Personal Wealth Management / Market Analysis

Russian Default’s Financial Fallout Likely Limited

Some form of Russian sovereign bond default is looking rather likely, but the implications seem considerably smaller to us than 1998’s, which played a central role in that year’s volatility.

Commentators we follow continue to track the horrific war in Ukraine this week. But amongst them, a related factor is also gaining prominence: Chatter over a Russian sovereign bond default is rising after the country failed to complete an interest payment to foreign holders of Russian bonds last Wednesday.[i] The miss starts the clock ticking on a 30-day grace period.[ii] If that expires and bondholders don’t receive their money, it will be in technical default.[iii] Although this prospect seems to be stirring some warnings amongst commentators we follow—and memories of 1998’s Russian default, part of a larger Emerging Markets (EM) debt crisis—we don’t think a chain reaction is likely to stem from this.

Interestingly to us, reports we saw suggested Russia’s debt service failure appeared to be mutual at first blush. Whilst Russia’s Ministry of Finance sent coupon payments to foreign holders of rouble-denominated sovereign debt—known as OFZs (the Russian abbreviation for Federal Loan Obligations)—the Central Bank of Russia (CBR) halted Russia’s National Settlement Depository from making payments to foreign clients.[iv] Russian President Vladimir Putin overruled this policy on Monday, stating that he would permit the payments to go through—even to creditors in nations he considers hostile.[v] However, another issue remains: Western clearing systems used to settle these payments stopped accepting them due to sanctions.[vi]

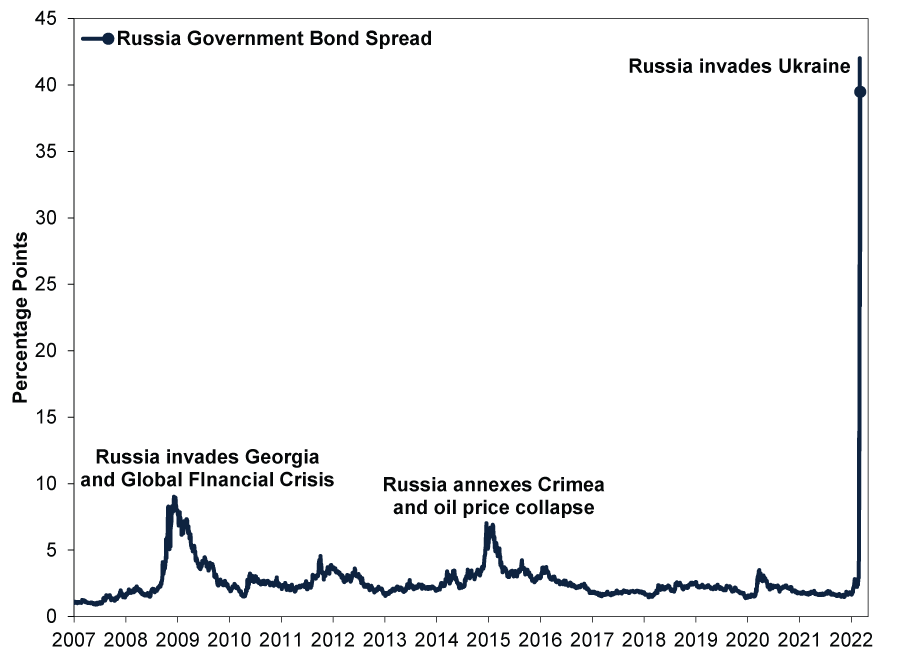

Whilst such a default is unusual, in our view—Russia has plenty of roubles in its coffers to pay if allowed—it doesn’t change the effect on bondholders.[vii] We think foreign investors in Russian OFZs could face substantial losses, if not complete write-offs—on top of the huge rouble depreciation they have already felt. The same fate could await foreign holders of dollar- and euro-denominated Russian debt, too. Payments on such bonds are scheduled for 16 March, and markets reflect a high likelihood they will go unpaid as the difference in yields between Russian bonds and US Treasurys soars.[viii] (Exhibit 1)

Exhibit 1: Markets Have Priced Russian Default

Source: FactSet, as of 7/3/2022. JP Morgan Emerging Markets Bond Index (EMBI) Global Russia credit spread, 1/1/2007 – 4/3/2022. The spread measures the index’s yield over equivalent-maturity US Treasury bonds’.

The fallout from potential Russian default looks limited to us. At 2021’s end, foreigners held only $20 billion (£15.25 billion) in foreign currency (mostly dollar and euro) sovereign debt and $41 billion (£31.26 billion) in rouble debt—now hugely depreciated.[ix] For comparison, the US Treasury sold $50 billion (£38.12 billion) in debt last month alone and plans to auction $48 billion (£36.61 billion) more this month.[x] Global sovereign debt and currency markets trade in the trillions daily.[xi] We think Russian exposure, whilst not nothing, is a drop in the bucket.

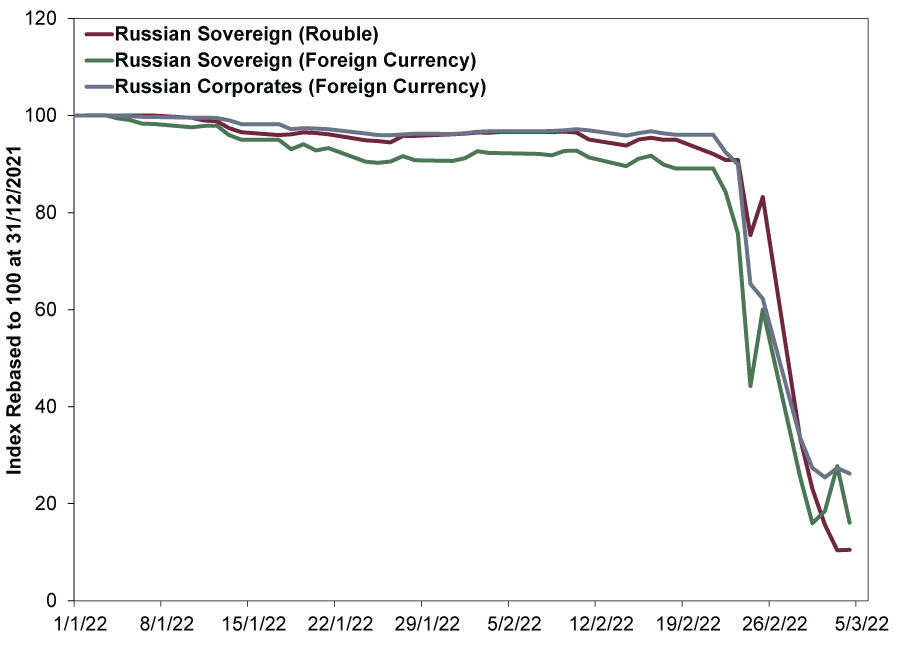

Foreign exposure to Russian corporate debt is a bit bigger, at around $75 billion (£57.23 billion) as of last September.[xii] But debt here looks more serviceable, in our view. Most of it was issued outside of Russia, and Russian corporations have dollar and euro bank deposits abroad to fund debt payments—they have the ability to pay.[xiii] We think the question is whether they will be allowed to, which remains a grey area. But Russian foreign currency corporate bonds are already selling at steep discounts—about 70% below face value.[xiv] The risk of non-payment to us looks priced in to a very great extent. (Exhibit 2)

Exhibit 2: Russian Debt Selling at Steep Discounts

Source: FactSet, as of 7/3/2022. JP Morgan EMBI Global Russia Indexes (local and foreign currency) and JP Morgan Corporate EMBI Russia Index total returns, 31/12/2021 – 4/3/2022.

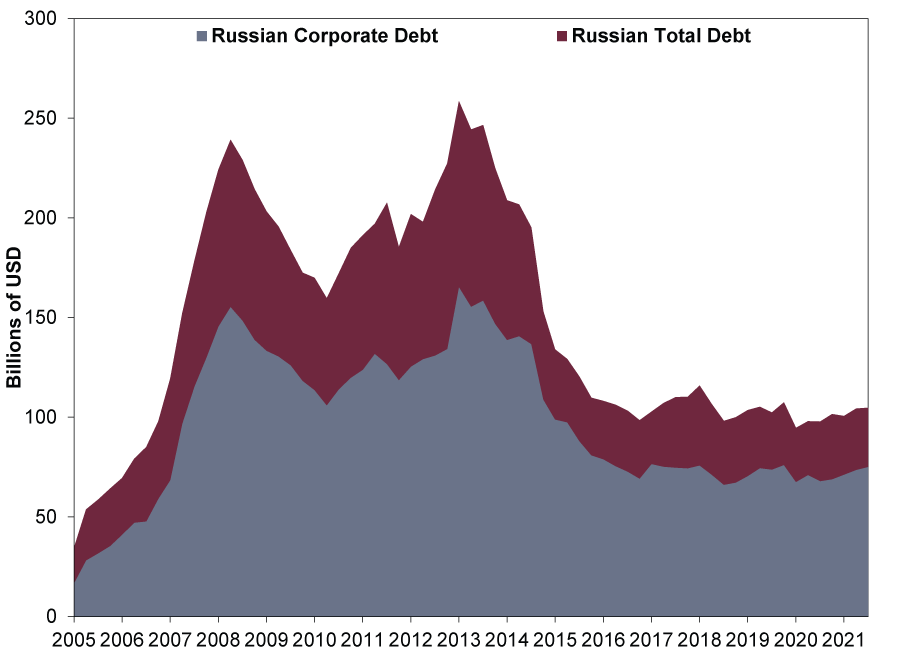

The lack of surprise at this point is a big reason we don’t think there are any noteworthy contagion effects from Russian default. In our view, sanctions stemming from its 2014 annexation of Crimea—and, apparently, in preparation for its invasion of Ukraine—mitigated the global effect. (Exhibit 3)

Exhibit 3: Foreign Banks Reduced Exposure to Russian Debt

Source: Bank for International Settlements, as of 7/3/2022. Foreign bank ownership of Russian debt securities (corporate and total), Q1 2005 – Q3 2021.

As for the rest of EM debt markets, our research shows their past vulnerabilities were mostly related to servicing foreign currency debt whilst maintaining fixed exchange rates they couldn’t defend. Today is light years different based on our analysis: Currency pegs are almost entirely gone now, and most issuing EM countries (as Russia was formerly)[xv] have amassed large reserves to back their debt. Besides, we don’t think the causal factors underpinning Russia’s default risk rising—starting a brutal war that is driving financial market restrictions—apply to any nation other than Russia and Belarus.

Russia may have a big geopolitical footprint, but in our view, its economy—and financial system—is far smaller and not critical to global markets, energy aside. Even if Russia doesn’t default, we think Putin’s decision to invade Ukraine is virtually assured to make Russia’s economic role far, far smaller for many years to come.

Hat Tip: Research Analysts Scott O’Leary, Delo Baker and Ori Powers

[i] “Russia Likely to Miss Interest Payment for First Time Since 1998 Crisis,” Anna Hirtenstein and Caitlin Ostroff, The Wall Street Journal, 3/3/2022. Accessed via The Wall Street Journal’s Live Coverage Feed for Russia’s invasion of Ukraine.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid.

[v] “Putin’s Ruble Workaround Still Leaves Bond Payments in Doubt,” Irene García Pérez, Bloomberg, 6/3/2022. Accessed via Yahoo!

[vi] See note i.

[vii] Source: FactSet, as of 7/3/2021. Statement based on Russian government external debt and foreign exchange reserves, 31/12/2021.

[viii] “Analysis: Ukraine War Raises Spectre of Russia’s First External Debt Default,” Karin Strohecker, Reuters, 2/3/2022. Accessed via Yahoo!

[ix] “Investors Struggle to Trade Russian Assets as Sanctions Hit Market Plumbing,” Philip Stafford and Tommy Stubbington, Financial Times, 1/3/2022. Accessed via Twitter.

[x] “Treasury Announces Details of Auctions of 3-Year, 10-Year Notes & 30-Year Bonds,” Staff, RTTNews, 3/3/2022.

[xi] Source: Securities Industry and Financial Markets Association and Bank for International Settlements, as of 4/3/2022.

[xii] Source: Bank for International Settlements, as of 30/9/2021.

[xiii] “Bondholders Say Russia’s Yandex Has Paid Coupon on Dollar Debt,” Irene García Pérez, Giulia Morpurgo and Abhinav Ramnarayan, Reuters, 3/3/2022. Accessed via Yahoo!

[xiv] See note viii.

[xv] MSCI reclassified Russia from EM to standalone markets status last Wednesday after deeming it uninvestable. “From Crisis to Crisis: Russia’s Diminished Role in Emerging Markets,” Peter Zangari, MSCI, 3/3/2022.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Macro Insights Q2 20262026-05-18

-

Politics A Market-Orientated Perspective on the UK’s Political Ructions and Q1 Economic Results2026-05-15

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today