Personal Wealth Management / Market Analysis

Surveys Still Say No to Global Recession

We think the latest flash PMIs suggest economic activity is holding up better than many financial commentators think.

With each passing day, more and more headlines in financial publications we monitor warn of impending global recession (a decline in broad economic output). Yet we don’t think economic data we have reviewed support that argument. The latest business surveys imply ongoing growth—another overlooked positive amidst today’s dreary sentiment backdrop, in our view.

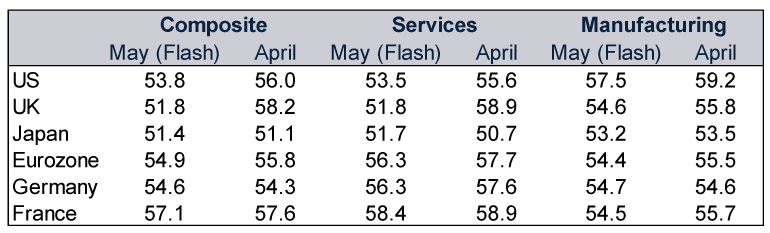

Though most major developed countries’ flash (preliminary) May purchasing managers’ indexes (PMIs) missed consensus expectations, they were also uniformly well above 50—suggesting a majority of respondents reported expansion. (Exhibit 1) PMIs are surveys tracking whether companies’ purchasing managers observed improvement or deterioration across a number of categories. On an individual nation basis, we observed many headlines focus on the UK’s weakest services PMI reading in 15 months, as survey respondents blamed economic and geopolitical uncertainty for the slowdown in client demand.[i] A development that received less attention based on our coverage: PMIs out of the eurozone and its two largest economies, Germany and France, continued showing growth despite myriad warnings that the Russia – Ukraine war would roil economic activity on the Continent.[ii]

Exhibit 1: The Latest PMIs

Source: FactSet and S&P Global, as of 25/5/2022.

Flash estimates reflect about 85% – 90% of total survey responses, so it is possible May’s final results get revised slightly after all data are collected.[iii] But we think those updates are unlikely to materially alter PMIs’ main message: The majority of reporting businesses are expanding. As always, PMIs aren’t perfect, as the surveys reveal the breadth of growth—how many businesses reported expansion. That is unlike output data like GDP (gross domestic product, a government-produced measure of economic output), which tally the magnitude, so PMIs don’t reveal how much businesses grew or shrank in aggregate. However, we think they offer a timely snapshot of recent economic conditions—and usually give a sense of broad economic direction.

Based on our coverage, the takeaways from May’s preliminary PMIs revolved around negatives that have led headlines in financial publications we follow for months. For example, UK goods producers pointed out growth headwinds tied to the war in Ukraine; Japanese manufacturers noted heightened supply chain pressures due to renewed lockdowns in China; and US firms reported a notable uptick in input costs.[iv]

Whilst pessimism coloured the coverage, PMI respondents also raised some positives—specifically, COVID restrictions’ easing as an offset to headwinds. Japan saw the strongest rise in services activity in five months thanks to the reduced impact of COVID restrictions, benefitting the tourism sector.[v] In France, businesses reported the resumption of projects previously put on hold and the return of trade shows and public events boosted economic activity.[vi]

Germany’s May flash PMI seems particularly noteworthy to us. Just a couple months ago, we observed many economists who thought recession in Europe’s largest economy was highly likely, tied to its large manufacturing sector’s energy intensity and exposure to raw materials in short supply.[vii] We think expansionary German PMIs from January – March argued against that dour forecast, and official GDP confirmed it was off base after 0.2% q/q growth in Q1.[viii] And now, as S&P Global Economics Associate Director Phil Smith noted, “A post-lockdown recovery in services activity continues to provide a strong tailwind for the German economy … Even manufacturing saw a slightly better performance in terms of production levels in May.”[ix] German PMIs remain expansionary thus far in Q2 despite the ongoing war—more evidence of the economy’s resilience, in our view.[x]

We don’t dismiss the possibility of an economic downturn lurking, but to cause a global recession, our study of history suggests the economic negative must be capable of destroying trillions of pounds in global GDP. Our review of forward-looking economic indicators and current political conditions doesn’t reveal anything that may qualify right now. Yes, we see plenty of regional economic headwinds (e.g., China’s latest lockdowns). But unless a negative morphs into something with the scale of roiling the global economy, a global recession is unlikely, in our view. Critically, today’s negatives are also broadly discussed amongst financial market observers and commentators we follow, sapping their ability to sneak up on anyone.

Moreover, our research shows signs of a looming global recession aren’t showing up in most broad economic data. Despite the war in Ukraine, data, including PMIs, continue pointing to eurozone growth—arguing against a regional recession on the Continent.[xi] We think PMIs better resemble a return to pre-pandemic trends, with countries getting back to a more normal mix of economic activity within the services and manufacturing sectors—where the former dominates GDP amongst major developed nations.[xii] As society makes its way to a post-COVID reality and learns to live with the virus, we think services will continue chugging along, benefitting those developed world, services-driven economies.

Now, we acknowledge individual nations or even regions may struggle economically, and some may even suffer recessions. However, our study of economic history implies that is true even during long-running global expansions—for example, during the 2009 – 2020 global expansion, the eurozone endured a regional economic downturn that didn’t prevent world GDP from rising.[xiii] We have found pockets of weakness don’t automatically derail everything else, as very often, areas of strength wind up pulling them along. In our view, reality continues to look better than many economic commentators we follow seem to appreciate, especially amidst the prevalent pessimism right now. The big disconnect between expectations and economic reality is reason to be optimistic about stocks going forward, in our view.

[i] Source: S&P Global, as of 24/5/2022.

[ii] “How Russia’s War Could Knock Out Europe’s Economy,” Charles Riley, CNN, 8/3/2022.

[iii] See note i.

[iv] Ibid.

[v] Ibid.

[vi] Ibid.

[vii] “Recession Warning From Germany’s Top Economic Advisors as Putin’s Gas Deadline Nears,” Silvia Amaro, CNBC, 31/3/2022.

[viii] Source: FactSet, as of 24/5/2022.

[ix] Source: S&P Global, as of 24/5/2022.

[x] Source: FactSet, as of 24/5/2022.

[xi] Ibid. Statement based on composite PMIs for eurozone, Germany and France, May 2022.

[xii] Source: World Bank, as of 26/5/2022. Statement based on services, value added as a percentage of GDP, for eurozone (66.4% as of 2020), UK (72.8% as of 2020), the United States (77.3% as of 2019) and Japan (69.3% as of 2019).

[xiii] Source: World Bank, as of 25/4/2022. Statement based on annual percent change in World GDP and eurozone GDP in constant 2015 USD in 2012.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Macro Insights Q1 2026 Global Markets Review & Outlook2026-05-12

-

Macro Insights Why Global Small Cap2026-05-07

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Market Analysis Europe’s Resilient Q1 GDP2026-05-01

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today