Personal Wealth Management / Politics

Scotland’s Election and the ‘Risk’ of IndyRef2

A second Scottish independence referendum isn’t a given, but either way, we think the impact on UK shares is likely limited.

Editors’ Note: As always, our political commentary is non-partisan by design. We favour no politician, political party nor any given outcome in a political referendum and assess political developments solely for their potential economic or market impact.

Scotland holds elections on 6 May, and with the Scottish National Party (SNP) polling well despite a scandal embroiling its current and former leaders, independence chatter is once again running hot amongst politicians and news commentators we follow.[i] The SNP is reportedly planning to table legislation laying the groundwork for an independence referendum before the election even takes place, suggesting tough rhetoric may dominate the campaign—and driving uncertainty for financial markets afterward if the SNP wins an outright majority.[ii] In our view, it is far too early to assess the probable election results. But even if another independence push gets going, we think it is likely to have only a limited impact on UK equities.

Even if the SNP wins an outright majority, holding a second independence referendum is likely easier said than done. Per the Scotland Act of 1998, all matters concerning the union must go through Westminster. That means the UK government must approve a request from Scotland to allow it to vote on holding a referendum. Prime Minister Boris Johnson hasn’t tipped his hand on this recently, instead suggesting in a recent speech that keeping an SNP majority out of Holyrood is the only way to prevent second vote.[iii] Guessing at politicians’ motives is always a treacherous task, but we wouldn’t be surprised if this were an exaggeration to motivate pro-union Scots to turn out in May. On past occasions, he has espoused the view that 2014’s vote was a once-in-a-generation event. Again, though, we don’t think it is possible to determine probabilities one way or the other.

In theory, Scotland could try to hold a referendum without Westminster’s support, allowing the UK Supreme Court to review the case in hopes of a favorable ruling. Some politicians have suggested this alternative, but Catalonia tried this in 2017 and it didn’t go well, which we think may discourage SNP leadership. In October 2017, pro-independence Catalan leaders held an independence referendum despite the Spanish government declaring it illegal. The referendum passed, 90% to 10%, but voter turnout was very low due to opposition boycotts and police intervention. The Federal government deemed the results illegitimate, leading to the arrest and jailing of many pro-independence leaders. Importantly, EU leaders also declared the referendum illegitimate, deferring to the Spanish government and constitution to resolve the matter.

We think it is reasonable to think the EU would likely react similarly to a Scottish independence referendum that lacks legal or UK government support. That is no small matter. Though the SNP wants independence, it likely wants world governments—particularly the EU—to view it as legitimate, considering part of the motive here is re-entering the bloc. As a result, we think independence options are limited and the process is unlikely to play out quickly given the nature of legal challenges.

Whilst the prospect of a second referendum may create some uncertainty, the long road ahead likely limits its surprise power over shares. Cloudy sentiment may dampen UK returns if the door to a referendum cracks open, but we think the bigger headwind to the country’s equity performance is stylistic.

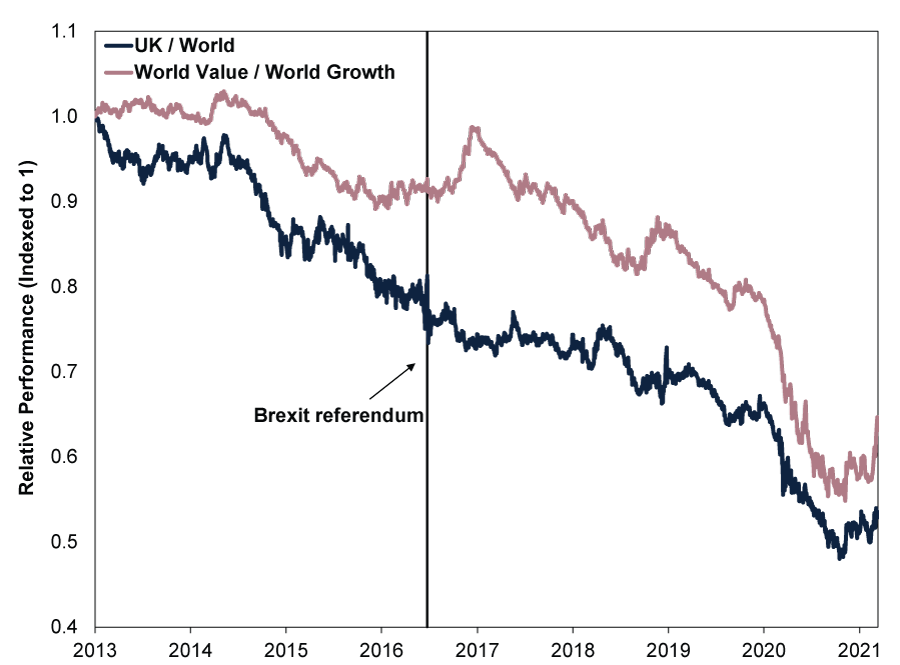

To see this, we think it is helpful to look at US shares surrounding 2014’s referendum. Whilst they underperformed global shares as 2014’s referendum approached (Exhibit 1), it is difficult to parse out how much—if any—was tied to referendum uncertainty. As the blue line indicates, the UK was underperforming back in 2013 and continued doing so well after the vote, despite uncertainty falling. A big reason for this, in our view, is the UK’s heavy tilt to value shares—particularly Financials and Energy. (Value-orientated companies tend to carry relatively lower price-to-earnings ratios and more debt, making them more sensitive to economic conditions, and they tend to return more money to shareholders via dividends and share buybacks and invest less in growth-orientated endeavours.) These sectors were 37% of UK market capitalisation entering 2014, and they lagged badly worldwide.[iv] Today, these two sectors still have an outsized footprint in British markets, with Financials and Energy comprising 19.6% and 10.4% of market capitalisation, respectively.[v] Both far exceed the world’s 13.6% and 3.2%.[vi]

This largely explains why UK relative returns have largely mirrored value’s returns relative to growth over the past several years, in our view. As long as Tech and growth shares are leading worldwide, the UK—which has barely any Tech—likely lags global markets even if referendum uncertainty evaporates in seven weeks. (Growth-orientated companies generally have higher valuation metrics like price-to-earnings ratios and focus on re-investing profits into the core business to expand over time, making their profits relatively less sensitive to economic ups and downs.)

Exhibit 1: MSCI UK Relative Performance Tends to Track Value’s Performance versus Growth

Source: Factset, as of 10/3/2021. MSCI United Kingdom Index, MSCI World Index, MSCI World Value Index and MSCI World Growth Index, 3/12/2012 – 10/3/2021. Indexed to 1 at 31/12/2012. UK and value shares are rising when the blue and mauve lines, respectively, are rising.

[i] Source: Politico, as of 17/3/2021.

[ii] Source: BBC News, as of 17/3/2021.

[iii] Source: The Scotsman, as of 17/3/2021.

[iv] Source: FactSet, as of 3/17/2021. MSCI UK Index Financials and Energy sector weights, 12/31/2013.

[v] Source: FactSet, as of 3/16/2021. MSCI UK Index Financials and Energy sector weights, 2/28/2021.

[vi] Source: FactSet, as of 3/16/2021. MSCI World Index Financials and Energy sector weights, 2/28/2021.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-07

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today