Personal Wealth Management / Financial Planning

Some Basics to Guard Against Hucksters and Financial Thieves

Big volatility could be sowing the seeds of the next big investment-related Ponzi scheme. Here are some tips to help protect yourself.

As investors deal with the challenges of a bear market (a long, fundamentally driven equity market decline of -20% or worse)—already a difficult prospect—we think they must also be on guard against another threat. This one comes from their fellow humans, unfortunately. The Pensions Regulator (TPR) recently warned savers they face higher risk of exploitation by scammers during this crisis.[i] Whilst fraudsters are always active, in our experience, we have found many of their plots come to light and make headlines during bear markets—like Bernie Madoff’s famous 2008 scam, which emerged only after the big bear market led many of his clients to seek withdrawals. Upon demanding their funds, they discovered their money was gone—stolen. But sharp volatility can also sow the seeds of future schemes, as we have observed many investors’ frazzled nerves have them clamouring for supposedly “safe” investments with good returns and no downside. With that in mind, we think investors would benefit from an explanation of how these plots generally look—and how to help guard against them.

When equity investors endure a large portfolio decline, in our experience, it often tends to weigh on their emotions. Seeing a large portion of one’s retirement savings vanish can heighten the appeal of an investment that seems “safe” and steady—a way to earn equity-like returns with less, or no, downside risk. Yet this is a fantasy. No financial product can provide returns approaching equities’ historical long-term returns without risk, in our view.

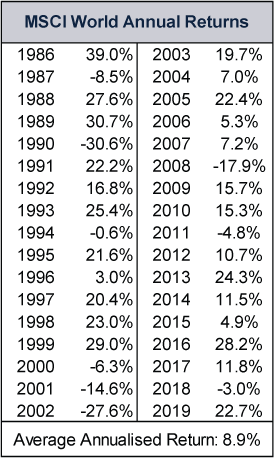

Ken Fisher, the founder of Fisher Investments UK, studied financial fraud schemes extensively for his 2009 book, How to Smell a Rat. In his research, he found many scammers would pitch fancy strategies and tactics featuring relatively high upside and, critically, no downside. Consider: Since 1985, the MSCI World Index’s average annualised return (meaning, the cumulative return transformed into a compound annual growth rate) is 8.9%.[ii] Hypothetically, a fraudster may say their product delivers a return that is modestly under that average, but, temptingly, without any of the associated negative volatility.

In our view, it is similar to how some sellers pitched mini-bonds to UK investors in recent years, based on the financial news coverage we followed. These are corporate debt securities issued directly from the company to the public, and they are not traded on public exchanges. The Belfast Telegraph describes them as “IOUs issued by a company to investors. The company will promise a fixed interest rate on the investor’s money, and will repay the loan at the end of a fixed period.”[iii] They advertised steady yields far above UK gilt yields and savings rates, and investors told reporters the risk of loss was minimised. But when some of these companies collapsed, people lost their entire investment. The collapse of London Capital & Finance in 2019 is one high-profile example, and the Financial Conduct Authority stated it found “evidence of a growing incidence of promotions which are frauds or scams.”[iv] In our view, the emphasis on high, steady returns and minimisation of the risk of loss was a key tell.

Alternatively, we have seen scammers claim their strategy combines a proprietary process with “alternative investments” nobody else is using—allowing them to remove the downside risk. Madoff famously described his approach as a “split/strike conversion” strategy, for example, which involved buying and selling options (contracts to buy or sell shares for a given price at a later date) on a portfolio’s share holdings—and claimed it drove high and consistently positive returns. Illuminatingly, nobody could replicate his results, which is probably because they weren’t possible. His strategy was sheer nonsense wrapped in impenetrable technical jargon.

As the old saw goes, if it sounds too good to be true, it likely is. Equities have high long-term returns, but the price tag for those returns is the risk of loss. A look back at the past 34 years for the MSCI World Index illustrates how returns fluctuate on a year-to-year basis.

Exhibit 1: MSCI World Annual Returns, 1986 – 2019

Source: FactSet, as of 1/4/2020. MSCI World Index annual returns with net dividends, 31/12/1985 – 31/12/2019.

Even during bull markets (long periods of generally rising equity markets), annual returns may be below average or negative periodically, as in 2011 and 2018. Moreover, significant volatility or price swings happen during great years. If someone is pitching you a strategy offering returns anywhere near equities’ long-term average with little to no downside risk, we think you should be extremely sceptical.

If confronted with a seemingly appealing offer, here are what we consider some helpful things to look for. First, seek out the bad years. Are returns eerily consistent and only positive? We think that should raise some eyebrows. Financial news coverage of the investment fund industry shows even the best managers will have some poor years, whether due to the environment (e.g., a bear market) or a portfolio decision that didn’t work out. If they don’t have any bad stretches, press them to explain why. How did they generate those remarkably smooth, positive returns during times when most markets were down?

Second, ask them to explain their strategy in simple, plain language. Our research shows an inability to explain financial jargon is another red flag. If it isn’t an attempt to obfuscate and confuse, it may also reveal ignorance—not a great trait, either, in our view. This is doubly true if the returns are smooth and strong. If someone has achieved remarkable investment results, they should have a plain English explanation for how they did so that doesn’t leave you confused.

Another consideration to be mindful of, according to our research: Many fraudsters exploit their personal networks and communities, effectively using a tactic known as “affinity marketing” to find targets. In these cases, the bad actor runs in the same social circles as you, a friend or a family member. Maybe they attend your religious congregation. Or perhaps they belong to the same community group or ethnic organisation or share some other common association that provides an easy path to build trust. Access and personal connection can build a false sense of security. For example, Madoff used his high-profile status in the Jewish community to take advantage of investors. Announcements from America’s Securities and Exchange Commission show many similar, if small-scale, plots uncovered every year that hinge on these kinds of relationships. Just because someone’s office is a 10-minute drive from your house or you see them every week at community gatherings doesn’t mean you shouldn’t do rigorous due diligence on any plan they are presenting you.

We understand the appeal of something that seems “safe” during sharp, painful volatility. But without doing proper due diligence, you risk losses of a different kind—ones that could be permanent.

[i] “Scams Warning for Pension Savers Worried About Impact of Coronavirus on Finances,” Press Association, 31 March 2020.

[ii] Source: FactSet, as of 1/4/2020. MSCI World Index annualised return with net dividends, 31/12/1985 – 31/12/2019.

[iii] “FCA Bans Mini-Bond Promotions After London Capital & Finance Scandal,” August Graham, Belfast Telegraph, 29 November 2019.

[iv] Ibid.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today