a few reasons why Italy won’t tip the rest of the eurozone economy into recession.

Italian gross domestic product (GDP)—a government-produced estimate of national economic output—fell -0.2% q/q in Q4. The dip is the second straight quarterly contraction, meeting one popular definition of a recession.[i] In the financial press we survey, this 31 January news release came with fears the eurozone’s third-largest economy will drag down the entire bloc. Yet a deeper dive suggests that may be a hasty judgment, in our view. Whilst Italy and the eurozone share some headwinds, our research shows some unique local factors made Italy more vulnerable. With those headwinds likely to fade soon, in our view, we think economic reality should surpass dreary expectations we find widespread in the media today. Expectations beating reality typically fuels rising equity markets.

Italy’s Q4 GDP contraction follows Q3’s -0.1% q/q dip.[ii] Although GDP details remain scarce, commentary from Italy’s national statistics office and companies surveyed by economic research firm IHS Markit hinted at weakness being concentrated in fixed investment, manufacturing and exports. Weak fixed investment likely resulted from Italian interest rates spiking higher during autumn’s budget standoff with the EU. The budget spat drove 10-year Italian government debt yields up to 3.6% in October from 2.8% in September.[iii] Whilst 3.6% isn’t historically high, we suspect the sharp spike may have temporarily deterred borrowing, with downstream impacts on business investment. This is doubly the case here, in our view, as the jump looked fear-driven and likely fleeting. According to our analysis, temporary rate spikes often cause businesses to delay funding planned investments as they wait for rates to subside before locking in years’ worth of interest expenses. It is sound financial management to take a wait-and-see approach before making a long-term decision. With Italy’s budget standoff now over and rates lower, firms are better able to pursue business plans, borrowing and investment they may have hesitated to undertake last autumn. In our view, this probably pushed some economic activity from late 2018 into early 2019.

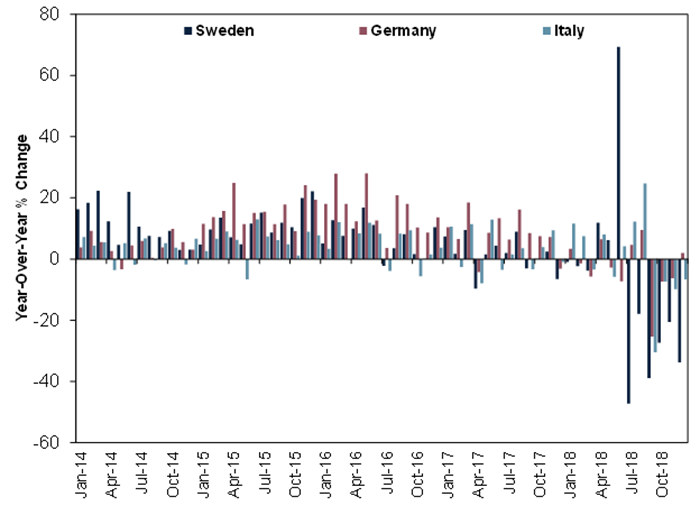

We think new EU emissions standards also likely pinched Italy in the autumn. These seemed to hit Italian industrial production, which fell in all three months during Q4, dropping -0.8% m/m in December.[iv] They also apparently drove deteriorating manufacturing purchasing managers’ indexes (PMIs)—surveys estimating the percentage of businesses that grew in a given month. The new standards took effect in September, creating production problems automakers needed to solve, according to industry reports. For example, Volkswagen estimated higher standards would interrupt production of 200,000 – 250,000 vehicles in 2018’s second half.[v] Whilst Germany is more known for auto production and felt a related GDP hit in Q3 (as did Sweden), Italy is also vulnerable because many Italian manufacturers supply German carmakers. Auto sales figures hint at consumers buying ahead of the new regulations, with sales jumping before the rules took effect and falling through yearend. (Exhibit 1) This is normal when changes like this take effect, in our view, and we think it usually proves short-lived as everyone adapts to the new regime.

Exhibit 1: New Passenger Car Registrations

Source: FactSet, as of 18/1/2019. New passenger car registrations, January 2014 – December 2018. Sweden’s effect is magnified by an additional sales tax designed to promote electric cars.

Export weakness, the last main Q4 GDP drawback, was a global headwind seemingly stemming from weak private sector demand in China. Whilst many blame tariffs, according to our research, it more likely results from China’s 2018 crackdown on shadow banking—lending occurring outside the traditional banking system—which mostly finances small and medium sized enterprises (SMEs). Whilst credit kept flowing from banks, government and industry reports suggest they lent primarily to large state-owned enterprises that didn’t need it as much versus picking up the slack from shadow lenders. Hence, it appears the government’s crackdown disproportionately affected China’s millions of small private businesses—its primary growth engine. But this should reverse soon, as Chinese fiscal and monetary authorities have implemented stimulus measures in recent weeks, aimed primarily at SMEs. Should those start bearing fruit in the coming months—and we expect they will—we think they should help bolster demand.

Whilst Italy’s weak areas garner the most headlines in the media we survey, the bulk of its economy—services and consumption—appears to be holding up better. Whereas fixed investment is less than 20% of Italian GDP, consumer spending is about 60%.[vi] Italian retail sales—although not entirely representative of overall consumer spending—accelerated from a 0.2% m/m October gain to 0.7% in November.[vii] The Italian National Institute of Statistics hasn’t yet released figures for Q4 services spending—almost two-thirds of total household consumption—but it described last quarter’s service sector production, nearly four times the size of Italy’s manufacturing sector, as “substantially stable.”[viii]

Beyond Italy, most of the eurozone grew in Q4. German composite PMI—combining manufacturing and services—strengthened to 52.1 in January (readings above 50 indicate more than half of responding companies reported increasing business activity), suggesting growth continues.[ix] Meanwhile, French Q4 GDP grew and beat analysts’ expectations. Spanish Q4 GDP grew 0.7% q/q—up from Q3’s 0.6% and ahead of consensus estimates.[x] Combined, their GDPs far outweigh Italy’s. The eurozone’s composite PMI was 51.0 in January—signalling growth on the Continent is chugging along.[xi] Yet in our survey of the media, positive Q4 eurozone economic reports gathered few headlines. The media’s apparent focus on Italy, whilst overlooking a brighter bigger picture, is a classic example of sentiment underrating reality, in our view.

Italy may have fallen into a shallow recession, but we think the evidence argues against a prolonged downturn in Italy and the eurozone. We think the future is brighter than most people fear. Hence, we don’t think it would take much to positively surprise investors and boost shares. In our view, that is the likely path forward.

[i] Source: Istat, as of 31/1/2019. Q4 2018 Real GDP.

[ii] Source: Istat, as of 31/1/2019. Real GDP, Q3 and Q4 2018.

[iii] Source: FactSet, as of 5/2/2019. 10-year Buoni del Tesoro Poliannuali (BTP) yield, 18/9/2018 and 19/10/2018.

[iv] Ibid. Italy industrial production, October and November 2018.

[v] “VW Says 250,000 Cars Could Be Delayed by New Testing Rules,” Andreas Cremer and Jan Schwartz, Reuters, 8/6/2018.

[vi] Source: FactSet, as of 5/2/2019. Gross Fixed Capital Formation and Household Consumption Expenditures as a percentage of GDP, Q3 2018.

[vii] Source: Istat, as of 10/1/2019. Retail trade index, October and November 2018.

[viii] “Italy Fourth-Quarter GDP Contracts, Throwing Economy Into Recession,” Gavin Jones, Reuters, 31/1/2019.

[ix] Source: IHS Markit, as of 5/2/2019. German Composite PMI, January 2019.

[x] Source: Eurostat, as of 6/2/2019. Spain, real GDP growth rate, Q4 and Q3 2018, respectively.

[xi] Source: IHS Markit, as of 5/2/2019. Eurozone Composite PMI, January 2019.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today