Personal Wealth Management / Economics

The Latest Confirmation of a Tough 2022

The latest output data aren’t great, but we think they are old news to markets.

Output gauges haven’t yet caught up to the fresh, preliminary 2023 purchasing managers’ indexes we detailed on Wednesday—both in terms of timing and the data themselves, which weren’t rosy. However, the latest output data’s findings provide insight on certain parts of the global economy—which we think can reduce uncertainty. Moreover, based on our coverage, there are some little-noticed signs of improvement, too, suggesting a lot of room for positive surprise that can be the foundation of a stock market rebound, in our view.

Japan’s Weak Core Machinery Orders

Japanese core machinery orders, which many observers we follow treat as a sign of future corporate investment, fell -8.3% m/m in November, much worse than consensus estimates of -0.9%.[i] (Core machinery orders are for capital goods excluding ship and electric utility firms.) We think that is a noteworthy drop for a series that is seasonally adjusted (adapted to remove skew from holidays, weather and other recurring events), although our research has found this metric tends to be more variable than others. Weakness was broad: Manufacturers’ orders fell -9.3% m/m due to a slump in semiconductor production equipment whilst non-manufacturers’ orders slipped -3.0% on tepid demand from the information service sector.[ii]

Japan’s Cabinet Office blamed poor orders on the global economic slowdown, and whilst Japanese factory orders are a notoriously volatile dataset, they struggled for most of 2022—contracting on a monthly basis in 7 of 11 reported months.[iii] Based on our analysis, several headwinds weighed on orders, from semiconductor shortages disrupting production to flagging external demand. Moreover, the zero-COVID strategy of China, Japan’s largest trading partner, also appeared to hurt business.[iv] Though easing COVID restrictions may drive something of a near-term economic bounce once the issues from the outbreak cool, we don’t think a huge rebound is likely.

Regardless, Japanese factories’ struggles are well known and in line with other manufacturing-related weakness (e.g., America's factory orders for durable goods, or goods designed to last at least three years). In our view, stocks have likely digested the developments and moved on. Consider: During a challenging 2022 for markets, global stocks fell as much as -15.3% in British pounds—and over that same period, Japanese machinery stocks fared worse, falling -18.1%.[v]

November data won’t shed much new insight about the future, but we think they do add more fodder to the overall negative sentiment we have observed towards the global economy—a typical backdrop for a market recovery, according to our research. We think weak orders could also reduce uncertainty by confirming trends stocks hinted at, allowing investors to move on.

Poor UK Retail Sales

UK December retail sales fell -1.0% m/m, missing analysts’ consensus expectations for a 0.5% rise.[vi] Unlike most other major economies, the UK adjusts sales for inflation (broadly rising prices across the economy)—and December’s figures suggest elevated prices are weighing on consumers. Non-food stores sales dropped -2.1% m/m as retailers reported reduced spending tied to affordability concerns.[vii] Discretionary spending in particular took a hit: Other non-food stores sales tumbled -6.2% as spending fell on cosmetics, sports equipment, games and toys, and watches and jewellery.[viii] Food stores sales contracted -0.3% m/m due in part to customers’ stocking up early for Christmas in November—though supermarkets also reported a decline in volumes sold because of high food prices.[ix]

Many financial commentators we follow argued December’s unexpected contraction signalled inflation dampened consumers’ holiday mood. Whilst higher prices are likely the primary culprit, we think there are some other factors perhaps exacerbating weakness. Thanks to Black Friday (the day after America’s Thanksgiving holiday in which retailers offer big discounts, traditionally kicking off the holiday shopping season), which UK retailers imported in recent years, holiday discounting started in November, pulling some demand ahead—which may have impacted month-on-month reads despite seasonal adjustments.[x] Another one-time variable we think may have possibly thrown off the usual seasonal adjustment calculations: the World Cup football tournament, which happens every four years, but typically during the summer. Postal strikes, too, may have weighed on some online spending.[xi]

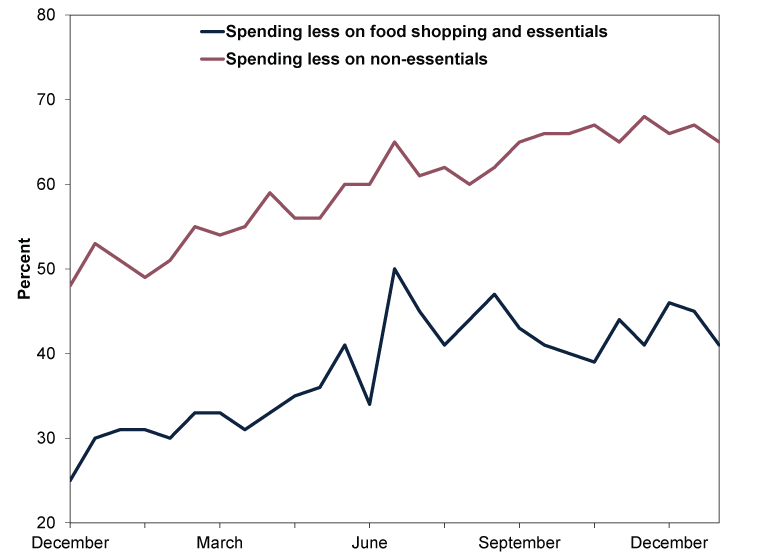

From an investing perspective, though, we think higher prices’ hitting cash-strapped households is a well-known issue. Per the Office for National Statistics’ (ONS’) “Opinions and Lifestyle Survey,” the number of respondents reporting reduced spending due to a rising cost of living has steadily climbed over the past year. (Exhibit 1) Now, we have found survey responses often don’t correlate with action—consumers may still spend despite saying they feel down about the economy. But in our view, when a majority of people tell a survey rising prices have weighed on their discretionary spending, markets are likely well aware of the issue, too—and have likely discounted the news accordingly.

Exhibit 1: UK Households Are Aware of Rising Prices

Source: ONS, as of 23/1/2023. “Public Opinions and Social Trends, Great Britain: 21 December 2022 to 8 January 2023.”

Ongoing Moderation on the Inflation Front

Whilst UK retail sales likely were hurt by hot inflation, we think there are nascent improvements worth noting. UK CPI rose 10.5% y/y in December, down from November’s 10.7% and extending the slowdown from October’s 41-year high of 11.1%.[xii] Of CPI’s 12 categories, 7 detracted—led by Transport (which decelerated from November’s 7.2% y/y to 6.5%—contributing to December’s slower inflation rate).[xiii] Core CPI, which excludes food, energy, alcohol and tobacco prices, rose 6.3% y/y, repeating November’s rate.[xiv] Despite the general improvement, many financial commentators we monitor shifted their analysis from high energy prices to focussing on surging food prices (up 16.8% y/y) and still-rising services prices.[xv]

Elsewhere, the US Producer Price Index (PPI), which tracks American businesses’ costs, echoed UK CPI’s findings. It fell -0.5% m/m (up 6.2% y/y) in December—the gauge’s sharpest monthly contraction since April 2020’s lockdown-induced -1.3%.[xvi] Behind the drop were falling energy (-7.9% m/m) and food (-1.2%) prices.[xvii] Core PPI, which excludes energy and food prices, rose 0.2% m/m, a tick slower than last month’s 0.3% rate.[xviii] Similar to the UK, we saw observers raise concerns about services prices—along with questions about China’s reopening and its impact on commodity prices.

In our view, the broad focus on negative developments is evidence of what we call the pessimism of disbelief, which our market analysis has shown is often the sentiment backdrop in a market recovery. To us, the broader implication is more notable: Inflation measures globally have been easing over the past several months, a sign one of the dominant fears from 2022 has been gradually abating. That few seem to recognise that now is a counterintuitive reason to be optimistic about stocks in 2023, in our view.

[i] Source: FactSet, as of 25/1/2023.

[ii] Ibid.

[iii] Ibid.

[iv] Source: World Bank, as of 27/1/2023. Based on 2020 trade data, which are the latest available.

[v] Source: FactSet, as of 27/1/2023. MSCI World Index returns with net dividends, in GBP, and MSCI Japan Machinery Industry returns with net dividends, in GBP, 10/12/2021 – 20/6/2022. Currency fluctuations between the pound and other currencies may result in higher or lower investment returns.

[vi] Source: Office for National Statistics, as of 23/1/2023.

[vii] Ibid.

[viii] Ibid.

[ix] Ibid.

[x] Ibid.

[xi] Ibid.

[xii] Ibid.

[xiii] Ibid.

[xiv] Ibid.

[xv] Ibid.

[xvi] See note i.

[xvii] Ibid.

[xviii] Ibid.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Markets Are Always Changing—What Can You Do About It?

Get tips for enhancing your strategy, advice for buying and selling and see where we think the market is headed next.

Related Resources

-

Market Volatility What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-31

-

Politics This Week in Gridlock: Europe Edition2026-03-27

-

In The News Predictions of an AI dystopia are the height of arrogance2026-03-23

Contact Us

Learn why 200,000 clients trust Fisher Investments and its affiliates to manage their money and find out how we may be able to help you achieve your financial goals.

As of 31/03/2026. Includes Fisher Investments and its affiliates.

New to Fisher? Call Us.

Contact Us Today