Personal Wealth Management / Economics

Rounding Up Major Global GDP Figures for Q1

What to make of some rather ugly results?

Japan reported Q1 gross domestic product (GDP, a government-produced estimate of economic output) on Monday, rounding out the preliminary results of COVID-19’s impact on major developed economies. As most financial commentators we follow anticipated, the Land of the Rising Sun joined Germany, France and Italy in recession (defined commonly as two consecutive quarters of falling GDP). At this juncture, investors might rationally seek to compare different nations’ results in search of insight, but national statistics agencies’ various reporting preferences may make doing so difficult. Hence, we have done the math to bring everything in line and show our analysis of what the results do—and don’t—mean for equities.

Under more typical circumstances, based on our long-running observation of economic reporting, the variance amongst countries’ GDP growth rates wouldn’t get a ton of scrutiny—just a quick Country A is growing faster than Country B. But in the COVID-19 era, financial commentators seem extremely motivated to calculate how the virus and the related stay-at-home orders are affecting the global economy, particularly with countries’ lockdowns (and re-openings) on differing timetables. Just looking at news coverage or national statistics bulletins probably won’t give you sufficient information, however, because countries use different reporting methods. The UK, eurozone and most of its member-states focus on year-over-year or quarter-over-quarter results. The former is the percentage change between GDP in a given quarter versus the same quarter in the prior year. The latter is the percentage between GDP in a given quarter and the preceding, usually with seasonal adjustments (meaning, extra calculations to account for holidays, weather and other recurring seasonal variables). The US and Japan report GDP growth at seasonally adjusted annualised rates, which is what you get if you extend the quarterly growth rate over a full year. So to enable a comparison, we made Exhibit 1, which displays seven major nations’ (plus the eurozone’s) annualised GDP growth rates over the past three quarters.

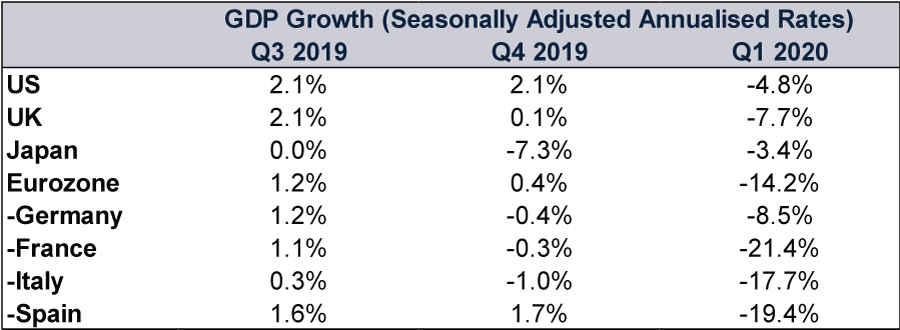

Exhibit 1: Annualised GDP Growth Rates

Source: FactSet and Destatis, as of 18/5/2020.

It might be tempting to look at this and make judgments about each country’s inherent strength and ability to weather the storm, but we don’t recommend going down that route. In our view, the staggered implementation of stay-at-home policies explains most of the difference. The eurozone’s lockdown started a couple of weeks before most US stay-at-home orders kicked in. The UK’s started around the same time as America’s, and household consumption in both nations took similar hits—the UK just didn’t get a boost from government spending and had a sharper contraction in exports.[i] As for Japan, its COVID restrictions were the last amongst major developed nations to take effect, and GDP fell from a lower base due to Q4’s sharp contraction, which the data suggest stemmed from October’s sales tax hike.[ii] So whilst the decline’s pace slowed and beat economists’ consensus expectations, we think it would be a mistake to portray Japan as improving and weathering COVID surprisingly well.[iii]

We think the only conclusion to draw from these data is perhaps the most obvious one: Restricting economic activity in hopes of slowing COVID’s spread caused economic activity to fall. The relatively worse results stemming from Continental Europe may hint at the extent to which Q2 data will worsen in the US and UK, but with both countries starting to reopen gradually, we wouldn’t overstate the predictive power. There are likely just too many moving parts, with too much country-specific nuance.

Therefore, from an investment standpoint, we think it is more meaningful to highlight what these data don’t tell us. One, whether good or bad, last quarter’s GDP numbers likely don’t dictate where equity markets will go from here. Our research shows equities generally move ahead of economic trends. This year, they fell before GDP (and earlier monthly data) did.[iv] Whenever the recovery begins (if it hasn’t already), we think it will likely do so before GDP improves—just as the 2007 – 2009 equity market downturn ended months before its accompanying recession ceased.[v] Two, GDP leaders and laggards don’t necessarily translate to leaders and laggards from a national equity market return standpoint. In our view, equities move most on the gap between reality and expectations, and GDP isn’t the only variable affecting either. The sectors and industries composing each country’s equity market matter a lot, in our view, as does and general investor sentiment. In other words, we don’t see Q1’s GDP results as a valid argument to overweight Japan. They are likely just one more piece of evidence showing this economic contraction is bad.

They probably won’t be the last evidence of this, either. But with abundant chatter in the press already swirling about how bad Q2 GDP will be and many commentators we follow already starting to dismiss an eventual recovery as a meaningless jump off a low base, potential negative surprise power seems to us to be falling by the day.

[i] Source: FactSet, as of 18/5/2020.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid. Statement based on MSCI World Index returns with net dividends.

[v] Ibid. Statement based on MSCI World Index returns with net dividends.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Economics Pain at the Petrol Station Won’t Hurt the Global Economy2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Market Analysis February’s Growthy Data—and the Iran War’s Souring Sentiment2026-03-06

-

Market Analysis Putting the Latest Private Credit Implosion in Perspective2026-03-06

Contact Us

Learn why 195,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/12/2025. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today