Personal Wealth Management / Politics

Sunset on Reform Hopes in Japan?

In our view, Japan’s new prime minister likely extends the status quo for equity markets’ political drivers.

Editors’ Note: MarketMinder Europe is politically agnostic. We favour no politician nor any party and assess political developments for their potential economic and market impact only.

Japan officially has a new prime minister (PM) in waiting, and it is … not the person most observers we follow expected. Heading into yesterday’s Liberal Democratic Party (LDP) leadership vote, reform minister Taro Kono was reportedly the apparent favoruite, but former LDP Research Council chair Fumio Kishida pulled off an upset with unexpectedly strong support from LDP lawmakers.[i] Presuming he wins a confidence vote in Japan’s parliament (known as the Diet) on 4 October—seemingly a foregone conclusion, considering the governing coalition’s supermajority—he will become the next PM. Japanese shares fell sharply on Wednesday, dipping -1.1% on the day, perhaps partly due to this news.[ii] We wouldn’t be surprised if Japanese shares trail the MSCI World Index over the foreseeable future, either. To us, investors seemed to get too far out over their skis on economic reform hopes when Kono looked like the heir apparent. But now it is Kishida, and reality is seemingly setting in.

When former PM Yoshihide Suga announced on 3 September that he wouldn’t seek re-election as LDP chief in yesterday’s election, commentators we follow swiftly identified Kono as the likely successor. Whilst equity markets in the rest of the world hit a speedbump, Japanese markets rallied, seemingly on the prospects of change, in our view.[iii] When Suga became PM, commentators we follow described him as a proverbial safe pair of hands—a name well known in Japan and a PM who would focus on shepherding the country through COVID rather than rock the boat with reforms that might be unpopular in some corners. In most developed countries, we think that sort of political gridlock and status quo is generally positive for equity markets, as reforms frequently create winners and losers. But according to our and many other analysts’ research, Japan remains plagued by a number of structural issues that stifle competition amongst companies and domestic demand, including a strict labour code and complex web of cross-shareholdings amongst the major conglomerates. (Meaning, companies form alliances and prevent hostile takeovers by owning large stakes in each other, which—in our view—can reduce board members’ incentives to pursue measures that might foster competition) Throughout Japan’s postwar history, our research shows this system has kept bloated, underperforming companies afloat and stifled competition from new challengers. In our view, is a big reason for the country’s famously weak economy in the 1990s and 2000s.

None of the commentators we follow portrayed Suga as likely to act on any of this, especially as successive COVID lockdowns, a controversial Olympic games and Japan’s delayed vaccine rollout sapped his political capital. But when he stepped aside and Kono took centre stage, sentiment flipped fast. Kono was popular. He championed reforms. He seemingly had the clout and charisma of former PMs Junichiro Koizumi and Shinzo Abe, the only recent Japanese PMs that pulled off some reforms (and had any staying power in office in recent years). Seemingly anticipating his victory and a raft of pro-market changes, Japanese shares jumped 7.5% in the 11 trading days after Suga’s announcement, making up much of their year-to-date lag versus global markets.[iv] Commentators we follow forecast even stronger returns over the foreseeable future, pointing to rising inbound investments from international investors and reform rumours.[v]

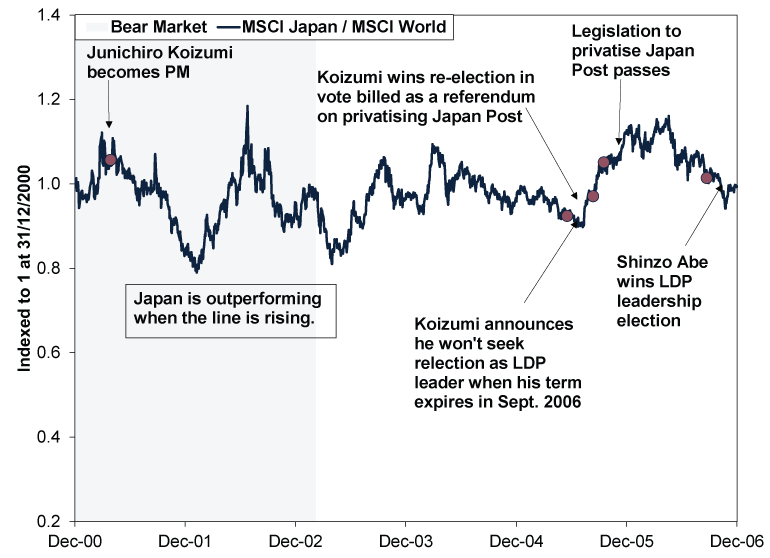

In our view, this rally likely would have proved irrational whether or not Kono won. In our many years covering Japanese politics, we think commentators have long gotten too starry-eyed over potential reformers, underestimating what our research has found to be the deep resistance to change. We have long observed LDP’s powerful rural wing, for example, counterbalancing leadership’s free-trade stance. The labour code and culture of lifetime employment have long appeared to be a political third rail. Even Abe and Koizumi, who did pass some significant measures, encountered opposition and left some areas undone. For example, Koizumi’s government did enact policies to help shore up Japan’s banking system in the early 2000s. These measures addressing the legions of so-called zombie banks that had dogged the country’s economy since the Nikkei bubble burst in the late 1980s. (A zombie bank is a bank that is technically insolvent—meaning its liabilities exceed its assets—but continues operating via support from the government or monetary policy officials.) But the effort to privatise Japan Post, the large government-run bank/postal service hybrid, which we think was beneficial for Japan’s financial system, monopolised the rest of his term, leaving other issues by the wayside. As Exhibit 1 shows, over his entire term, Japanese shares performed roughly in line with global equity markets, as spells of leading and lagging canceled each other out.

Exhibit 1: Japanese Shares Didn’t Excel Under Koizumi

Source: FactSet, as of 30/9/2021. MSCI Japan and MSCI World Index returns with net dividends, 31/12/2000 – 31/12/2006. A bear market is a broad, lasting equity market decline of -20% or worse with an identifiable fundamental cause.

When Abe succeeded Koizumi after the latter termed out as LDP leader in September 2006, commentators maintained high hopes for reform. The privatisation of Japan Post was in progress, and Abe, reportedly Koizumi’s hand-picked successor, espoused a similar reform agenda. Or so many observers thought. In reality, his primary focus seemed to us to be amending Japan’s Constitution to remove the anti-war clause and restore the country’s military might. That hogged most of his government’s attention until he stepped down for health reasons a year later. But in late 2012, he mounted a comeback, reviving reform hopes. When he returned as PM late December 2012, the LDP and its coalition partner, the New Komeito party, had a supermajority in the lower house—theoretically giving him the clout to pull off what Koizumi couldn’t.

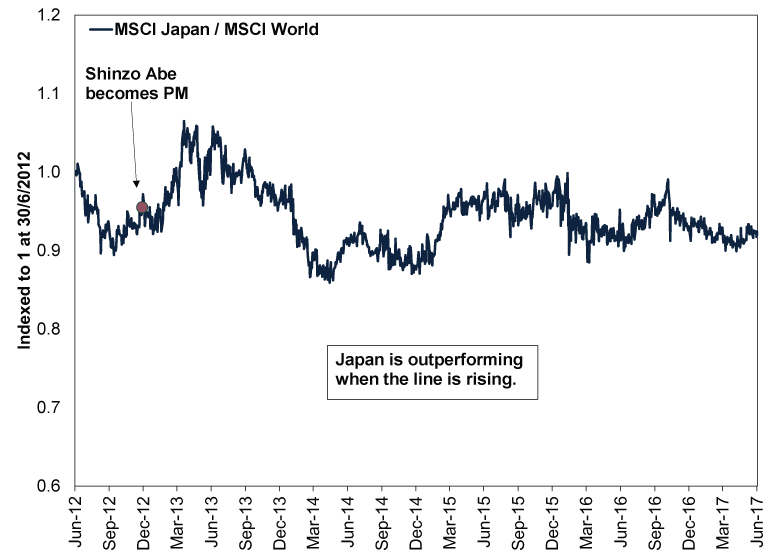

As Exhibit 2 shows, Japanese shares rallied on high hopes as Abe’s Abenomics agenda topped headlines globally we reviewed with its three arrows of monetary stimulus, fiscal stimulus and economic reforms. Abe even had a few legislative successes on the latter front, including a handful of free-trade agreements and significant corporate tax cuts. But reforms eventually took a back seat as constitutional change returned to the fore, again draining the government’s attention and political capital. After outperforming global equity markets significantly during Abe’s honeymoon period, Japanese shares soon paralleled investors’ dashed hopes. By 2014, they were underperforming cumulatively since Abe’s election, and they would keep doing so over the rest of his long tenure.[vi]

Exhibit 2: Abe’s Honeymoon Period Was Short

Source: FactSet, as of 30/9/2021. MSCI Japan and MSCI World Index returns with net dividends, 30/6/2012 – 30/6/2017.

When Suga announced he would step down, we asked readers a simple question: What was the likelihood Kono (or whoever) could pull off major changes that Abe and Koizumi couldn’t? Our answer, in a nutshell, was low. This isn’t a we told you so, mind you, but a reminder to think critically and not get taken in by headline hype, lest you chase heat and get burned. Had Kono won, we think there was a risk Japan would outperform for a while longer as irrational hopes inflated, but the likelihood relative returns followed their general path under Abe—and faltered as reform hopes faded—seemed high to us.

As for what comes next, many commentators we follow portrayed Kishida as the status-quo candidate during the LDP leadership contest. He championed big fiscal stimulus, rather than reform. Whilst many commentators cheer fiscal stimulus as a potential economic and market positive, multiple administrations have thrown stimulus at Japan’s economy during this millennium, and our research indicates there wasn’t much to show for it. The result is public spending and investment representing an outsized share of GDP relative to the US and elsewhere—not a dynamite economy.[vii]

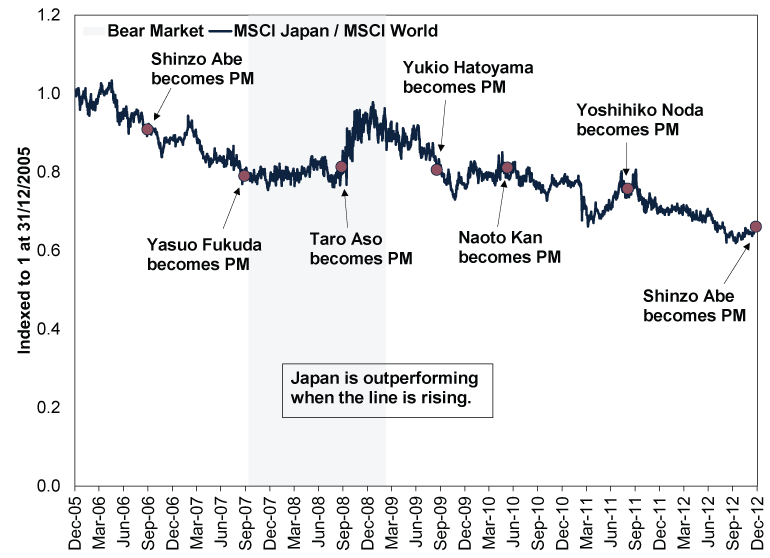

More broadly, it looks to us like Japan’s infamous revolving door of PMs may be back. Not because of anything unique to Kishida, but because that has been the 21st century norm when Japan selects a status quo-type candidate that churns out of the country’s political machine. Between Koizumi and Abe’s second turn at the wheel, Japan had six PMs in six years. As Exhibit 3 shows, during this stretch, the only notable burst of outperformance happened during the global financial crisis, when Japanese shares fulfilled what our research indicates is their traditional, defensive role (we think defensive shares tend to fare better during downturns because of relatively consistent demand). Otherwise and overall, the revolving door did not coincide with world-beating equity returns.

Exhibit 3: The Revolving Door Didn’t Make Japanese Shares Soar

Source: FactSet, as of 30/9/2021. MSCI Japan and MSCI World Index returns with net dividends, 31/12/2005 – 31/12/2012.

Therefore, we think it is most beneficial for investors seeking long-term growth in globally diversified portfolios to view Japan as we long have: a place where big multinationals are likely to outperform domestically orientated companies that would likely benefit most from reforms. In that regard, we think Japanese shares have plenty to offer from a diversification standpoint, but we don’t think the country is likely to be beneficial as the centrepiece of a global portfolio for now.

[i] “Kishida Elected as LDP President, Set to Become Japan’s New PM,” Staff, The Yomiuri Shimbun, 29/9/2021.

[ii] Source: FactSet, as of 30/9/2021. MSCI Japan Index return in GBP with net dividends on 29/9/2021.

[iii] Ibid. Statement refers to MSCI Japan and MSCI World Index returns in GBP with net dividends.

[iv] Ibid. MSCI Japan Index returns in GBP with net dividends, 2/9/2021 – 20/9/2021. Statement also refers to MSCI Japan and MSCI World Index returns in GBP with net dividends.

[v] “Foreigners Net Buyers of Japan Stocks for Fourth Straight Week,” Staff, Reuters, 27/9/2021.

[vi] See Note iii.

[vii] Source: FactSet, as of 29/9/2021. Statement based on government spending and investment as a percentage of 2019 gross domestic product in the US, UK, Germany and Japan. Gross domestic product is a government-produced measure of economic output.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-24

-

Market Analysis Reviewing America’s Q1 Earnings and What Q2 Expectations Say2026-06-23

-

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-23

-

Macro Insights SpaceX IPO and Rising Equity Supply2026-06-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today