Personal Wealth Management / Politics

‘Super’ Mario’s New Government Doesn’t Look Super Active

The more Italian prime ministers change, the more gridlock remains the same.

Editor’s Note: MarketMinder favours no political party nor any politician and our commentary aims to be nonpartisan. We assess developments solely for how they may impact equity markets.

Italy’s new government has been in office for only one week, but many financial commentators we follow are getting optimistic about what the new regime could accomplish. A little over a month after former Prime Minister Matteo Renzi and his small Italia Viva party withdrew from Italy’s multiparty coalition—leading to that coalition’s eventual dissolution—uncertainty over the shape of the country’s government has fallen. Former ECB head Mario Draghi—aka, Super Mario in honour of the iconic Nintendo character—is now Italy’s prime minister, charged with deploying EU coronavirus aid and leading a unity government comprised of virtually every major party in Italian politics. But while uncertainty is down and Draghi may have success in deploying EU aid, we think the government’s structure suggests Italian politics are as gridlocked as ever, which we think highlights the importance of keeping measured expectations. Whether you are bullish or bearish on the idea of a much-heralded central banker leading the country, don’t overrate Draghi’s ability to enact big reforms and change—which should be fine for equities, in our view.

Draghi’s victories in twin confidence votes—first last Wednesday’s 262 – 40 in the Senate, then the 535 – 56 win in the Chamber of Deputies last Thursday—were decisive. He now heads a broad-based government with the support of the Five-Star Movement, Lega, Democratic Party, Forza Italia and Renzi’s Italia Viva. Ministerial posts will be divided amongst these supporters, with a few going to non-partisan technocrats (meaning, appointees who don’t currently sit in Parliament but have technical expertise). As for the opposition, it chiefly comprises the far-right Brothers of Italy, who have voiced objection to Draghi’s staunchly pro-EU line. They were joined by a group from the Five-Star Movement—a group the party now says it will eject, so we figure it stands to reason that Italy will probably have a new political party in Parliament soon. Regardless, though, Draghi’s new government has broad support at its dawn.

The new government’s chief task is determining how to spend €209 billion (£182 billion) in EU coronavirus aid. Most plans we have seen loosely target aiding the tourism industry and health service in the near term, with green infrastructure, education and transportation spending getting larger, if longer-term, allocations. Disagreements over how to dole this money out were reportedly the proximate cause of the prior Prime Minister Giuseppe Conte government’s collapse. Now Italy ostensibly has until 30 April to present the EU with its plan, although we will note that EU politicians have a long history of moving self-imposed deadlines. Regardless, we think it is well within the realm of possibility that Draghi’s government could get a deal done on a non-contentious matter like this over the next month and a half or so.

Beyond that immediate task, though, we think Draghi’s government will likely face the same gridlock as its predecessors. In Draghi’s first major speech to Italy’s Parliament last week, he touted citizens ceding more sovereignty to the EU—including a permanent, common EU budget charged with supporting the bloc in times of economic pressure. He also referenced sweeping tax and immigration reforms. These are all just general ideas, not legislation. But we have observed them to be contentious ideas in Italy in the past, meaning any associated measures would likely prove difficult to enact. The parties in Draghi’s coalition have publicly espoused quite disparate views of them, and getting consensus has proven extraordinarily difficult in Italy over the past several years. All across Europe—in Holland, Germany, Spain and more—big tent coalitions that unite political opponents have proven incapable of passing big new laws.

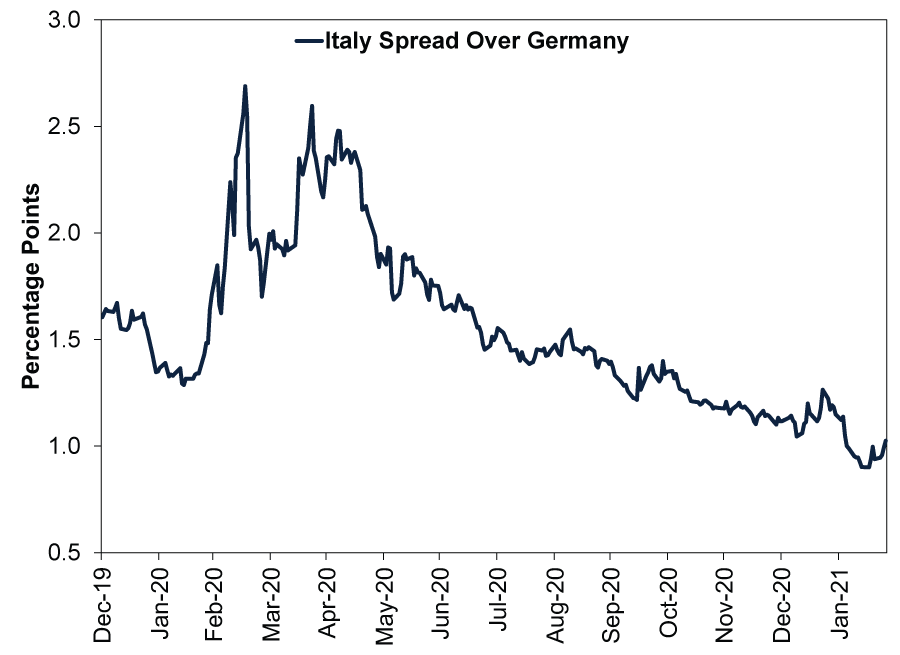

Many financial commentators we follow now cite Draghi’s popularity and reputation for competence as reasons he will buck the trend and succeed in passing major reforms. Some even claim this is a positive driver for Italian shares, citing factors like the initial narrowing in the gap between Italy’s 10-year yield and Germany’s since his appointment. In the eurozone, the difference between a member-state’s sovereign yield and Germany’s yield is a common measure of perceived risk, since Germany’s creditworthiness is widely seen as the highest in the bloc. Therefore, a lower spread theoretically shows investors have more confidence in a Draghi-run Italy. But as Exhibit 1 illustrates, that narrowing started after the lockdown-driven crisis inflated spreads last spring. Yes, spreads ticked higher when the Renzi-Conte spat started early this year and reversed as Draghi’s appointment reduced uncertainty. But that is a short-term wiggle amid a longer trend—a wiggle that has reversed somewhat already. We wouldn’t overthink it.

Exhibit 1: Italy 10-Year Spread Versus Germany

Source: FactSet, as of 25/2/2021. 31/12/2019 – 25/2/2021.

A popular incoming technocrat isn’t unprecedented in Italy. Former Prime Minister Mario Monti’s appointment in 2011 was greeted with similar cheer throughout the financial press. His technocratic government, installed at the height of the eurozone debt crisis, won confidence votes by a 281 – 25 margin in the Senate and 556 – 61 in the Chamber of Deputies. Only one party—Lega’s forerunner, the Northern League—opposed him. That is eerily similar to Draghi’s government now. Monti’s government accomplished relatively little and mostly stoked a backlash against unelected leaders that we think may have contributed to Italian populism’s rise.

Now, some observers we follow note the outgoing Conte government had a penchant for meddling in corporate affairs—blocking foreign acquisitions of Italian firms, urging domestic mergers and using its control of the state lender, Cassa Depositi e Prestiti, to try to acquire the assets of some private firms.[i] Perhaps the potential end of that is a modest plus. But we see little evidence indicating it is a huge matter for equities, and would suggest Italy’s heavy value tilt explains its equity market’s relative underperformance versus the world better during Conte’s time at the country’s helm.[ii] (Value-orientated companies tend to carry relatively lower price-to-earnings ratios and more debt, making them more sensitive to economic conditions, and they tend to return more money to shareholders via dividends and share buybacks and invest less in growth-orientated endeavours.)

We have a strong hunch that, beyond COVID aid decisions, Italy’s coalition is likely to return to inactive infighting. The fragility of the country’s governments in recent years highlights that—it doesn’t undercut it. That inactivity means reforms—which our research shows nearly always create winners and losers, often bring unintended consequences and occasionally roil markets—aren’t likely. Gridlock, in our view, mitigates the risk a potential political negative strikes equity markets.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Assessing Private Credit Risks and Exposures2026-06-09

-

Macro Insights SpaceX IPO and Rising Equity Supply2026-06-09

-

In The News Trump’s tariff turmoil isn’t just delayed – it’s never coming2026-06-08

-

Macro Insights Brazil Review & Outlook2026-06-04

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today