Personal Wealth Management / Economics

Leading Indicators Point to Slowing US Inflation Ahead

Beyond American price measures themselves, signs of improvement in one of the global market’s big concerns abound.

Recent US inflation (rising prices economy-wide) reports have slowed some, and given America’s sizeable weight in world markets, we think they offer global investors a modicum of relief.[i] Yet many commentators we follow warn that high inflation won’t subside anytime soon, with October’s readings a false dawn.[ii] They say it is “too soon to celebrate” and argue the US Federal Reserve has more work to do.[iii] Perhaps. Monthly inflation data variability is unpredictable, in our experience. However, we see growing evidence inflation is likely to slow—and defang one of the global market’s biggest concerns this year.

From America’s headline consumer price index (CPI—a government-produced measure of goods and services prices across the economy) and its “core” CPI excluding food and energy to producer prices and import prices, US inflation has come off the boil since the summer.[iv] Yet commentators we read argue other measures—like the “sticky price” CPI (a gauge of less-volatile prices)—continue to rise.[v] Whilst we agree about not reading too much into short-term wiggles, we don’t think various inflation measures—or subsets of them—are any more telling than others. For example, our research shows producer prices don’t reliably lead CPI. We find they are coincident, rising and falling together. Instead of poring over backward-looking inflation data—past prices, which our research shows never predict—we think it is more helpful to take cues from forward-looking measures, which indicate inflation is likely to fade over the coming year.

Exhibits 1 through 3 show a few leading US inflation indicators. Now, as the charts also show, these aren’t super-precise gauges. Their lead times to American CPI can vary—sometimes by a lot. They probably won’t pinpoint inflation’s peak, but together, we think they give a good sense of US CPI’s likely general direction ahead.

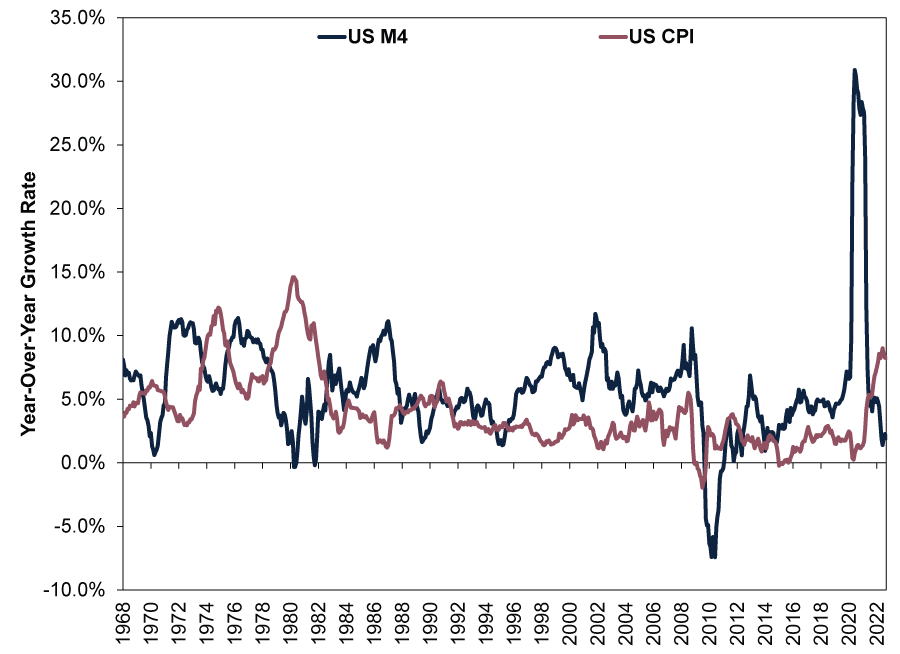

Let us start with money supply. Monetarist theory states inflation is always and everywhere a monetary phenomenon.[vi] So consider US M4, the broadest measure of America’s money supply, which includes highly liquid near-money substitutes like US Treasury bills.[vii] Whatever the accuracy of money supply measures, which seem somewhat questionable to us, the pattern is telling, in our view. M4 spiked above 30% y/y in June 2020. (Exhibit 1) Inflation began escalating about a year later as reopening commenced and demand surged, but M4 growth has since slowed dramatically. It crawled 1.9% y/y in September. We think less money sloshing around the system means fewer dollars chasing (up until recently) supply-constrained goods.

Exhibit 1: US Money Supply’s Decelerating Implies Inflation Will, Too

Source: Center for Financial Stability and US Federal Reserve Bank of St. Louis, as of 17/11/2022. US Divisia M4 (including US Treasurys), January 1968 – September 2022, and consumer price index (CPI), January 1968 – October 2022.

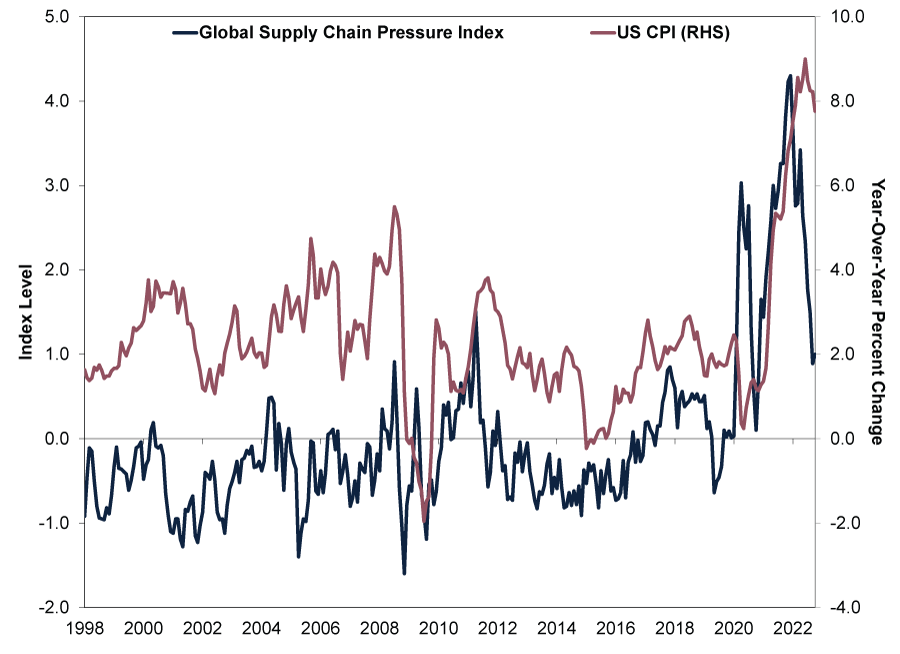

Supply chain issues have featured prominently in this year’s hot inflation, in our view, yet improvements are showing. We have featured the New York Federal Reserve branch’s Global Supply Chain Pressure Index (GSCPI) a couple times before as an indication price pressures are easing. The GSCPI has dropped from over 4.0 late last year to around 1.0 recently. (Exhibit 2) That still shows elevated pressure, but it has eased substantially from the peak.

Exhibit 2: Global Supply Chain Pressure Easing Helps Relieve Price Pain

Source: US Federal Reserve Banks of New York and St. Louis, as of 17/11/2022. Global Supply Chain Pressure Index and CPI, January 1998 – October 2022.

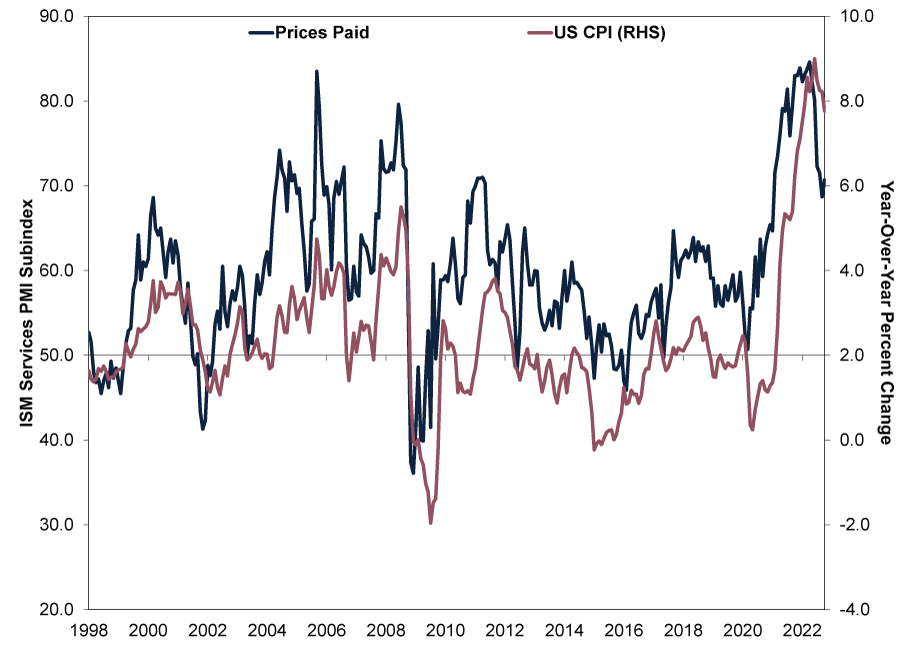

America’s Institute for Supply Management (ISM) purchasing managers’ index (PMI) prices paid component for the services sector offers a separate look at input prices for firms representing 71% of US gross domestic product (GDP, a government-produced measure of economic output).[viii] Around 70% of services firms surveyed in October said the prices they pay are rising—historically elevated, like the GSCPI—but that has come down from 9 straight months of readings above 80% through June. (Exhibit 3) Meanwhile, ISM’s sister manufacturing survey showed more respondents noted falling input prices than rising.[ix]

Exhibit 3: US Services Firms Are Also Seeing Slower Price Growth

Source: FactSet and US Federal Reserve Bank of St. Louis, as of 17/11/2022. ISM services Purchasing Managers’ Index (PMI) prices paid subindex and CPI, January 1998 – October 2022.

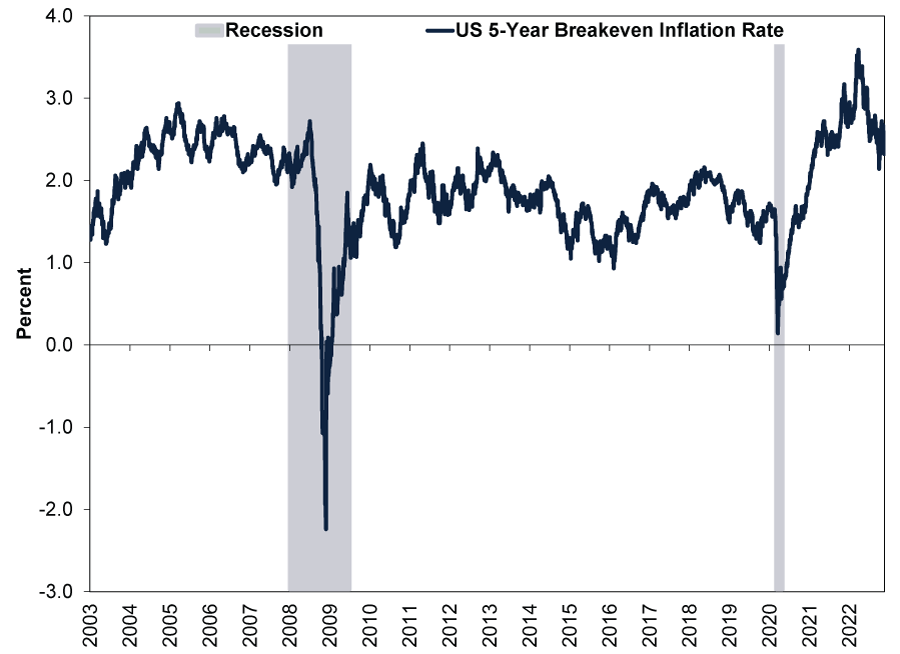

US bond markets appear to reflect likely easing inflation pressures, too. Exhibit 4 shows the average inflation rate over the next five years implied by the difference between 5-year Treasury and Treasury Inflation-Protected Securities (US Treasury securities whose interest payments are linked to inflation, similar to the UK’s index-linked Gilts) yields has fallen to 2.3% from a high of nearly 3.6% in March.

Exhibit 4: America’s Bond Market Reflects Moderating Inflation Ahead

Source: US Federal Reserve Bank of St. Louis, as of 17/11/2022. US 5-Year Breakeven Inflation Rate, 2/1/2003 – 16/11/2022. Recession shading based on US National Bureau of Economic Research (NBER) Business Cycle Dating Committee.

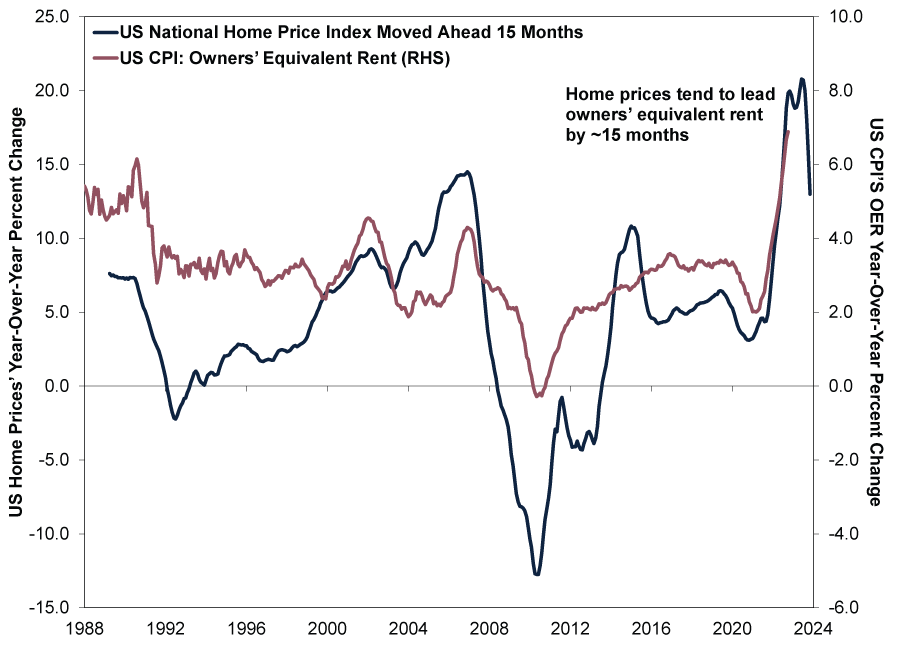

Meanwhile, the S&P/Case-Shiller US National Home Price Index has shown cooling prices for months now, and it typically leads shelter costs—among those “sticky” prices some warn are still rising.[x] As Exhibit 5 shows, American home prices tend to lead US CPI’s owners’ equivalent rent (OER) component—the single-largest CPI category at a nearly 25% weight—by around 15 months.[xi] Now, we think OER is a largely illusory line item in CPI, because it represents what homeowners would pay if they rented their house. The BLS imputes it from the relatively small sample size of single-family home occupants renting their primary residence.[xii] But regardless, actual US rental rates have decelerated to 4.7% y/y in October, down rapidly from January’s 17.4% peak, according to Realtor.com.[xiii]

Exhibit 5: Home Price Growth and Rental Rates Starting to Decelerate

Source: FactSet and US Federal Reserve Bank of St. Louis, as of 17/11/2022. S&P/Case-Shiller US National Home Price Index, January 1988 – August 2022, and US CPI: owners’ equivalent rent, January 1988 – October 2022. The Home Price Index is pulled 15 months forward for illustrative purposes.

Continually escalating grocery bills may also be in the rear view before too long. The UN Food and Agricultural Organization (FAO) Food Price Index—international prices for food commodities the FAO measures—has steadily slowed since spring. Food price inflation decelerated from 34% y/y in March (when Russia invaded Ukraine, both major agricultural exporters) to just 2% in October.[xiv] This may not yet show in falling prices people are paying, but we think it is an encouraging signal that upward pressure is abating.

In our view, inflation was a key factor in souring sentiment this year, hurting stocks. We don’t think inflation itself fundamentally caused 2022’s market ructions. After all, the US economy has (so far) avoided recession (broad economic contraction) despite widespread alarm—and an impending one in coming quarters isn’t assured.[xv] Meanwhile, corporate profit margins and investment have held up rather resiliently.[xvi] But now, signs of inflation pressure ebbing suggest to us that dour inflation sentiment may be overdone—bringing relief. It may not come in a straight line—few economic or market factors do. It may also take longer to show up in the UK, where higher imported commodity prices due to the weak pound and the energy price cap’s semi-annual reset add wild cards. But we think it does seem likely to come soon, almost no matter what mainly drove inflation this year.

[i] Source: US Bureau of Labor Statistics, as of 17/11/2022. Statement based on US consumer, producer and import price indexes, October 2022.

[ii] “Inflation Isn’t Dead Yet,” Editors, Bloomberg, 15/11/2022, accessed via Advisor Perspectives. “Wait, This Is The Inflation News Everyone Is Celebrating?” Editorial Board, Issues & Insights, 15/11/2022.

[iii] Ibid.

[iv] See note i.

[v] Source: US Federal Reserve Bank of St. Louis, as of 17/11/2022. Sticky Price Consumer Price Index less Food and Energy, October 2022. “Are Some Prices in the CPI More Forward Looking Than Others? We Think So.,” Michael F. Bryan and Brent H. Meyer, US Federal Reserve Bank of Cleveland, 19/5/2010. “Cleveland Fed: Median CPI Increased 0.5% and Trimmed-Mean CPI Increased 0.4% in October,” Bill McBride, Calculated Risk, 10/11/2022.

[vi] “Inflation: True and False,” David R. Henderson, Hoover Institution, 20/5/2021.

[vii] Source: Center for Financial Stability, as of 17/11/2022. Statement based on US Divisia M4 (including US Treasurys).

[viii] Source: US Bureau of Economic Analysis, as of 17/11/2022. Private services-producing industries percent of GDP, Q2 2022.

[ix] Source: FactSet, as of 17/11/2022. ISM manufacturing PMI prices paid subindex, October 2022.

[x] See notes ii and v.

[xi] Source: US Bureau of Labor Statistics, as of 17/11/2022. Relative Importance and Weight Information for the Consumer Price Indexes, December 2021.

[xii] “Measuring Price Change in the CPI: Rent and Rental Equivalence,” Staff, US Bureau of Labor Statistics, 29/3/2022.

[xiii] “October Rental Report: Rent Prices Fall for the Third Straight Month,” Jiayi Xu, Realtor.com, 17/11/2022.

[xiv] Source: FactSet, as of 17/11/2022. FAO Food Price Index, March 2022 – October 2022.

[xv] Source: NBER, as of 17/11/2022. Statement based on NBER’s Business Cycle Dating Committee.

[xvi] Source: FactSet and US Bureau of Economic Analysis, as of 17/11/2022. Statement based on S&P 500 profit margins and private non-residential fixed investment, Q3 2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Brazil Review & Outlook2026-06-04

-

Market Analysis Global Bond Calamity Calls for Calm Perspective2026-05-27

-

Economics A May Global Economic Check-In2026-05-26

-

Macro Insights Macro Insights Q2 20262026-05-22

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today